Nokia 2004 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2004 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

|

|

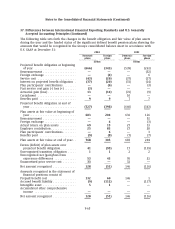

Notes to the Consolidated Financial Statements (Continued)

37. Differences between International Financial Reporting Standards and U.S. Generally

Accepted Accounting Principles (Continued)

Earnings per share under U.S. GAAP:

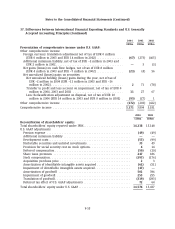

Earnings per share amounts are presented below:

2004 2003 2002

EUR EUR EUR

Earnings per share (net income):

Basic ........................................................ 0.73 0.86 0.76

Diluted ...................................................... 0.73 0.86 0.75

Pension expense and additional minimum liability

Under IFRS, pension assets, defined benefit pension liabilities and expense are actuarially

determined in a similar manner to U.S. GAAP. However, under IFRS the prior service cost,

transition adjustments and expense resulting from plan amendments are generally recognized

immediately. Under U.S. GAAP, these expenses are generally recognized over a longer period. Also,

under U.S. GAAP the employer should recognize an additional minimum pension liability charged

to other comprehensive income when the accumulated benefit obligation (ABO) exceeds the fair

value of the plan assets and this amount is not covered by the liability recognized in the balance

sheet. The calculation of the ABO is based on approach two as described in EITF 88-1,

Determination of Vested Benefit Obligation for a Defined Benefit Pension Plan, under which the

actuarial present value is based on the date of separation from service.

The U.S. GAAP pension adjustment reflects the difference between the prepaid pension asset and

related pension expense as determined by applying IAS 19, Employee Benefits, and the pension

asset and pension expense determined by applying FAS 87, Employers’ Accounting for Pensions.

Development costs

Development costs have been capitalized under IFRS after the product involved has reached a

certain degree of technical feasibility. Capitalization ceases and depreciation begins when the

product becomes available to customers. The depreciation period of these capitalized assets is

between two and five years.

Under U.S. GAAP, software development costs would similarly be capitalized after the product has

reached a certain degree of technical feasibility. However, certain non-software related

development costs capitalized under IFRS would not be capitalizable under U.S. GAAP and

therefore would have been expensed under U.S. GAAP.

Under IFRS, whenever there is an indication that capitalized development costs may be impaired

the recoverable amount of the asset is estimated. An asset is impaired when the carrying amount

of the asset exceeds its recoverable amount. Recoverable amount is defined as the higher of an

asset’s net selling price and value in use. Value in use is the present value of estimated discounted

future cash flows expected to arise from the continuing use of an asset and from its disposal at

the end of its useful life.

Under U.S. GAAP, the unamortized capitalized costs of a computer software product is compared at

each balance sheet date to the net realizable value of that product with any excess written off. Net

realizable value is defined as the estimated future gross revenues from that product reduced by

the estimated future costs of completing and disposing of that product, including the costs of

F-56