3M 2010 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2010 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

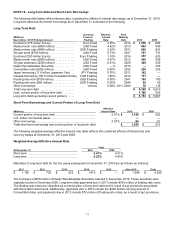

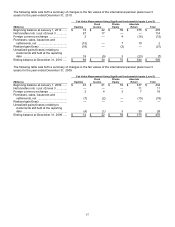

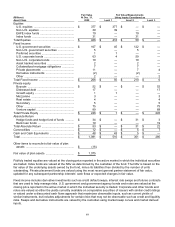

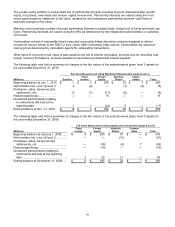

|

|

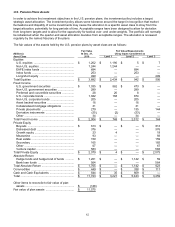

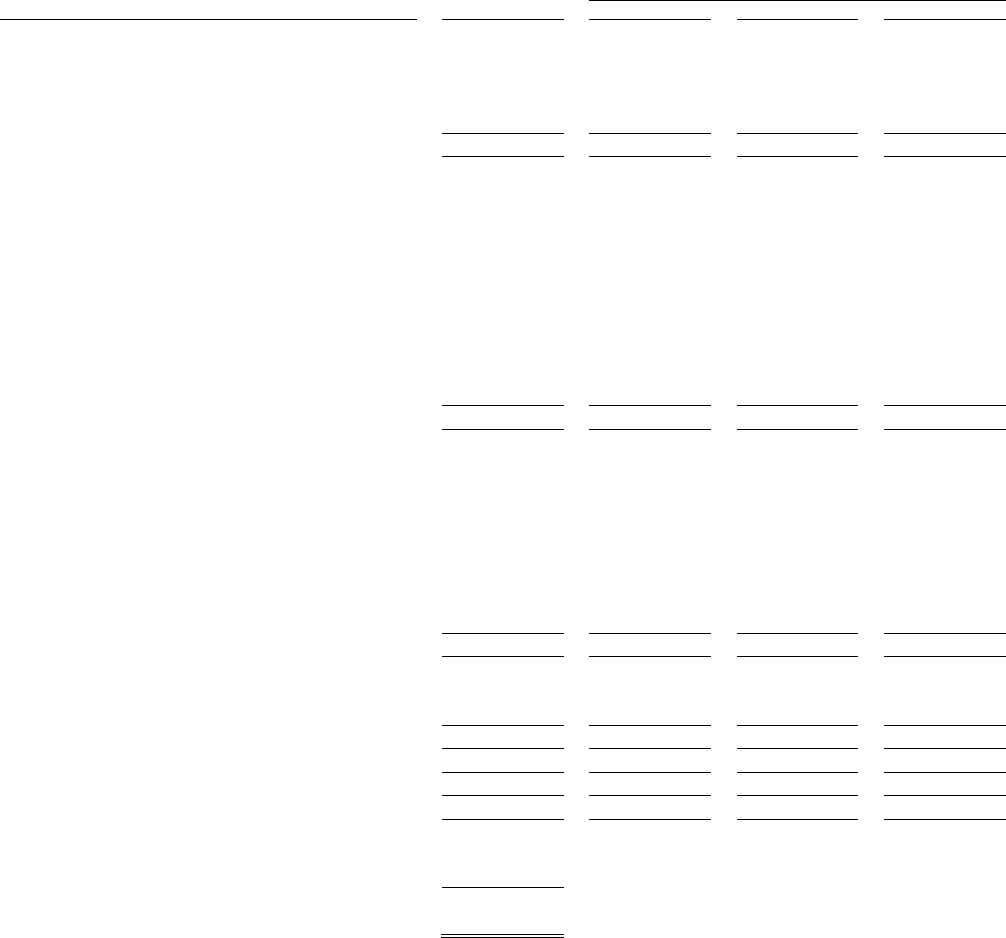

83

(Millions)

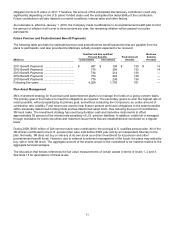

Fair Value

At Dec. 31,

Fair Value Measurements

Using Inputs Considered as

Asset Class

2009

Level 1

Level 2

Level 3

Equities

U.S. equities ...................................................

$

1,215

$

1,206

$

6

$

3

Non-U.S. equities ............................................

1,128

1,128

—

—

EAFE index funds ...........................................

633

—

633

—

Other ...............................................................

7

6

—

1

Total Equities ......................................................

$

2,983

$

2,340

$

639

$

4

Fixed Income

U.S. government securities ............................

$

891

$

610

$

281

$

—

Non-U.S. government securities .....................

165

—

165

—

Preferred and convertible securities ...............

29

20

9

—

U.S. corporate bonds ......................................

1,222

147

1,059

16

Non-U.S. corporate bonds ..............................

175

—

175

—

Asset backed securities ..................................

20

—

20

—

Collateralized mortgage obligations ...............

56

—

56

—

Private placements .........................................

253

—

120

133

Derivative instruments ....................................

(50

)

6

(56

)

—

Other ...............................................................

36

—

—

36

Total Fixed Income .............................................

$

2,797

$

783

$

1,829

$

185

Private Equity

Buyouts ...........................................................

$

569

$

—

$

—

$

569

Distressed debt ...............................................

359

—

—

359

Growth equity ..................................................

32

32

—

—

Mezzanine ......................................................

102

—

—

102

Real estate ......................................................

134

—

—

134

Secondary .......................................................

147

—

—

147

Other ...............................................................

137

4

—

133

Venture capital ................................................

517

—

—

517

Total Private Equity ............................................

$

1,997

$

36

$

—

$

1,961

Absolute Return

Hedge funds and hedge fund of funds ...........

$

1,141

$

—

$

1,038

$

103

Bank loan funds ..............................................

625

—

—

625

Total Absolute Return .........................................

$

1,766

$

—

$

1,038

$

728

Commodities ......................................................

$

396

$

—

$

159

$

237

Cash and Cash Equivalents ...............................

$

696

$

552

$

144

$

—

Total ....................................................................

$

10,635

$

3,711

$

3,809

$

3,115

Other items to reconcile to fair value of plan

assets .............................................................

$

(142

)

Fair value of plan assets ....................................

$

10,493

Publicly traded equities are valued at the closing price reported in the active market in which the individual securities

are traded. Index funds are valued at the net asset value (NAV) as determined by the custodian of the fund. The NAV

is based on the fair value of the underlying assets owned by the fund, minus its liabilities then divided by the number

of units outstanding. Private placement funds are valued using the most recent general partner statement of fair

value, updated for any subsequent partnership interests’ cash flows or expected changes in fair value.

Fixed income includes derivative instruments such as credit default swaps, interest rate swaps and futures contracts

that are used to help manage risks. U.S. government and government agency bonds and notes are valued at the

closing price reported in the active market in which the individual security is traded. Corporate and other bonds and

notes are valued at either the yields currently available on comparable securities of issuers with similar credit ratings

or valued under a discounted cash flows approach that maximizes observable inputs, such as current yields of

similar instruments, but includes adjustments for certain risks that may not be observable such as credit and liquidity

risks. Swaps and derivative instruments are valued by the custodian using closing market swap curves and market

derived inputs.