Pizza Hut 2013 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2013 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

YUM! BRANDS, INC.-2013 Form10-K 19

Form 10-K

PART II

ITEM7Management’s Discussion and Analysis of Financial Condition and Results of Operations

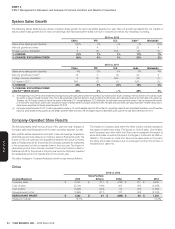

Restaurant Margin by 0.4 percentage points and did not have a significant

impact on China Division Operating Profit versus 2011.

The purchase price paid for the additional 66% interest and the resulting

purchase price allocation assumed same-store sales growth and new

unit development for the brand. As a result of consolidating Little Sheep,

the primary assets recorded in 2012 were an indefinite-lived Little Sheep

trademark and goodwill of approximately $400 million and $375 million,

respectively. The goodwill was assigned to the newly formed Little Sheep

reporting unit within our China Division.

Little Sheep’s sales were negatively impacted by a longer than expected

purchase approval and ownership transition phase. Our efforts to regain

sales momentum were significantly compromised in May 2013 due to

negative publicity regarding quality issues with unrelated hot pot concepts

in China, even though there was not an issue with the quality of Little

Sheep products.

While we remain confident in the long-term potential of Little Sheep,

the sustained declines in sales and profits that began in May 2013 and

continued through the third quarter, coupled with the anticipated time it will

now take for the business to recover, resulted in a determination during the

quarter ended September7, 2013 that it was not more likely than not that

the Little Sheep trademark and reporting unit fair values were in excess of

their carrying values. Therefore, our Little Sheep trademark and goodwill

were tested for impairment in the quarter ended September7, 2013, prior

to the annual impairment reviews performed in the fourth quarter of each

year in accordance with our accounting policy.

As a result of comparing the trademark’s fair value of $345 million to

its carrying value of $414 million, an impairment charge of $69 million

was recorded. Additionally, after determining the fair value of the Little

Sheep reporting unit was less than its carrying value, goodwill was

written down to $162 million, resulting in an impairment charge of

$222 million. The Company also evaluated other Little Sheep long-lived

assets for impairment and recorded a $4 million impairment charge related

to restaurant-level PP&E.

These non-cash impairment charges totalling $295 million were recorded

in Closures and impairment (income) expense on our Consolidated

Statement of Income. We recorded an $18 million tax benefit associated

with these impairments and allocated $19 million of the after-tax impairment

charges to Net Income (loss) - noncontrolling interests, which resulted in

a net impairment charge of $258 million allocated to Net Income - YUM!

Brands, Inc.

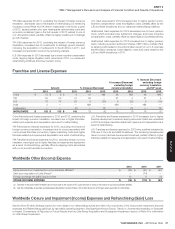

Losses Associated With the Refranchising of the Pizza

Hut UK Dine-in Business

During the fourth quarter of 2012, we refranchised our remaining

331 Company-owned Pizza Hut dine-in restaurants in the United Kingdom

(“UK”). The franchise agreement for these stores allows the franchisee

to pay continuing franchise fees in the initial years of the agreement at a

reduced rate. We agreed to allow the franchisee to pay these reduced fees

in part as consideration for their assumption of lease liabilities related to

underperforming stores that we anticipate they will close that were part of

the refranchising. We recognize the estimated value of terms in franchise

agreements entered into concurrently with a refranchising transaction that

are not consistent with market terms as part of the upfront refranchising

gain (loss). Accordingly, upon the closing of this refranchising in the

fourth quarter of 2012, we recognized a loss of $53 million representing

the estimated value of these reduced continuing fees. The associated

deferred credit is being amortized into YRI’s Franchise and license fees

and income through 2016. This upfront loss largely contributed to a

$70million Refranchising loss we recognized in Special Items during

2012, net of income tax benefits of $9 million. During 2011, we recorded

a $76million charge in Refranchising gain (loss) as a result of our decision

to refranchise or close all of the remaining Company-owned Pizza Hut UK

dine-in restaurants, primarily to write down these restaurants’ long-lived

assets to their then estimated fair value.

