Vodafone 2010 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2010 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Performance

Vodafone Group Plc Annual Report 2010 35

Other Africa and Central Europe

Service revenue declined by 0.9%(*) due to the performance in Turkey combined with

the impact of deteriorating economic conditions across Central Europe, most notably

in Romania in the fourth quarter. Service revenue in Turkey decreased by 7.6%(*) with

an 18.4%(*) fall in the fourth quarter. Termination rate cuts adversely impacted

revenue by 6.9% and revenue was further depressed by a higher rate of churn and a

decline in prepaid ARPU due to intense competition in the market. Consumer

confidence in Turkey fell with the deterioration in the macroeconomic environment

impacting revenue. Competition also intensified with the launch of mobile number

portability in November 2008 leading to aggressive acquisition and pricing

campaigns, especially in the fourth quarter of the year. Mobile ARPU fell in the second

half of the year but stabilised in the fourth quarter following successful promotions.

In Romania service revenue grew by 1.1%(*) but deteriorated during the year with a

10.3%(*) decline in the fourth quarter. The market continued to mature, with the

decline in ARPU resulting from local currency devaluation against the euro – whilst

tariffs are quoted in euros household incomes are earned in local currency – in

addition to market led price reductions impacting performance in the fourth quarter

in particular. These effects were partially offset by data revenue growth following

successful data promotions and flexible access offers which led to a rise in the

number of mobile PC connectivity devices.

EBITDA decreased by 6.7%(*), with the EBITDA margin also declining due to the fall in

revenue and investment in the turnaround plan in Turkey. EBITDA in Turkey declined

by 36.6%(*) as a result of the decline in revenue and increased operating expenses

reflecting higher marketing costs, higher technology costs due to expansion of the

network and organisational restructuring as part of the turnaround plan. In Romania

EBITDA decreased by 3.7%(*) as aggressive market competition and higher gross

customer additions led to the rise in the cost of acquiring and retaining customers.

In May 2008 the Group changed the consolidation status of Safaricom from a joint

venture to an associate following completion of the share allocation for the public

offering of 25.0% of Safaricom’s shares previously held by the Government of Kenya

and termination of the shareholders’ agreement with the Government of Kenya. In

August 2008 we acquired 70.0% of Ghana Telecommunications Company Limited

which offers both mobile and fixed services. We also increased our stake in Polkomtel

from 19.6% to 24.4% in December 2008.

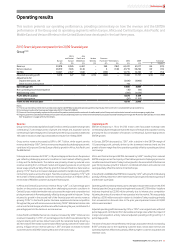

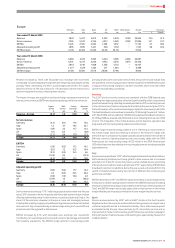

Asia Pacic and Middle East

Asia

Pacific

and

Elimi- Middle

India Other nations East % change

£m £m £m £m £Organic

Year ended

31 March 2009

Revenue 2,689 3,131 (1) 5,819 32.3 9.3

Service revenue 2,604 2,831 (1) 5,434 32.5 8.5

EBITDA 717 1,062 −1,779 18.3 6.9

Adjusted

operating

(loss)/profit (30) 586 −556 0.5 5.8

EBITDA margin 26.7% 33.9% 30.6%

Year ended

31 March 2008

Revenue 1,822 2,577 −4,399

Service revenue 1,753 2,348 −4,101

EBITDA 598 906 −1,504

Adjusted

operating profit 35 518 −553

EBITDA margin 32.8% 35.2% 34.2%

Revenue increased by 32.3%, including the contribution from favourable

exchange rate movements in addition to the benefit from acquisitions, primarily

in India. Revenue growth on a pro-forma basis was 19%, reflecting the growth in

India, Egypt and Australia. Service revenue increased by 8.5%(*) primarily as a

result of the 27.3% organic rise in the average customer base, although revenue

growth slowed as a result of stronger competition coupled with maturing

market conditions.

EBITDA grew by 18.3% with favourable exchange rate movements and the positive

impact of acquisitions contributing to the growth. On a pro-forma basis including

India, EBITDA increased by 7%. The decline in the EBITDA margin resulted from

positive performances in India and Egypt being mitigated by a decline in Australia.

The impact of merger and acquisition activity and foreign exchange movements on

revenue, service revenue, EBITDA and adjusted operating profit are shown below:

Organic M&A Foreign Reported

growth activity exchange growth

%pps pps %

Revenue

Asia Pacific and Middle East 9.3 13.3 9.7 32.3

Service revenue

India –42.5 6.0 48.5

Other 8.5 0.3 11.8 20.6

Asia Pacific and Middle East 8.5 14.2 9.8 32.5

EBITDA

India –14.1 5.8 19.9

Other 6.9 (3.4) 13.7 17.2

Asia Pacific and Middle East 6.9 0.6 10.8 18.3

Adjusted operating profit

India –(173.2) (12.5) (185.7)

Other 5.8 (6.8) 14.1 13.1

Asia Pacific and Middle East 5.8 (19.7) 14.4 0.5

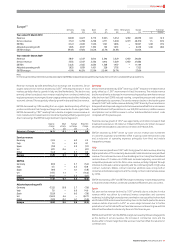

India

Revenue grew by 33% on a pro-forma basis, with growth in the fourth quarter of

27.7%(*). Growth in the fourth quarter remained stable in comparison to the third

quarter as the eight percentage point benefit of the new revenue stream from the

network sharing joint venture, Indus Towers, which launched during the first half of

the 2009 financial year, offset the slowing underlying growth rate. Visitor revenue

increased, albeit at a lower rate, due to the impact of economic pressures as people

travel less. Lower effective rates per minute reflecting price reductions earlier in the

year, coupled with the continued market shift to lifetime validity prepaid offerings,

led to a reduction in customer churn. The lower effective rate and a slight fall in usage

per customer were mitigated by net customer additions, which averaged 2.1 million

per month, and the launch of services in seven new circles, bringing the closing

customer base to 68.8 million. Customer penetration in the Indian mobile market

reached 34% at 31 March 2009.

EBITDA grew by 6% on a pro-forma basis. Customer costs as a percentage of revenue

decreased, benefiting from economies of scale. Licensing costs increased as

discounts received from the regulator in some service areas were terminated.

Network expansion continued, with an average of 2,600 base stations constructed

per month, primarily in the new circles. Site sharing increased and Indus Towers

steadily increased its operations throughout the rest of the year, with 95,000 sites

under its management at the end of March 2009.