IBM 2004 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2004 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

MANAGEMENT DISCUSSION

International Business Machines Corporation and Subsidiary Companies

39

ibm annual report 2004

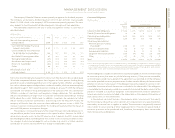

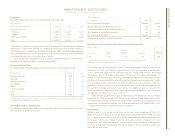

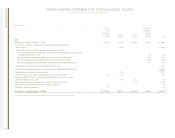

return on equity

(Dollars in millions)

AT DECEMBER 31: 2004 2003

Numerator:

Global Financing after tax income (A)*$÷««937 $««««766

Denominator:

Average Global Financing equity (B)** $«3,272 $«3,436

Global Financing Return on Equity (A)/(B) 28.6% 22.3%

*Calculated based upon an estimated tax rate principally based on Global Financing’s geographic mix of earnings as

IBM’s provision for income taxes is determined on a consolidated basis.

** Average of the ending equity for Global Financing for the last five quarters.

critical accounting estimates

As discussed in note a, “Significant Accounting Policies,” on page 49, the application of

GAAP involves the exercise of varying degrees of judgment. The following areas require

more judgment relative to the others and relate to Global Financing. Also see “Critical

Accounting Estimates” on page 32.

Financing Receivables Reserves

Global Financing reviews its financing receivables portfolio at least quarterly in order to

assess collectibility. A description of the methods used by management to estimate the

amount of uncollectible receivables is included on page 54. Factors that could result in

actual receivable losses that are materially different from the estimated reserve include

sharp changes in the economy, or a large change in the health of a particular industry seg-

ment that represents a concentration in Global Financing’s receivables portfolio.

To the extent that actual collectibility differs from management’s estimates by 5 per-

cent, Global Financing net income would be higher or lower by an estimated $24 million

(using 2004 data), depending upon whether the actual collectibility was better or worse,

respectively, than the estimates.

Residual Value

Residual value represents the estimated fair value of equipment under lease as of the end

of the lease. Global Financing estimates the future fair value of residual values by using

historical models, the current market for used equipment and forward-looking product

information such as marketing plans and technological innovations. In addition, Global

Financing estimates the fair value by analyzing current market conditions for leasing and

sales of both new and used equipment. These estimates are periodically reviewed and any

other than temporary declines in estimated future residual values are recognized upon

identification. Anticipated increases in future residual value are not recognized until the

equipment is remarketed. Factors that could cause actual results to materially differ from

the estimates include severe changes in the used equipment market brought on by

unforeseen changes in technology innovations and any resulting changes in the useful

lives of used equipment.

To the extent that actual residual value recovery is lower than management’s estimates

by 5 percent, Global Financing’s net income would be lower by an estimated $16 million

(using 2004 data). If the actual residual value recovery is higher than management’s esti-

mates, the increase in net income will be realized at the end of lease when the equipment

is remarketed.

market risk

See pages 33 and 34 for discussion of the company’s overall market risk.

looking forward

Given Global Financing’s mission of supporting IBM’s hardware, software and services

businesses, originations for both customer and commercial finance businesses will be

dependent upon the overall demand for IT hardware, software and services, as well as the

customer participation rates.

Interest rates and the overall economy (including currency fluctuations) will have an

effect on both revenue and gross profit. The company’s interest rate risk management

policy, however, combined with the Global Financing funding strategy (see page 38),

should mitigate gross margin erosion due to changes in interest rates. The company’s

policy of matching asset and liability positions in foreign currencies will limit the impacts

of currency fluctuations.

The economy could impact the credit quality of the Global Financing receivables port-

folio and therefore the level of provision for bad debts. Global Financing will continue to

apply rigorous credit policies in both the origination of new business and the evaluation

of the existing portfolio.

As discussed above, Global Financing has historically been able to manage residual

value risk both through insight into the product cycles as well as through its remarket-

ing business.

Global Financing has policies in place to manage each of the key risks involved in

financing. These policies, combined with product and customer knowledge, should allow

for the prudent management of the business going forward, even during periods of

uncertainty with respect to the economy.

Forward-Looking and Cautionary Statements

Certain statements contained in this Annual Report may constitute forward-looking state-

ments within the meaning of the Private Securities Litigation Reform Act of 1995. These

statements involve a number of risks, uncertainties and other factors that could cause

actual results to be materially different, as discussed more fully elsewhere in this Annual

Report and in the company’s filings with the SEC, including the company’s 2004 Form 10-K

filed on February 24, 2005.