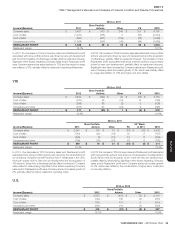

For the year ended December 28, 2013, the refranchising of the Pizza Hut

UK dine-in restaurants decreased Company sales by 18% and increased

Franchise and license fees and income and Operating Profit by 2% and

3%, respectively, for the YRI Division versus 2012.

Losses and Other Costs Relating to the LJS and A&W

Divestitures

In 2011, we sold the Long John Silver’s and A&W All American Food

Restaurants brands to key franchise leaders and strategic investors in

separate transactions. We recognized $86 million of losses and other costs

primarily in Closures and impairment (income) expenses as a result of our

decision to sell these businesses. Additionally, we recognized $104million

of tax benefits related to these divestitures. In 2012 as compared to 2011,

System sales and Franchise and license fees and income in the U.S. were

negatively impacted by 5% and 6%, respectively, due to these divestitures

while YRI’s system sales and Franchise and license fees and income

were both negatively impacted by 1%. While these divestitures negatively

impacted both the U.S. and YRI segments’ Operating Profit by 1% in

2012, the impact on our consolidated Operating Profit was not significant.

Other Special Items Income (Expense)

In connection with the aforementioned refranchising of stores in the U.S.,

we have taken several measures to transform our U.S. business, including

G&A productivity initiatives and realignment of resources (primarily severance

and early retirement costs). Other Special Items Income (Expense) in

2013 includes charges relating to these U.S. G&A productivity initiatives

and realignment of resources of $5 million as well as $2 million of costs

recorded in G&A that were part of the $120 million charge related to the

extinguishment of debt. Other Special Items Income (Expense) in 2012

includes the depreciation reduction from the Pizza Hut UK and KFC

U.S. restaurants impaired upon our decision or offer to refranchise that

remained Company stores for some or all of the periods presented of

$13million and $3 million, respectively, gains from real estate sales related

to our previously refranchised Mexico business of $3 million and charges

relating to U.S. G&A productivity initiatives and realignment of resources

of $5 million. Other Special Items Income (Expense) in 2011 includes the

depreciation reduction from the Pizza Hut UK and KFC U.S. restaurants

impaired upon our decision or offer to refranchise that remained Company

stores for some or all of the periods presented of $3 million and $10 million,

respectively, and charges relating to U.S. G&A productivity initiatives and

realignment of resources of $21 million.

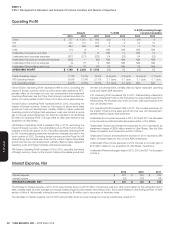

Losses Related to the Extinguishment of Debt

During the fourth quarter of 2013, we completed a cash tender offer to

repurchase $550 million of our Senior Unsecured Notes due either March

2018 or November 2037. This transaction resulted in $120 million of losses

as a result of premiums paid and other costs, $118 million of which was

classified as Interest expense, net in our Consolidated Statement of Income.

The repurchase of the Senior Unsecured Notes was funded primarily

by proceeds of $599 million received from the issuance of new Senior

Unsecured Notes. See Note 10 for further discussion on the issuance of

Senior Unsecured Notes.

China Poultry Supply Incident and Avian Flu

In late December 2012 our KFC China sales began to be negatively

impacted by intense media attention surrounding an investigation by

the Shanghai FDA (SFDA) into poultry supply management at our

China Division. In January 2013 the SFDA concluded its investigation

and released its recommendations to Yum! China. During 2013 our

team in China undertook a comprehensive review of our supply chain,

incorporated the SFDA’s recommendations and, as part of our commitment

to quality, took additional steps to further strengthen our overall poultry

supply chain practices, including increased testing of product received