IBM 2004 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2004 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

02

chairman’s letter

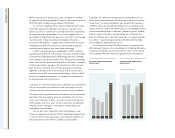

We were able to achieve these results because of our

performance in the marketplace.

•IBM Global Services is the leading IT services company in

the world, with more than twice the revenue of our nearest

rival. We are ranked number one in IT outsourcing, application

management and e-business hosting. In 2004, Global Services

revenue grew 8percent to $46.2 billion, driven by continued

growth in Strategic Outsourcing, as well as revenue increases

in Integrated Technology Services and Business Consulting

Services (led by strong growth in Business Transformation

Outsourcing). Although signings and backlog declined in

2004, Global Services improved its rate of revenue growth in

every quarter, excluding the benefit of currency, due to the

improving yield of our backlog and current signings.

•Our software revenue totaled $15.1 billion, an increase

of 5percent. We gained share in key segments and held our

leading share position in middleware overall. WebSphere

grew 14 percent, Rational 15 percent and Tivoli 15 percent.

•We continue as number one in the world in servers, with

zSeries, pSeries and xSeries each increasing its share position

in 2004.IBM is the market leader in the super-hot category of

blade servers, with revenue growing more than 150 percent

for the year. Industry analyst IDC estimates that by 2008

one of every four servers will be a blade. We had challenging

product transitions in storage systems and iSeries, which

hurt us. Personal computer revenue growth was strong for

the year. Technology OEM growth was good, and we continue

to see yield improvements in our semiconductor operation.

Overall, our hardware revenue was $31.2 billion, an increase

of 10 percent.

•Revenue in all of IBM’s industry sectors— which is the way

we serve our largest clients globally—grew for the full year,

led by the financial services, communications and distribution

sectors. We continued our strong growth in sales to small and

medium-size businesses, which grew by 8percent.

•We grew and expanded our business in the world’s hyper-

growth markets. We have learned over many years that the

best way to pursue opportunities in emerging markets is to

make investments and build relationships for the long haul,

to become part of the local economy and to help advance

the society’s broader goals. We are doing that in China,

India, Brazil and Russia— and it’s yielding good results. IBM’s

business in these four key emerging markets grew more than

25 percent in 2004, to more than $4billion.

The year had its share of challenges, and some parts of

the business fell short. But overall, it was a solid year for the

IBM company. The results confirm that we are in the right

businesses and the right segments of the industry.

A transaction and a transformation

Of course, just as significant as the segments we are in are

those we are not. The industry’s contraction in recent years

has forced IT companies to choose between being high-

value innovation players or high-volume distributors of other

people’s intellectual capital. Companies that are caught

in the middle run the risk of being hammered from both

below and above.

As I described to you last year, we’ve made our choice: IBM

is an innovation company. Of course, declaring something like

that is easy. It has taken a great deal of discipline to execute.

For instance, over the past several years, while we increased

our presence in software, consulting and infrastructure serv-

ices, we exited or reduced our presence in commoditizing

businesses like hard disk drives, memory chips and network-

ing hardware. And most notably, this past December we

announced our agreement for Lenovo, China’s computer

leader, to acquire IBM’s Personal Computing Division.

These kinds of decisions are hard for many companies—

indeed, some won’t make them—because it means parting

with business models and technologies that were once their

crown jewels. In our own case, IBM invented the hard disk drive

and DRAM chip, and we set the standard in PCs back in 1981.