IBM 2004 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2004 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

57

International Business Machines Corporation and Subsidiary Companies

ibm annual report 2004

In April 2003, the FASB issued SFAS No. 149, “Amendment of Statement 133 on

Derivative Instruments and Hedging Activities.” SFAS No. 149 clarifies under what circum-

stances a contract with an initial net investment meets the characteristics of a derivative as

discussed in SFAS No. 133. It also specifies when a derivative contains a financing compo-

nent that requires special reporting in the Consolidated Statement of Cash Flows. SFAS

No. 149 amends certain other existing pronouncements in order to improve consistency in

reporting these types of transactions. The new guidance was effective for contracts entered

into or modified after June 30, 2003, and for hedging relationships designated after

June 30, 2003. SFAS No. 149 did not have a material effect on the company’s Consolidated

Financial Statements.

In November 2002, the FASB issued Interpretation No. 45 (FIN 45), “Guarantor’s

Accounting and Disclosure Requirements for Guarantees, Including Indirect Guarantees

of Indebtedness of Others,” which addresses the disclosures to be made by a guarantor

in its interim and annual financial statements about its obligations under guarantees.

FIN 45 also requires the recognition of a liability by a guarantor at the inception of certain

guarantees that are entered into or modified after December 31, 2002. The company

adopted the disclosure requirements of FIN 45 (see note a, “Significant Accounting

Policies,” on page 55 under “Product Warranties,” and note o, “Contingencies and Commit-

ments,” on page 71) and applied the recognition and measurement provisions for all

material guarantees entered into or modified in periods beginning January 1, 2003. The

adoption of the recognition and measurement provisions of FIN 45 did not have a mate-

rial impact on the company’s Consolidated Financial Statements. The impact of FIN 45 on

the company’s future Consolidated Financial Statements will depend upon whether the

company enters into or modifies any material guarantee arrangements.

In July 2002, the FASB issued SFAS No. 146, “Accounting for Costs Associated with Exit

or Disposal Activities.” SFAS No. 146 supersedes EITF No. 94-3, “Liability Recognition for

Certain Employee Termination Benefits and Other Costs to Exit an Activity (Including

Certain Costs Incurred in a Restructuring),” and requires that a liability for a cost associated

with an exit or disposal activity be recognized when the liability is incurred. Such liabilities

should be recorded at fair value and updated for any changes in the fair value each

period. The company adopted this statement effective January 1, 2003, and its adoption

did not have a material effect on the Consolidated Financial Statements. Going forward,

the impact of SFAS No. 146 on the company’s Consolidated Financial Statements will

depend upon the timing of and facts underlying any future exit or disposal activity.

In April 2002, the FASB issued SFAS No. 145, “Rescission of FASB Statements No. 4, 44

and 64, Amendment of FASB Statement No. 13, and Technical Corrections,” effective May 15,

2002. SFAS No. 145 eliminates the requirement that gains and losses from the extinguish-

ment of debt be aggregated and classified as an extraordinary item, net of tax, and makes

certain other technical corrections. SFAS No. 145 did not have a material effect on the

company’s Consolidated Financial Statements.

On January 1, 2003, the company adopted SFAS No. 143, “Accounting for Asset

Retirement Obligations,” which was issued in June 2001. SFAS No. 143 provides accounting

and reporting guidance for legal obligations associated with the retirement of long-lived

assets that result from the acquisition, construction or normal operation of a long-lived

asset. SFAS No. 143 requires the recording of an asset and a liability equal to the present

value of the estimated costs associated with the retirement of long-lived assets for which

a legal or contractual obligation exists. The asset is required to be depreciated over the

life of the related equipment or facility, and the liability is required to be accreted each

year based on a present value interest rate. The adoption of the standard did not have a

material effect on the company’s Consolidated Financial Statements.

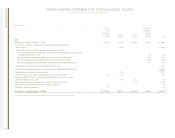

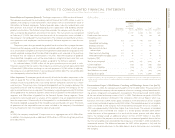

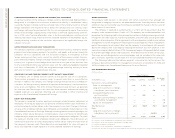

c. Acquisitions/Divestitures

acquisitions

2004

In 2004, the company completed 14 acquisitions at an aggregate cost of $2,111 million.

(Dollars in millions)

Candle

Original

Amount

Disclosed in

Amortization Second Purchase Total Other

Life (in Years) Qtr. 2004 Adjustments* Allocation Maersk Acquisitions

Current assets $«202 $««(2) $«200 $«319 $«««191

Fixed assets/non-current 82 (19) 63 123 176

Intangible assets:

Goodwill NA 256 39 295 426 711

Completed technology 2–3 23 — 23 11 29

Client relationships 3–765—6510050

Other identifiable

intangible assets 56—6213

Total assets acquired 634 18 652 981 1,170

Current liabilities (119) (22) (141) (145) (198)

Non-current liabilities (80) — (80) (44) (84)

Total liabilities assumed (199) (22) (221) (189) (282)

Total purchase price $«435 $««(4) $«431 $«792 $«««888

*Adjustments primarily relate to acquisition costs, deferred taxes and other accruals.