IBM 2004 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2004 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

International Business Machines Corporation and Subsidiary Companies

66

ibm annual report 2004

long-term investments in foreign subsidiaries (net investment)

A significant portion of the company’s foreign currency denominated debt portfolio is

designated as a hedge of net investment to reduce the volatility in stockholders’ equity

caused by changes in foreign currency exchange rates in the functional currency of major

foreign subsidiaries with respect to the U.S. dollar. The company also uses currency swaps

and foreign exchange forward contracts for this risk management purpose. The currency

effects of these hedges (approximately $156 million in 2004 and approximately $200 mil-

lion in 2003, net of tax) are reflected as a loss in the Accumulated gains and (losses) not

affecting retained earnings section of the Consolidated Statement of Stockholders’ Equity,

thereby offsetting a portion of the translation adjustment of the applicable foreign sub-

sidiaries’ net assets.

anticipated royalties and cost transactions

The company’s operations generate significant nonfunctional currency, third-party vendor

payments and intercompany payments for royalties, and goods and services among the

company’s non-U.S. subsidiaries and with the parent company. In anticipation of these

foreign currency cash flows and in view of the volatility of the currency markets, the com-

pany selectively employs foreign exchange forward and option contracts to manage its

currency risk. In general, these hedges have maturities of one year or less, but from time

to time extend beyond one year commensurate with the underlying hedged anticipated

cash flow. At December 31, 2004, the weighted-average remaining maturity of these

derivative instruments was approximately one year.

subsidiary cash and foreign currency asset/liability management

The company uses its Global Treasury Centers to manage the cash of its subsidiaries.

These centers principally use currency swaps to convert cash flows in a cost-effective

manner. In addition, the company uses foreign exchange forward contracts to hedge, on

a net basis, the foreign currency exposure of a portion of the company’s nonfunctional cur-

rency assets and liabilities. The terms of these forward and swap contracts are generally

less than one year. The changes in fair value from these contracts and from the underlying

hedged exposures are generally offsetting and are recorded in Other (income) and

expense in the Consolidated Statement of Earnings.

equity risk management

The company is exposed to certain equity price changes related to certain obligations to

employees. These equity exposures are primarily related to market value movements in

certain broad equity market indices and in the company’s own stock. Changes in the over-

all value of this employee compensation obligation are recorded in SG&A expense in the

Consolidated Statement of Earnings. Although not designated as accounting hedges, the

company utilizes equity derivatives, including equity swaps and futures to economically

hedge the equity exposures relating to this employee compensation obligation. To match

the exposures relating to this employee compensation obligation, these derivatives are

linked to the total return of certain broad equity market indices and/or the total return of

the company’s common stock. These derivatives are recorded at fair value with gains or

losses also reported in SG&A expense in the Consolidated Statement of Earnings.

other derivatives

The company holds warrants in connection with certain investments that, although not

designated as hedging instruments, are deemed derivatives since they contain net share

settlement clauses. During the year, the company recorded the change in the fair value of

these warrants in net income.

The company is exposed to a potential loss if a client fails to pay amounts due the

company under contractual terms (“credit risk”). The company has established policies and

procedures for mitigating credit risk on principal transactions, including reviewing and estab-

lishing limits for credit exposure, maintaining collateral, and continually assessing the credit-

worthiness of counterparties. Master agreements with counterparties include master netting

arrangements as further mitigation of credit exposure to counterparties. These arrangements

permit the company to net amounts due from the company to a counterparty with amounts

due to the company from a counterparty reducing the maximum loss from credit risk in the

event of counterparty default. Also, in 2003, the company began utilizing credit default swaps

to economically hedge certain credit exposures. These derivatives have terms of two years.

The swaps are not designated as accounting hedges and are recorded at fair value with

gains and losses reported in SG&A expense in the Consolidated Statement of Earnings.

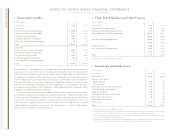

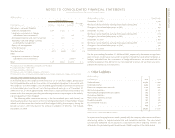

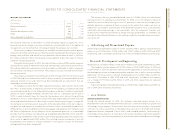

The following table and the table on page 67 summarize the net fair value of the

company’s derivative and other risk management instruments at December 31, 2004 and

2003 (included in the Consolidated Statement of Financial Position).

risk management program

(Dollars in millions)

Hedge Designation

Net Non-Hedge/

AT DECEMBER 31, 2004 Fair Value Cash Flow Investment Other

Derivatives—net asset/(liability):

Debt risk management $«221 $«««(53) $«««««««— $«(14)

Long-term investments in foreign

subsidiaries (net investments) — — (58) —

Anticipated royalties and

cost transactions — (939) — —

Subsidiary cash and foreign currency

asset/liability management — — — (19)

Equity risk management ——— (7)

Total derivatives 221(a) (992) (b) (58) (c) (40) (d)

Debt:

Long-term investments in foreign

subsidiaries (net investments) — — (2,490) (e) —

Total $«221 $«(992) $«(2,548) $«(40)

(a) Comprises assets of $440 million and liabilities of $219 million.

(b) Comprises assets of $12 million and liabilities of $1,004 million.

(c) Comprises liabilities of $58 million.

(d) Comprises assets of $60 million and liabilities of $100 million.

(e) Represents fair value of foreign denominated debt issuances formally designated as a hedge of net investment.