ADT 2003 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2003 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

76

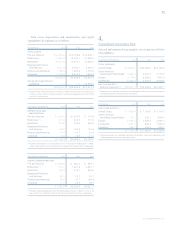

The following weighted-average assumptions were used for

fiscal 2003, fiscal 2002 and fiscal 2001:

2003 2002

2001

TYCO TYCO TYCO TYCOM

Expected stock price

volatility 64% 52% 39% 80%

Risk-free interest rate 2.48% 4.03% 5.18% 4.71%

Expected annual

dividend per share $0.05 $0.05 $0.05 —

Expected life of

options 4.3 years 5.0 years 4.4 years 4.0 years

The effects of applying SFAS No. 123 in this pro forma disclosure

are not indicative of what the effects may be in future years.

SFAS No. 123 does not apply to awards prior to 1995. Additional

awards in future years are anticipated.

During fiscal 2003, the Company adopted FASB Interpreta-

tion No. (“FIN”) 45, “Guarantor’s Accounting and Disclosure

Requirements for Guarantees.” FIN 45 requires increased dis-

closure of guarantees, including those for which likelihood of

payment is remote, and product warranty information (see Note

20). FIN 45 also requires that guarantors recognize a liability

for certain types of guarantees equal to the fair value of the

guarantee upon its issuance. The adoption of FIN 45 did not

have a material impact on our results of operations or finan-

cial position.

In January 2003, the FASB issued FIN 46, “Consolidation of

Variable Interest Entities.” This interpretation clarifies the

application of Accounting Research Bulletin No. 51, “Consoli-

dated Financial Statements,” relating to consolidation of certain

entities. FIN 46 requires identification of the Company’s partici-

pation in variable interest entities (“VIE’s”), which are defined

as entities with a level of invested equity that is not sufficient to

fund future activities to permit them to operate on a stand-

alone basis, or whose equity holders lack certain characteristics

of a controlling financial interest. For entities identified as

VIE’s, FIN 46 sets forth a model to evaluate potential consoli-

dation based on an assessment of which party to VIE’s, if any,

bears a majority of the risk to its expected losses, or stands to

gain from a majority of its expected returns. FIN 46 also sets

forth certain disclosures regarding interests in VIE’s that are

deemed significant, even if consolidation is not required. The

Company adopted FIN 46’s accounting provisions as of July 1,

2003. See Notes 12 and 30 for further discussion of the impact

of FIN 46.

In November 2002, the EITF reached a consensus on EITF

Issue No. 00-21, “Revenue Arrangements with Multiple Deliver-

ables.” EITF No. 00-21 provides guidance on how to determine

when an arrangement that involves multiple revenue-generating

activities or deliverables should be divided into separate units

of accounting for revenue recognition purposes. It further states,

that if this division is required, the arrangement consideration

should be allocated among the separate units of accounting.

The guidance in the consensus is effective for revenue arrange-

ments entered into in fiscal periods that began after June 15,

2003. The adoption of this new standard did not have a material

impact on our results of operations or financial position.

In April 2003, the FASB issued SFAS No. 149, “Amendment

of Statement 133 on Derivative Instruments and Hedging

Activities,” which amends and clarifies financial accounting and

reporting for derivative instruments, including certain derivative

instruments embedded in other contracts and for hedging

activities under SFAS No. 133, “Accounting for Derivative

Instruments and Hedging Activities.” SFAS No. 149, which is to

be applied prospectively, is effective for contracts entered into

or modified after June 30, 2003, and for hedging relationships

designated after June 30, 2003. The adoption of this new standard

did not have a material impact on our results of operations or

financial position.

In May 2003, the FASB issued SFAS No. 150, “Accounting for

Certain Financial Instruments with Characteristics of Both

Liabilities and Equity,” which establishes standards for how an

issuer classifies and measures certain financial instruments

with characteristics of both liabilities and equity. It requires

that an issuer classify a financial instrument that is within its

scope as a liability (or an asset in some circumstances) and is

effective for instruments entered into or modified after May 31,

2003 and otherwise is effective at the beginning of the first

interim period beginning after June 15, 2003. The adoption of

this new standard did not have a material impact on our results

of operations or financial position.

Reclassifications Certain prior year amounts have been reclas-

sified to conform with current year presentation.

TYCO INTERNATIONAL LTD.

Notes to Consolidated Financial Statements