Samsung 2005 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2005 Samsung annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

91

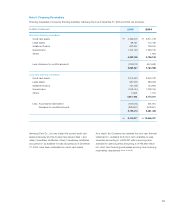

Cash and Cash Equivalents, and Short-Term Financial

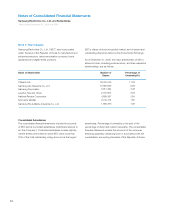

Instruments

Cash and cash equivalents include cash on hand and in bank

accounts, with original maturities of three months or less.

Investments which are readily convertible into cash within

four to 12 months of purchase are classified in the balance

sheet as short-term financial instruments. The cost of these

investments approximates fair value.

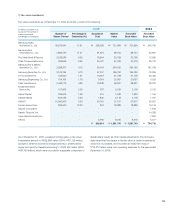

Marketable Securities

Investments in equity securities or debt securities are classi-

fied into trading securities, available-for-sale securities and

held-to-maturity securities, depending on the acquisition and

holding purpose. Trading securities are classified as current

assets; while available-for-sale securities and held-to-maturity

securities are classified as long-term investments, except that

those securities that mature or are certain to be disposed of

within one year are classified as current assets.

Cost is measured at the market value upon acquisition,

including incidental costs, and is determined using the

average cost method.

Available-for-sale securities are stated at fair value, while

non-marketable equity securities are stated at cost.

Unrealized holding gains and losses on available-for-sale

securities are reported in a separate component of shareholders’

equity under capital adjustments, which are to be included

in current operations upon the disposal or impairment of the

securities. In the case of available-for-sale debt securities, the

difference between the acquisition cost after amortization,

using the effective interest rate method, and the fair value is

reported as a capital adjustment.

Impairment resulting from the decline in realizable value below

the acquisition cost, net of amortization, are included in current

operations.

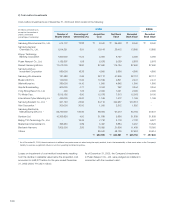

Equity-Method Investments

In the consolidated financial statements of the Company,

investments in business entities in which the Company has

a control or the ability to exercise a significant influence over

the operating and financial policies are accounted for using

the equity method of accounting.

Under the equity method, the original investment is recorded

at cost and adjusted by the Company’s share in the net book

value of the investee with a corresponding charge to current

operations, a separate component of shareholders’ equity, or

retained earnings, depending on the nature of the underlying

change in the net book value. All significant unrealized profits

resulting from inter company transactions of inventories and

property, plant and equipment are fully eliminated.

Differences between the investment account and corresponding

capital account of the investee at the date of acquisition of

the investment are recorded as part of investments and are

amortized over five years using the straight-line method.

However, differences which occur from additional investments

after the Company has significant influence in its investees are

reported in a separate component of shareholders’ equity,

and are not included in the determination of the results of

operations.

Assets and liabilities of the Company’s foreign investees

are translated at current exchange rates, while income and

expenses are translated at average rates for the year. Adjust-

ments resulting from the translation process are reported in

a separate component of shareholders’ equity, and are not

included in the determination of the results of operations.

In accordance with SKFAS No.15, Equity Method, the Com-

pany changed its policy in accounting for the earnings from

equity-method investments from the net basis to gross basis.

This change had no effect on the net income or shareholders’

equity. The financial statements as of December 31, 2004,

and for the year ended December 31, 2004, have not been

restated to reflect such change.

Allowance for Doubtful Accounts

The Company provides an allowance for doubtful accounts

and notes receivable based on the aggregate estimated col-

lectibility of the receivables.

Inventory Valuation

Inventories are stated at the lower of cost or net realizable

value. Cost is determined using the average cost method,

except for materials-in-transit which are stated at actual

cost as determined using the specific identification method.

Losses on valuation of inventories and losses on inventory

obsolescence are recorded as part of cost of sales.

Property, Plant and Equipment and Related Depreciation

Property, plant and equipment are stated at cost, except for

certain assets subject to upward revaluation in accordance

with the Asset Revaluation Law of Korea. The revaluation

presents production facilities and other buildings at their

depreciated replacement cost, and land at the prevailing

market price, as of the effective date of revaluation. The

revaluation increment, net of revaluation tax, is first applied

to offset accumulated deficit and deferred foreign exchange

losses, if any. The remainder may be credited to other capital