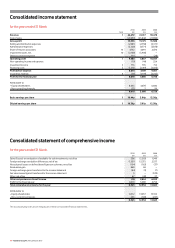

Vodafone 2010 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2010 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

72 Vodafone Group Plc Annual Report 2010

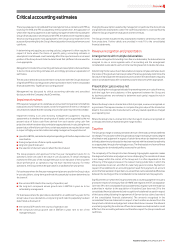

Estimation of useful life

The useful life used to amortise intangible assets relates to the future performance

of the assets acquired and management’s judgement of the period over which

economic benefit will be derived from the asset. The basis for determining the useful

life for the most significant categories of intangible assets is as follows:

Licences and spectrum fees

The estimated useful life is generally the term of the licence unless there is a

presumption of renewal at negligible cost. Using the licence term reflects the period

over which the Group will receive economic benefit. For technology specific licences

with a presumption of renewal at negligible cost, the estimated useful economic life

reflects the Group’s expectation of the period over which the Group will continue to

receive economic benefit from the licence. The economic lives are periodically

reviewed taking into consideration such factors as changes in technology. Historically

any changes to economic lives have not been material following these reviews.

Customer bases

The estimated useful life principally reflects management’s view of the average

economic life of the customer base and is assessed by reference to customer churn

rates. An increase in churn rates may lead to a reduction in the estimated useful life

and an increase in the amortisation charge. Historically changes to the estimated

useful lives have not had a significant impact on the Group’s results and financial position.

Capitalised software

The useful life is determined by management at the time the sof tware is acquired and

brought into use and is regularly reviewed for appropriateness. For computer

software licences, the useful life represents management’s view of expected benefits

over which the Group will receive benefits from the software, but not exceeding the

licence term. For unique software products controlled by the Group, the life is based

on historical experience with similar products as well as anticipation of future events

which may impact their life such as changes in technology. Historically changes in

useful lives have not resulted in material changes to the Group’s amortisation charge.

Property, plant and equipment

Property, plant and equipment also represent a significant proportion of the asset

base of the Group being 12.9% (2009: 12.6%) of the Group’s total assets. Therefore the

estimates and assumptions made to determine their carrying value and related

depreciation are critical to the Group’s financial position and performance.

Estimation of useful life

The charge in respect of periodic depreciation is derived after determining an

estimate of an asset’s expected useful life and the expected residual value at the end

of its life. Increasing an asset’s expected life or its residual value would result in a

reduced depreciation charge in the consolidated income statement.

The useful lives and residual values of Group assets are determined by management

at the time the asset is acquired and reviewed annually for appropriateness. The lives

are based on historical experience with similar assets as well as anticipation of future

events which may impact their life such as changes in technology. Furthermore

network infrastructure is only depreciated over a period that extends beyond

the expiry of the associated licence under which the operator provides

telecommunications services

if there is a reasonable expectation of renewal or an

alternative future use for the asset.

Historically changes in useful lives and residual values have not resulted in material

changes to the Group’s depreciation charge.

Provisions and contingent liabilities

The Group exercises judgement in measuring and recognising provisions and the

exposures to contingent liabilities related to pending litigation or other outstanding

claims subject to negotiated settlement, mediation, arbitration or government

regulation, as well as other contingent liabilities (see note 29 to the consolidated

financial statements). Judgement is necessary in assessing the likelihood that a

pending claim will succeed, or a liability will arise, and to quantify the possible range

of the financial settlement. Because of the inherent uncertainty in this evaluation

process, actual losses may be different from the originally estimated provision.

Recognition of deferred tax assets

The recognition of deferred tax assets is based upon whether it is more likely than not

that sufficient and suitable taxable prof its will be available in the future against which

the reversal of temporary differences can be deducted.Where the temporary

differences related to losses, the availability of the losses to offset against forecast

taxable profits is also considered.

Recognition therefore involves judgement regarding the future financial performance

of the particular legal entity or tax group in which the deferred tax asset has

been recognised.

Historical differences between forecast and actual taxable profits have not resulted

in material adjustments to the recognition of deferred tax assets.

Business combinations

The recognition of business combinations requires the excess of the purchase price

of acquisitions over the net book value of assets acquired to be allocated to the

assets and liabilities of the acquired entity. The Group makes judgements and

estimates in relation to the fair value allocation of the purchase price. If any unallocated

portion is positive it is recognised as goodwill and if negative, it is recognised in the

income statement.

Goodwill

The amount of goodwill initially recognised as a result of a business combination is

dependent on the allocation of the purchase price to the fair value of the identifiable

assets acquired and the liabilities assumed. The determination of the fair value of the

assets and liabilities is based, to a considerable extent, on management’s judgement.

Allocation of the purchase price affects the results of the Group as finite lived

intangible assets are amortised, whereas indefinite lived intangible assets, including

goodwill, are not amortised and could result in differing amortisation charges based

on the allocation to indefinite lived and finite lived intangible assets.

On transition to IFRS the Group elected not to apply IFRS 3, “Business combinations”,

retrospectively as the difficulty in applying these requirements to the large number

of business combinations completed by the Group from incorporation through to

1 April 2004 exceeded any potential benefits. Goodwill arising before the date of

transition to IFRS, after adjusting for items including the impact of proportionate

consolidation of joint ventures, amounted to £78,753 million.

If the Group had elected to apply the accounting for business combinations

retrospectively it may have led to an increase or decrease in goodwill and increase in

licences, customer bases, brands and related deferred tax liabilities recognised

on acquisition.

Finite lived intangible assets

Other intangible assets include the Group’s aggregate amounts spent on the

acquisition of 2G and 3G licences, computer software, customer bases, brands and

development costs. These assets arise from both separate purchases and from

acquisition as part of business combinations.

On the acquisition of mobile network operators the identifiable intangible assets may

include licences, customer bases and brands. The fair value of these assets is

determined by discounting estimated future net cash flows generated by the asset

where no active market for the assets exist. The use of different assumptions for the

expectations of future cash flows and the discount rate would change the valuation

of the intangible assets.

The relative size of the Group’s intangible assets, excluding goodwill, makes the

judgements surrounding the estimated useful lives critical to the Group’s financial

position and performance.

At 31 March 2010 intangible assets, excluding goodwill, amounted to £22,420 million

(2009: £20,980 million) and represented 14.3% (2009: 13.7%) of the Group’s

total assets.

Critical accounting estimates continued