ADT 2003 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2003 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

54

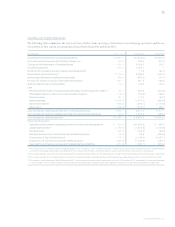

Off-Balance Sheet Arrangements

SALES OF ACCOUNTS RECEIVABLE

Tyco has several programs under which it sells participating

interests in accounts receivable to investors who, in turn, pur-

chase and receive ownership and security interests in those

receivables. As collections reduce accounts receivable included

in the pool, the Company sells new receivables. The Company

has the risk of credit loss on the receivables and, accordingly,

the full amount of the allowance for doubtful accounts has

been retained on the Consolidated Balance Sheets. At

September 30, 2003, the availability under these programs is

$1,025 million. At September 30, 2003 and 2002, $803 million

and $933 million, respectively, was utilized under the programs.

The proceeds from the sales were used to repay short-term and

long-term borrowings and for working capital and other cor-

porate purposes and are reported as operating cash flows in the

Consolidated Statements of Cash Flows. The sale proceeds are

less than the face amount of accounts receivable sold by an

amount that approximates the cost that would be incurred if

commercial paper were issued backed by these accounts receiv-

able. The discount from the face amount is accounted for as a

loss on the sale of receivables and has been included in selling,

general and administrative expenses in the Consolidated

Statements of Operations. Such discount aggregated $29.0 mil-

lion, $17.0 million, and $25.3 million, or 3.5%, 2.7%, and 5.3%

of the weighted-average balance of the receivables outstanding,

during fiscal 2003, 2002 and 2001, respectively. The Company

retains collection and administrative responsibilities for the

participating interests in the defined pool. Also, some of our

international businesses sell accounts receivable as a short-term

financing mechanism. These transactions qualify as true sales.

The aggregate amount outstanding under these arrangements

was $202 million and $157 million at September 30, 2003 and

2002, respectively.

As a result of the rating agencies’ downgrade of Tyco’s debt

in June 2002, investors of one of our accounts receivable pro-

grams have the option to discontinue reinvestment in new

receivables and terminate the program. However, the investors

have not exercised this option. The amount outstanding under

this program was $103.2 million and $132.4 million at

September 30, 2003 and 2002, respectively.

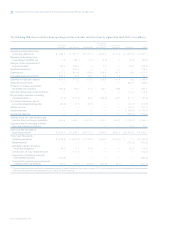

VARIABLE INTEREST ENTITIES (VIE’s)

During fiscal 2003, the Company adopted FIN 46, which

requires identification of the Company’s participation in VIE’s,

which are entities with a level of invested equity that is not

sufficient to fund future activities to permit them to operate

on a stand-alone basis, or whose equity holders lack certain

characteristics of a controlling financial interest. For entities

identified as VIE’s, FIN 46 sets forth a model to evaluate poten-

tial consolidation based on an assessment of which party to

VIE’s, if any, bears a majority of the risk to its expected losses,

or stands to gain from a majority of its expected returns.

The Company has programs under which it sells machinery

and equipment to investors who, in turn, purchase and receive

ownership and security interests in those assets. As such, the

Company may have certain investments in those affiliated com-

panies whereby it provides varying degrees of financial support

and where the investors are entitled to a share in the results of

those entities but do not consolidate these entities. While these

entities may be substantive operating companies, they have

been evaluated for potential consolidation under FIN 46.

As discussed in “Results of Operations

—

Cumulative Effect

of Accounting Changes,” the Company has three synthetic lease

programs utilized, to some extent, by all of the Company’s seg-

ments to finance capital expenditures for manufacturing

machinery and equipment and for ships used by Tyco

Submarine Telecommunications. During fiscal 2003, the

Company restructured one of the synthetic leases to meet the

requirements of FIN 46 for operating lease accounting and

reclassified the remaining two leases as capital leases. In addi-

tion, the Company evaluated other investments and concluded

that four joint ventures that were previously accounted for

under the equity method of accounting within Tyco

Infrastructure Services, in which we own a minority interest,

meet the consolidation criteria set forth in FIN 46. Accordingly,

these ventures have been consolidated onto the Company’s

balance sheet. The following table presents balance sheet infor-

mation for the VIE’s that were included within the Company’s

TYCO INTERNATIONAL LTD.

Management’s Discussion and Analysis of Financial Condition and Results of Operations