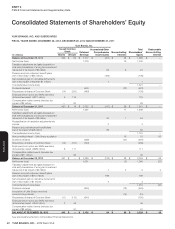

Pizza Hut 2013 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2013 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

YUM! BRANDS, INC.-2013 Form10-K32

Form 10-K

PART II

ITEM7Management’s Discussion and Analysis of Financial Condition and Results of Operations

New Accounting Pronouncements Not Yet Adopted

In March 2013, the Financial Accounting Standards Board (“FASB”) issued

Accounting Standards Update (“ASU”) No. 2013-05, Foreign Currency

Matters, (Topic 830): Parent’s Accounting for the Cumulative Translation

Adjustment upon Derecognition of Certain Subsidiaries or Groups of

Assets within a Foreign Entity or of an Investment in a Foreign Entity

(ASU 2013-05), to resolve a diversity in accounting for the cumulative

translation adjustment of foreign currency upon derecognition of a foreign

subsidiary or group of assets. ASU 2013-05 requires the parent to apply

the guidance in Subtopic 830-30 to release any related cumulative

translation adjustment into net income when a reporting entity (parent)

ceases to have a controlling financial interest in a subsidiary or group

of assets within a foreign entity. Accordingly, the cumulative translation

adjustment should be released into net income only if the sale or transfer

results in the complete or substantially complete liquidation of the foreign

entity in which the subsidiary or group of assets had resided. Further, ASU

2013-05 clarified that the parent should apply the guidance in

Subtopic 810-10 if there is a sale of an investment in a foreign entity, including

both (1) events that result in the loss of a controlling financial interest in

a foreign entity and (2) events that result in an acquirer obtaining control

of an acquiree in which it held an equity interest immediately before the

acquisition date. Accordingly, the cumulative translation adjustment should

be released into net income upon the occurrence of those events. ASU

2013-05 is effective prospectively for the Company in our first quarter of

fiscal 2014. We do not believe the adoption of this standard will have a

significant impact on our consolidated financial statements.

In July 2013, the FASB issued ASU No. 2013-11, Presentation of an

Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a

Similar Tax Loss, or a Tax Credit Carryforward Exists (ASU 2013-11), to

require that in certain cases, an unrecognized tax benefit, or portion of an

unrecognized tax benefit, should be presented in the financial statements

as a reduction to a deferred tax asset for a net operating loss carryforward,

a similar tax loss, or a tax credit carryforward when such items exist in

the same taxing jurisdiction. ASU 2013-11 is effective for the Company

in our first quarter of fiscal 2014. The amendments should be applied

prospectively to all unrecognized tax benefits that exist at the effective

date, and retrospective application is permitted. We do not believe the

adoption of this standard will have a significant impact on our consolidated

financial statements.

Critical Accounting Policies and Estimates

Our reported results are impacted by the application of certain accounting

policies that require us to make subjective or complex judgments. These

judgments involve estimations of the effect of matters that are inherently

uncertain and may significantly impact our quarterly or annual results of

operations or financial condition. Changes in the estimates and judgments

could significantly affect our results of operations, financial condition and

cash flows in future years� A description of what we consider to be our

most significant critical accounting policies follows.

Impairment or Disposal of Long-Lived Assets

We review long-lived assets of restaurants (primarily PP&E and allocated

intangible assets subject to amortization) semi-annually for impairment, or

whenever events or changes in circumstances indicate that the carrying

amount of a restaurant may not be recoverable. We evaluate recoverability

based on the restaurant’s forecasted undiscounted cash flows, which

incorporate our best estimate of sales growth and margin improvement based

upon our plans for the unit and actual results at comparable restaurants�

For restaurant assets that are deemed to not be recoverable, we write

down the impaired restaurant to its estimated fair value� Key assumptions

in the determination of fair value are the future after-tax cash flows of the

restaurant, which are reduced by future royalties a franchisee would pay,

and a discount rate� The after-tax cash flows incorporate reasonable sales

growth and margin improvement assumptions that would be used by a

franchisee in the determination of a purchase price for the restaurant�

Estimates of future cash flows are highly subjective judgments and can be

significantly impacted by changes in the business or economic conditions.

We perform an impairment evaluation at a restaurant group level if it is more

likely than not that we will refranchise restaurants as a group. Expected

net sales proceeds are generally based on actual bids from the buyer,

if available, or anticipated bids given the discounted projected after-tax

cash flows for the group of restaurants� Historically, these anticipated bids

have been reasonably accurate estimations of the proceeds ultimately

received� The after-tax cash flows used in determining the anticipated bids

incorporate reasonable assumptions we believe a franchisee would make

such as sales growth and margin improvement as well as expectations as

to the useful lives of the restaurant assets, including a deduction for the

anticipated, future royalties we would receive under a franchise agreement

with terms substantially at market entered into simultaneously with the

refranchising transaction�

The discount rate used in the fair value calculations is our estimate of the

required rate of return that a franchisee would expect to receive when

purchasing a similar restaurant or groups of restaurants and the related

long-lived assets� The discount rate incorporates rates of returns for

historical refranchising market transactions and is commensurate with the

risks and uncertainty inherent in the forecasted cash flows�

We evaluate indefinite-lived intangible assets for impairment on an annual

basis or more often if an event occurs or circumstances change that indicates

impairment might exist. We perform our annual test for impairment of our

indefinite-lived intangible assets at the beginning of our fourth quarter.

We may elect to perform a qualitative assessment to determine whether

it is more likely than not that the fair value of an indefinite-lived intangible

asset is greater than its carrying value. If a qualitative assessment is not

performed, or if as a result of a qualitative assessment it is not more likely

than not that the fair value of an indefinite-lived intangible asset exceeds

its carrying value, then the asset’s fair value is compared to its carrying

value. Fair value is an estimate of the price a willing buyer would pay for

the intangible asset and is generally estimated by discounting the expected

future after-tax cash flows associated with the intangible asset�

Our most significant indefinite-lived intangible asset is our Little Sheep

trademark. We wrote down the Little Sheep trademark from $414 million

to $345 million as a result of an impairment charge of $69 million recorded

in the quarter ended September 7, 2013. See the Little Sheep Acquisition

and Subsequent Impairment section of Note 4 for details. No additional

indefinite-lived intangible asset impairment was recorded as a result of

our annual testing at the beginning of the fourth quarter.

The fair value of the Little Sheep trademark was based on the estimated

price a willing buyer would pay for the asset, and was determined using

a relief from royalty valuation approach that included future estimated

sales as a significant input. This fair value incorporated a discount rate of

13% as our estimate of the required rate of return that a third-party buyer

would expect to receive when purchasing the Little Sheep trademark.

While future business results are difficult to predict, we believe the decline in

Little Sheep same-store sales and profit that were deemed an impairment

indicator will be reversed over time and significant new unit development

will take place. The inputs used in determining the fair value of the Little

Sheep trademark assumed that the business will recover to pre-acquisition

average unit sales volumes and profit over the next three years. At such

pre-acquisition sales and profit levels, we believe that the Little Sheep