Vodafone 2010 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2010 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Financials

Vodafone Group Plc Annual Report 2010 71

The Group prepares its consolidated financial statements in accordance with IFRS as

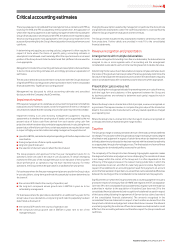

issued by the IASB and IFRS as adopted by the European Union, the application of

which often requires judgements to be made by management when formulating the

Group’s financial position and results. Under IFRS, the directors are required to adopt

those accounting policies most appropriate to the Group’s circumstances for the

purpose of presenting fairly the Group’s financial position, financial performance and

cash flows.

In determining and applying accounting policies, judgement is often required in

respect of items where the choice of specific policy, accounting estimate or

assumption to be followed could materially affect the reported results or net asset

position of the Group should it later be determined that a different choice would be

more appropriate.

Management considers the accounting estimates and assumptions discussed below

to be its critical accounting estimates and, accordingly, provides an explanation of

each below.

The discussion below should also be read in conjunction with the Group’s disclosure

of significant IFRS accounting policies which is provided in note 2 to the consolidated

financial statements, “Significant accounting policies”.

Management has discussed its critical accounting estimates and associated

disclosures with the Company’s Audit Committee.

Impairment reviews

IFRS requires management to undertake an annual test for impairment of indefinite

lived assets and, for finite lived assets, to test for impairment if events or changes in

circumstances indicate that the carrying amount of an asset may not be recoverable.

Impairment testing is an area involving management judgement, requiring

assessment as to whether the carrying value of assets can be supported by the net

present value of future cash flows derived from such assets using cash flow

projections which have been discounted at an appropriate rate. In calculating the net

present value of the future cash flows, certain assumptions are required to be made

in respect of highly uncertain matters including management’s expectations of:

growth in EBITDA, calculated as adjusted operating profit before depreciation and

amortisation;

timing and quantum of future capital expenditure;

long term growth rates; and

the selection of discount rates to reflect the risks involved.

The Group prepares and approves formal five year management plans for its

operations, which are used in the value in use calculations. In certain developing

markets the fifth year of the management plan is not indicative of the long-term

future performance as operations may not have reached maturity. For these

operations, the Group extends the plan data for an additional five year period.

For businesses where the five year management plans are used for the Group’s value

in use calculations, a long-term growth rate into perpetuity has been determined as

the lower of:

the nominal GDP rates for the country of operation; and

the long-term compound annual growth rate in EBITDA in years six to ten

estimated by management.

For businesses where the plan data is extended for an additional five years for the

Group’s value in use calculations, a long-term growth rate into perpetuity has been

determined as the lower of:

the nominal GDP rates for the country of operation; and

the compound annual growth rate in EBITDA in years nine to ten of the

management plan.

Changing the assumptions selected by management, in particular the discount rate

and growth rate assumptions used in the cash flow projections, could significantly

affect the Group’s impairment evaluation and hence results.

The Group’s review includes the key assumptions related to sensitivity in the cash

flow projections. Further details are provided in note 10 to the consolidated

financial statements.

Revenue recognition and presentation

Arrangements with multiple deliverables

In revenue arrangements including more than one deliverable, the deliverables are

assigned to one or more separate units of accounting and the arrangement

consideration is allocated to each unit of accounting based on its relative fair value.

Determining the fair value of each deliverable can require complex estimates due to

the nature of the goods and services provided. The Group generally determines the

fair value of individual elements based on prices at which the deliverable is regularly

sold on a standalone basis after considering volume discounts where appropriate.

Presentation: gross versus net

When deciding the most appropriate basis for presenting revenue or costs of revenue,

both the legal form and substance of the agreement between the Group and

its business partners are reviewed to determine each party’s respective role in

the transaction.

Where the Group’s role in a transaction is that of principal, revenue is recognised on

a gross basis. This requires revenue to comprise the gross value of the transaction

billed to the customer, after trade discounts, with any related expenditure charged

as an operating cost.

Where the Group’s role in a transaction is that of an agent, revenue is recognised on

a net basis with revenue representing the margin earned.

Taxation

The Group’s tax charge on ordinary activities is the sum of the total current and deferred

tax charges. The calculation of the Group’s total tax charge necessarily involves a degree

of estimation and judgement in respect of certain items whose tax treatment cannot

be finally determined until resolution has been reached with the relevant tax authority

or, as appropriate, through a formal legal process. The final resolution of some of these

items may give rise to material profits, losses and/or cash flows.

The complexity of the Group’s structure following its geographic expansion makes

the degree of estimation and judgement more challenging. The resolution of issues

is not always within the control of the Group and it is often dependent on the

efficiency of the legal processes in the relevant taxing jurisdictions in which the

Group operates. Issues can, and often do, take many years to resolve. Payments in

respect of tax liabilities for an accounting period result from payments on account

and on the final resolution of open items. A s a result there can be substantial dif ferences

between the tax charge in the consolidated income statement and tax payments.

Significant items on which the Group has exercised accounting judgement include a

provision in respect of an enquir y from UK HMRC with regard to the CFC tax legislation

(see note 29 to the consolidated financial statements), litigation with the Indian tax

authorities in relation to the acquisition of Vodafone Essar (see note 29 to the

consolidated financial statements) and recognition of a deferred tax asset in respect

of the losses arising following the agreement of German tax loss claims (see note 6

of the consolidated financial statements). The amounts recognised in the

consolidated financial statements in respect of each matter are derived from the

Group’s best estimation and judgement as described above. However the inherent

uncertainty regarding the outcome of these items means eventual resolution could

differ from the accounting estimates and therefore impact the Group’s results and

cash flows.

Critical accounting estimates