Nokia 2004 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2004 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

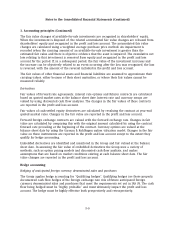

Notes to the Consolidated Financial Statements (Continued)

1. Accounting principles (Continued)

The Group adopted the transition provisions of IFRS 3, Business Combinations, with effect from

April 1, 2004. As a result, goodwill relating to purchase acquisitions and acquisitions of associated

companies for which the agreement date was on or after March 31, 2004, is no longer subject to

amortization. Goodwill arising in business combinations completed before March 31, 2004 will

continue to be amortized until the standard is fully adopted as of January 1, 2005.

The Group assesses the carrying value of goodwill annually or, more frequently, if events or

changes in circumstances indicate that such carrying value may not be recoverable. If such

indication exists the recoverable amount is determined for the cash-generating unit, to which

goodwill belongs. This amount is then compared to the carrying amount of the cash-generating

unit and an impairment loss is recognized if the recoverable amount is less than the carrying

amount. Impairment losses are recognized immediately in the profit and loss account.

Transactions in foreign currencies

Transactions in foreign currencies are recorded at the rates of exchange prevailing at the dates of

the individual transactions. For practical reasons, a rate that approximates the actual rate at the

date of the transaction is often used. At the end of the accounting period, the unsettled balances

on foreign currency receivables and liabilities are valued at the rates of exchange prevailing at the

year-end. Foreign exchange gains and losses related to normal business operations are treated as

adjustments to sales or to cost of sales. Foreign exchange gains and losses associated with

financing are included as a net amount under financial income and expenses.

Foreign Group companies

In the consolidated accounts all items in the profit and loss accounts of foreign subsidiaries are

translated into euro at the average foreign exchange rates for the accounting period. The balance

sheets of foreign Group companies are translated into euro at the year-end foreign exchange rates

with the exception of goodwill arising on the acquisition of a foreign company, which is

translated to euro at historical rates. Differences resulting from the translation of profit and loss

account items at the average rate and the balance sheet items at the closing rate are also treated

as an adjustment affecting consolidated shareholders’ equity. On the disposal of all or part of a

foreign Group company by sale, liquidation, repayment of share capital or abandonment, the

cumulative amount or proportionate share of the translation difference is recognized as income or

as expense in the same period in which the gain or loss on disposal is recognized.

Fair valuing principles

Financial assets and liabilities

Under IAS 39, the Group classifies its investments in marketable debt and equity securities and

investments in unlisted equity securities into the following categories: held-to-maturity, trading, or

available-for-sale depending on the purpose for acquiring the investments. All investments of the

Group are currently classified as available-for-sale. Available-for-sale investments are fair valued

by using quoted market rates, discounted cash flow analyses and other appropriate valuation

models at the balance sheet date. Certain unlisted equities for which fair values cannot be

measured reliably are reported at cost less impairment. All purchases and sales of investments are

recorded on the trade date, which is the date that the Group commits to purchase or sell the asset.

F-8