IBM 2004 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2004 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

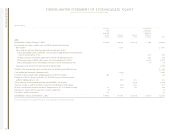

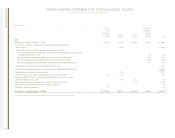

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

International Business Machines Corporation and Subsidiary Companies

54

ibm annual report 2004

The company generally reports cash flows arising from the company’s derivative

financial instruments consistent with the classification of cash flows from the underlying

hedged items that the derivatives are hedging. Accordingly, the majority of cash flows

associated with the company’s derivative programs are classified in Cash flows from operat-

ing activities in the Consolidated Statement of Cash Flows. For currency swaps designated

as hedges of foreign currency denominated debt (included in the company’s debt risk

management program as addressed in note l, “Derivatives and Hedging Transactions” on

pages 65 to 67), cash flows directly associated with the settlement of the principal element

of these swaps are reported in Payments to settle debt in the Cash flow from financing

activities section of the Consolidated Statement of Cash Flows.

financial instruments

In determining fair value of its financial instruments, the company uses a variety of methods

and assumptions that are based on market conditions and risks existing at each balance

sheet date. For the majority of financial instruments, including most derivatives, long-term

investments and long-term debt, standard market conventions and techniques such as

discounted cash flow analysis, option-pricing models, replacement cost and termination

cost are used to determine fair value. Dealer quotes are used for the remaining financial

instruments. All methods of assessing fair value result in a general approximation of value,

and such value may never actually be realized.

cash equivalents

All highly liquid investments with maturities of three months or less at the date of purchase

are carried at fair value and considered to be cash equivalents.

marketable securities

Marketable securities included in Current assets represent securities with a maturity of

less than one year. The company also has marketable securities, including non-equity

method alliance investments, with a maturity of more than one year. These non-current

investments are included in Investments and sundry assets. The company’s marketable

securities, including certain non-equity method alliance investments, are considered

available for sale and are reported at fair value with changes in unrealized gains and losses,

net of applicable taxes, recorded in Accumulated gains and (losses) not affecting retained

earnings within Stockholders’ equity. Realized gains and losses are calculated based on

the specific identification method. Other-than-temporary declines in market value from

original cost are charged to Other (income) and expense in the period in which the loss

occurs. In determining whether an other-than-temporary decline in the market value has

occurred, the company considers the duration that, and extent to which, market value is

below original cost. Realized gains and losses also are included in Other (income) and

expense in the Consolidated Statement of Earnings. All other investment securities not

described above or in “Principles of Consolidation” on page 49, primarily non-publicly

traded equity securities, are accounted for using the cost method.

inventories

Raw materials, work in process and finished goods are stated at the lower of average cost

or net realizable value.

allowance for uncollectible receivables

Trade

An allowance for uncollectible trade receivables is recorded based on a combination of

write-off history, aging analysis, and any specific, known troubled accounts.

Financing

Financing receivables include sales-type leases, direct financing leases, and loans. Below

are the methodologies the company uses to calculate both its specific and its unallocated

reserves, which are applied consistently to its different portfolios.

Specific. The company reviews all financing accounts receivable considered at risk on a

quarterly basis. The review primarily consists of an analysis based upon current information

available about the client, such as financial statements, news reports and published credit

ratings, as well as the current economic environment, collateral net of repossession cost

and prior history. For loans that are collateral dependent, impairment is measured using

the fair value of the collateral when foreclosure is probable. Using this information, the

company determines the expected cash flow for the receivable and calculates a recom-

mended estimate of the potential loss and the probability of loss. For those accounts in

which the loss is probable, the company records a specific reserve.

Unallocated. The company records an unallocated reserve that is calculated by applying a

reserve rate to its different portfolios, excluding accounts that have been specifically

reserved. This reserve rate is based upon credit rating, probability of default, term, asset

characteristics, and loss history.

Receivable losses are charged against the allowance when management believes the

uncollectibility of the receivable is confirmed. Subsequent recoveries, if any, are credited

to the allowance.

Certain receivables for which the company recorded specific reserves may also be

placed on nonaccrual status. Nonaccrual assets are those receivables (impaired loans or

nonperforming leases) with specific reserves and other accounts for which it is likely that

the company will be unable to collect all amounts due according to original terms of the

lease or loan agreement. Income recognition is discontinued on these receivables.

Receivables may be removed from nonaccrual status, if appropriate, based upon changes

in client circumstances.