Nokia 2004 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2004 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195

|

|

Notes to the Consolidated Financial Statements (Continued)

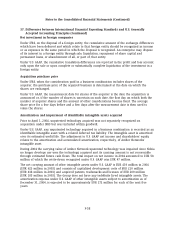

37. Differences between International Financial Reporting Standards and U.S. Generally

Accepted Accounting Principles (Continued)

Pension expense

Under IFRS, the determination of pension expense for defined benefit plans differs from the

methodology set forth in U.S. GAAP. For purposes of U.S. GAAP, the Group has estimated the effect

on net income and shareholders’ equity assuming the application of SFAS No. 87 in calculating

pension expense as of January 1, 1992.

The Group uses December 31 as the measurement date for its pension plans.

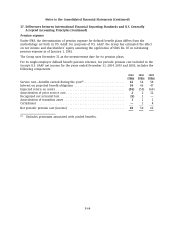

For its single-employer defined benefit pension schemes, net periodic pension cost included in the

Group’s U.S. GAAP net income for the years ended December 31, 2004, 2003 and 2002, includes the

following components:

2004 2003 2002

EURm EURm EURm

Service cost—benefits earned during the year(1) ........................ 62 54 58

Interest on projected benefit obligation .............................. 56 46 47

Expected return on assets ......................................... (56) (55) (60)

Amortization of prior service cost ................................... 2212

Recognized net actuarial loss ....................................... (5) 1—

Amortization of transition asset .................................... 111

Curtailment .................................................... —14

Net periodic pension cost (income) .................................. 60 50 62

(1) Excludes premiums associated with pooled benefits.

F-64