ADT 2003 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2003 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

111

TYCO INTERNATIONAL LTD.

obligations for Messrs. Kozlowski and Swartz as of September 30,

2002 were $50.6 million and $25.9 million, respectively. Retire-

ment benefits are available at earlier ages and alternative forms

of benefits can be elected. Any such variations would be

actuarially equivalent to the fixed lifetime benefit starting at

age 65. Amounts owed to Messrs. Kozlowski and Swartz under

the ERA are in dispute by the Company. For further information,

see Note 18.

Defined Contribution Retirement Plans The Company maintains

several defined contribution retirement plans, which include

401(k) matching programs, as well as qualified and nonqualified

profit sharing and share bonus retirement plans. Pension

expense for the defined contribution plans is computed as a

percentage of participants’ compensation and was $184.0 mil-

lion, $179.9 million and $152.8 million for fiscal 2003, fiscal

2002 and fiscal 2001, respectively. The Company also maintains

an unfunded Supplemental Executive Retirement Plan (“SERP”).

This plan is nonqualified and restores the employer match that

certain employees lose due to IRS limits on eligible compensa-

tion under the defined contribution plans. Expense related to

the SERP was $4.0 million, $16.1 million and $9.3 million in

fiscal 2003, fiscal 2002 and fiscal 2001, respectively.

Deferred Compensation Plans The Company has nonqualified

deferred compensation plans, which permit eligible employees

to defer a portion of their compensation. A record keeping

account is set up for each participant and the participant chooses

from a variety of measurement funds for the deemed invest-

ment of their accounts. The measurement funds correspond to

a number of funds in the Company’s 401(k) plans and the

account balance fluctuates with the investment returns on those

funds. Deferred compensation expense was $17.4 million,

$15.9 million and $10.3 million for fiscal 2003, fiscal 2002 and

fiscal 2001, respectively. Total deferred compensation liabilities

were $189.0 million, $182.3 million and $292.3 million for fiscal

2003, fiscal 2002 and fiscal 2001. The Company has established

a rabbi trust that is currently funded through corporate-owned

life insurance policies. The rabbi trust assets, which are consoli-

dated, are available to pay plan benefits and are subject to the

claims of the Company’s creditors in the event of the Company’s

insolvency. The cash surrender value of these policies, net of

outstanding loans, included in other noncurrent assets on the

Consolidated Balance Sheet were $231.7 million, $316.0 mil-

lion and $328.6 million in fiscal 2003, fiscal 2002 and fiscal

2001, respectively. The employees are general creditors of the

Company with respect to these benefits.

Postretirement Benefit Plans The Company generally does not

provide postretirement benefits other than pensions for its

employees. However, certain acquired operations provide these

benefits to employees who were eligible at the date of acquisition,

and a small number of U.S. and Canadian operations provide

on-going eligibility for such benefits. The following tables

exclude amounts related to the discontinued operations of CIT

for all periods presented.

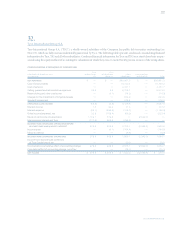

Net periodic postretirement benefit cost reflects the following

components ($ in millions):

2003 2002 2001

Service cost $««2.0 $««1.8 $««3.4

Interest cost 23.5 22.5 22.7

Expected return on assets (0.3) (0.4) (0.3)

Recognition of prior

service credit (3.3) (3.5) (2.5)

Recognition of net actuarial

loss (gain) 7.1 — (1.7)

Curtailment/settlement

(gain) loss (2.3) —0.4

Net periodic postretirement

benefit cost $26.7 $20.4 $22.0

The components of the accrued postretirement benefit

obligation, substantially all of which are unfunded, are as follows

($ in millions):

SEPTEMBER 30, 2003 2002

CHANGE IN BENEFIT OBLIGATION

Benefit obligation at beginning of year $«355.4 $«332.6

Service cost 2.0 1.8

Interest cost 23.5 22.5

Amendments (14.3) 0.7

Actuarial loss 71.0 32.5

Acquisition —(1.1)

Plan curtailments (4.6) —

Expected net benefits paid (36.2) (33.6)

Currency translation adjustment 1.1 —

Benefit obligation at end of year $«397.9 $«355.4

CHANGE IN PLAN ASSETS

Fair value of assets at beginning of year $«««««4.7 $«««««5.2

Employer contributions 35.8 33.5

Payment of benefits from plan assets (36.2) (33.6)

Actual return on plan assets 0.4 (0.4)

Fair value of plan assets at end of year $«««««4.7 $«««««4.7

Funded status $(393.2) $(350.7)

Unrecognized net loss 110.6 47.5

Unrecognized prior service cost (36.1) (24.0)

Accrued postretirement benefit cost $(318.7) $(327.2)