Pizza Hut 2013 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2013 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

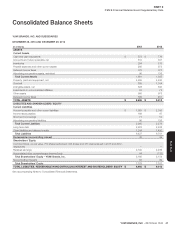

YUM! BRANDS, INC.-2013 Form10-K 31

Form 10-K

PART II

ITEM7Management’s Discussion and Analysis of Financial Condition and Results of Operations

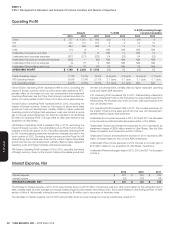

The majority of our remaining long-term debt primarily comprises Senior

Unsecured Notes with varying maturity dates from 2014 through 2043

and interest rates ranging from 2.38% to 6.88%. The Senior Unsecured

Notes represent senior, unsecured obligations and rank equally in right

of payment with all of our existing and future unsecured unsubordinated

indebtedness. Amounts outstanding under Senior Unsecured Notes

were $2.8 billion at December 28, 2013. Our Senior Unsecured Notes

provide that the acceleration of the maturity of any of our indebtedness in

a principal amount in excess of $50 million will constitute a default under

the Senior Unsecured Notes if such acceleration is not annulled, or such

indebtedness is not discharged, within 30 days after notice.

During the fourth quarter of 2013, we issued $325 million aggregate principal

amount of 3.88% 10 year Senior Unsecured Notes and $275million

aggregate principal amount of 5.35% 30 year Senior Unsecured Notes.

We used the proceeds from our issuances of these Senior Unsecured

Notes in part to repurchase certain of our Senior Unsecured Notes due

March 2018 and November 2037 with principal amounts of $275 million

each totaling $550 million. See Significant Known Events, Trends or

Uncertainties Impacting or Expected to Impact Comparisons of Reported

or Future Results and Note 10 for information on the Repurchase of those

Senior Unsecured Notes.

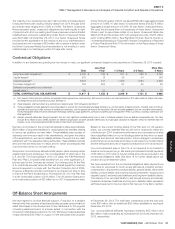

Contractual Obligations

In addition to any discretionary spending we may choose to make, our significant contractual obligations and payments as of December 28, 2013 included:

Total

Less than

1 Year 1-3 Years 3-5 Years

More than

5 Years

Long-term debt obligations(a) $ 4,300 $ 186 $ 791 $ 529 $ 2,794

Capital leases(b) 276 18 38 34 186

Operating leases(b) 5,697 721 1,299 1,084 2,593

Purchase obligations(c) 784 604 87 55 38

Deferred compensation and unfunded

benefit plans(d) 160 21 33 29 77

TOTAL CONTRACTUAL OBLIGATIONS $ 11,217 $ 1,550 $ 2,248 $ 1,731 $ 5,688

(a) Debt amounts include principal maturities and expected interest payments on a nominal basis. Debt amounts exclude a fair value adjustment of $14 million related to interest rate swaps

that hedge the fair value of a portion of our debt. See Note 10.

(b) These obligations, which are shown on a nominal basis, relate to nearly 7,300 restaurants. See Note 11.

(c) Purchase obligations include agreements to purchase goods or services that are enforceable and legally binding on us and that specify all significant terms, including: fixed or minimum

quantities to be purchased; fixed, minimum or variable price provisions; and the approximate timing of the transaction. We have excluded agreements that are cancelable without penalty.

Purchase obligations relate primarily to information technology, marketing, supply agreements, purchases of property, plant and equipment (“PP&E”) as well as consulting, maintenance and

other agreements.

(d) Includes actuarially determined timing of payments from our most significant unfunded pension plan as well as scheduled payments from our deferred compensation plan. This table

excludes $113 million of future benefit payments for deferred compensation and other unfunded benefit plans to be paid upon separation of employee’s service or retirement from the

company, as we cannot reasonably estimate the dates of these future cash payments.

We have not included in the contractual obligations table approximately

$224 million of long-term liabilities for unrecognized tax benefits relating

to various tax positions we have taken. These liabilities may increase or

decrease over time as a result of tax examinations, and given the status

of the examinations, we cannot reliably estimate the period of any cash

settlement with the respective taxing authorities. These liabilities exclude

amounts that are temporary in nature and for which we anticipate that

over time there will be no net cash outflow.

We sponsor noncontributory defined benefit pension plans covering certain

salaried and hourly employees, the most significant of which are in the

U.S. and UK. The most significant of the U.S. plans, the YUM Retirement

Plan (the “Plan”), is funded while benefits from our other significant U.S.

plan are paid by the Company as incurred. Our funding policy for the Plan

is to contribute annually amounts that will at least equal the minimum

amounts required to comply with the Pension Protection Act of 2006.

However, additional voluntary contributions are made from time to time

to improve the Plan’s funded status. At December 28, 2013 the Plan was

in a net overfunded position of $10 million. The UK pension plans are in

a net overfunded position of $33 million at our 2013 measurement date.

Based on the current funding status of the Plan and our UK pension

plans, we currently estimate that we will not be required to make any

contributions in 2014. Investment performance and corporate bond rates

have a significant effect on our net funding position as they drive our asset

balances and discount rate assumption. Future changes in investment

performance and corporate bond rates could impact our funded status

and the timing and amounts of required contributions in 2014 and beyond.

Our post-retirement plan in the U.S. is not required to be funded in

advance, but is pay as you go. We made post-retirement benefit payments

of $7 million in 2013 and no future funding amounts are included in the

contractual obligations table. See Note 14 for further details about our

pension and post-retirement plans.

We have excluded from the contractual obligations table payments we

may make for exposures for which we are self-insured, including workers’

compensation, employment practices liability, general liability, automobile

liability, product liability and property losses (collectively “property and

casualty losses”) and employee healthcare and long-term disability claims.

The majority of our recorded liability for self-insured property and casualty

losses and employee healthcare and long-term disability claims represents

estimated reserves for incurred claims that have yet to be filed or settled.

Off-Balance Sheet Arrangements

We have agreed to provide financial support, if required, to a variable

interest entity that operates a franchisee lending program used primarily to

assist franchisees in the development of new restaurants or the upgrade

of existing restaurants and, to a lesser extent, in connection with the

Company’s refranchising programs in the U.S. We have provided guarantees

of approximately $35 million in support of the franchisee loan program

at December 28, 2013. The total loans outstanding under the loan pool

were $38 million with an additional $42 million available for lending at

December 28, 2013.

Our unconsolidated affiliates had approximately $85 million and

$60 million of debt outstanding as of December 28, 2013 and December 29,

2012, respectively.