Lenovo 2015 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2015 Lenovo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

147

2014/15 Annual Report Lenovo Group Limited

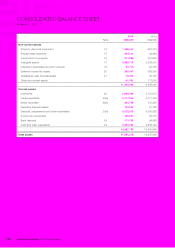

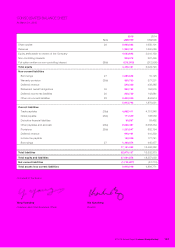

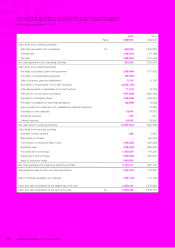

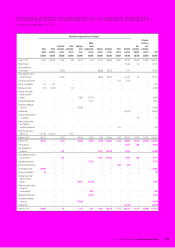

NOTES TO THE FINANCIAL STATEMENTS

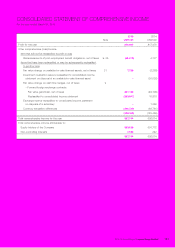

2 SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies adopted in the preparation of these financial statements are set out below. These policies

have been consistently applied to all the years presented, unless otherwise stated.

(a) Subsidiaries

(i) Consolidation

The consolidated financial statements include the financial statements of the Company and all of its subsidiaries

made up to March 31.

Subsidiaries are all entities (including structured entities) over which the Group is exposed to, or has rights to,

variable returns from its involvement with the entity and has the ability to affect those returns through its power

over the entity generally accompanying a shareholding of more than one half of the voting rights. The existence

and effect of potential voting rights that are currently exercisable or convertible are considered when assessing

whether the Group controls another entity. The Group also assesses existence of control where it does not have

more than 50% of the voting power but is able to govern the financial and operating policies by virtue of de-facto

control. De-facto control may arise from circumstances where it does not have more than 50% of the voting power

but is able to govern the financial and operating policies by virtue of de-facto control such as enhanced minority

rights or contractual terms between shareholders, etc.

Subsidiaries are fully consolidated from the date on which control is transferred to the Group. They are de-

consolidated from the date that control ceases.

Inter-company transactions, balances, income and expenses on transactions are eliminated. Profits and losses

resulting from inter-company transactions that are recognized in assets are also eliminated.

Adjustments have been made to the financial statements of subsidiaries when necessary to align their accounting

policies to ensure consistency with the policies adopted by the Group.

For subsidiaries which adopted December 31 as their financial year end date for statutory reporting purposes,

their financial statements for the years ended March 31, 2014 and 2015 have been used for the preparation of the

Group’s consolidated financial statements.

(ii) Business combinations

The Group applies the acquisition method to account for business combinations. The consideration transferred

for the acquisition of a subsidiary is the fair values of the assets transferred, the liabilities incurred to the former

owners of the acquiree and the equity interests issued by the Group. The consideration transferred includes the

fair value of any asset or liability resulting from a contingent consideration arrangement. Identifiable assets acquired

and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values

at the acquisition date. The Group recognizes any non-controlling interest in the acquiree on an acquisition-by-

acquisition basis, either at fair value or at the non-controlling interest’s proportionate share of the recognized

amounts of acquiree’s identifiable net assets.

Acquisition-related costs are expensed as incurred.

If the business combination is achieved in stages, the acquirer’s previously held equity interest in the acquiree

is re-measured to fair value at the acquisition date; any gains or losses arising from such re-measurement are

recognized in profit or loss.

Any contingent consideration to be transferred by the Group is recognized at fair value at the acquisition date.

Subsequent changes to the fair value of the contingent consideration that is deemed to be an asset or liability

is recognized in the consolidated income statement or as a change to other comprehensive income. Contingent

consideration that is classified as equity is not re-measured, and its subsequent settlement is accounted for within

equity.

Goodwill is initially measured as the excess of the aggregate of the consideration transferred, the amount of any

non-controlling interest in the acquiree and, in a business combination achieved in stages the acquisition-date fair

value of any previous equity interest in the acquiree over the net identifiable assets acquired and liabilities assumed

(Note 2(g)(i)). If it is less than the fair value of the net assets of the subsidiary acquired, the difference is recognized

directly in the consolidated income statement.