Vodafone 2010 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2010 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

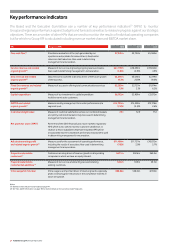

Performance

Vodafone Group Plc Annual Report 2010 33

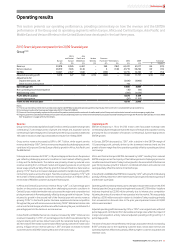

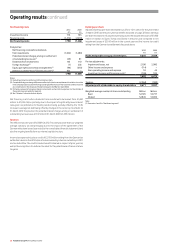

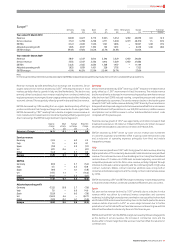

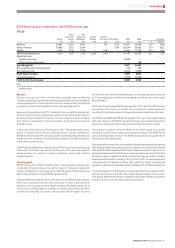

Europe

Germany Italy Spain UK Other Eliminations Europe % change

£m £m £m £m £m £m £m £Organic

Year ended 31 March 2009

Revenue 7,847 5,547 5,812 5,392 5,329 (293) 29,634 13.6 (2.1)

Service revenue 7,535 5,347 5,356 4,912 5,029 (293) 27,886 14.1 (1.7)

EBITDA 3,225 2,565 2,034 1,368 1,957 −11,149 9.7 (5.0)

Adjusted operating profit 1,835 1,839 1,421 328 1,702 −7,125 9.8 (5.4)

EBITDA margin 41.1% 46.2% 35.0% 25.4% 36.7% 37.6%

Year ended 31 March 2008

Revenue 6,866 4,435 5,063 5,424 4,583 (290) 26,081

Service revenue 6,551 4,273 4,646 4,952 4,295 (287) 24,430

EBITDA 2,816 2,148 1,908 1,560 1,735 −10,167

Adjusted operating profit 1,577 1,528 1,362 517 1,504 –6,488

EBITDA margin 41.0% 48.4% 37.7% 28.8% 37.9% 39.0%

Revenue increased by 13.6%, with favourable euro exchange rate movements

contributing 14.3 percentage points of growth and mergers and acquisitions activity,

primarily Tele2, contributing a further 1.4 percentage point benefit. The organic

decline in revenue of 2.1% was a result of a 1.7% decrease in service revenue and a

decline in equipment revenue, reflecting lower volumes.

The impact of merger and acquisition activity and foreign exchange movements on

revenue, service revenue, EBITDA and adjusted operating profit are shown below:

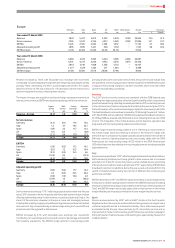

Organic M&A Foreign Reported

growth activity exchange growth

%pps pps %

Revenue – Europe (2.1) 1.4 14.3 13.6

Service revenue

Germany (2.5) (0.1) 17.6 15.0

Italy 1.2 4.7 19.2 25.1

Spain (4.9) 2.5 17.7 15.3

UK (1.1) 0.3 −(0.8)

Other (1.2) 0.4 17.9 17.1

Europe (1.7) 1.4 14.4 14.1

EBITDA

Germany (2.8) (0.2) 17.5 14.5

Italy (0.1) 1.2 18.3 19.4

Spain (9.2) (0.5) 16.3 6.6

UK (12.8) 0.5 −(12.3)

Other (4.3) (0.1) 17.2 12.8

Europe (5.0) 0.2 14.5 9.7

Adjusted operating profit

Germany (0.9) (0.4) 17.7 16.4

Italy 2.4 (0.5) 18.5 20.4

Spain (9.8) (1.9) 16.0 4.3

UK (37.9) 1.3 −(36.6)

Other (4.8) 1.1 16.9 13.2

Europe (5.4) (0.3) 15.5 9.8

Service revenue declined by 1.7%(*), reflecting a gradual deterioration over the year

and a 3.3%(*) decrease in the fourth quarter, with favourable trends in Italy more than

offset by deteriorating trends in other markets, in particular Spain and Greece. The

impact of the economic slowdown in Europe on voice and messaging revenue,

including from roaming, ongoing competitive pricing pressures and lower termination

rates were not fully compensated by increased usage arising from new tariffs and

promotions and strong growth in data revenue.

EBITDA increased by 9.7%, with favourable euro exchange rate movements

contributing 14.5 percentage points of growth and a 0.2 percentage point benefit

from business acquisitions. The EBITDA margin declined 1.4 percentage points

primarily driven by the downward revenue trend, the growth of lower margin fixed

line operations, a brand royalty provision release included in the 2008 financial year

in Italy and restructuring charges in a number of markets, which more than offset

customer and operating cost savings.

Germany

The 2.5%(*) decline in service revenue was consistent with the 2008 financial year,

benefiting from higher penetration of the new SuperFlat tariff portfolio. Data revenue

growth remained strong, reflecting increased penetration of PC connectivity services

in the customer base. Fixed line revenue declined during the year, but grew 2.1%(*) in

the fourth quarter, as the customer base largely migrated to new, lower priced tariffs.

The fixed broadband customer base increased by 15.9% during the year to 3.1 million

at 31 March 2009, with an additional 154,000 wholesale fixed broadband customers.

On 19 May 2008 we acquired a 26.4% interest in Arcor, following which we own 100%

of Arcor. The integration of the mobile business and the fixed line operations has

progressed, with cost savings being realised according to plan.

EBITDA margin remained broadly stable at 41.1%, reflecting an improvement in

the mobile margin which was offset by a decline in the fixed line margin, with

the former due to a reduction in prepaid subsidies and an increase in the number of

SIM-only contracts. Operating expenses were also broadly stable with the 2008

financial year as a restructuring charge of €35 million in the 2009 financial year

(£32 million) was more than offset by non-recurring adjustments, including favourable

legal settlements.

Italy

Ser vice revenue grow th was 1.2%(*) reflecting targeted demand stimulation initiatives,

ARPU enhancing initiatives and strong growth in data revenue due to increased

penetration of mobile PC connectivity devices, email enabled devices and mobile

internet services. Fixed line revenue growth was 3.7%(*). supported by 278,000 fixed

broadband customer net additions during the year as well as the benefit from the

launch of Vodafone Station during the summer of 2008 and the continued good

performance of Tele2.

EBITDA declined by 0.1%(*) and EBITDA margin declined by 2.2 percentage points

mainly due to a brand royalty provision release in the 2008 financial year. Excluding

the impact of the brand royalty provision release and the impact of the acquisition of

Tele2, the EBITDA margin was broadly stable, with an improvement in the mobile

margin offsetting the increased contribution of lower margin fixed line services.

Spain

Service revenue declined by 4.9%(*) with an 8.6%(*) decline in the fourth quarter.

Negative trends in the economic environment put strong pressure on usage in some

customer segments and led to increased involuntary churn. Data revenue growth

accelerated during the year, driven primarily by PC connectivity services and an

improvement in media content revenue growth following a successful campaign in

the fourth quarter. Fixed line revenue continued to grow, supported by the launch of

Vodafone Station.