3M 2010 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2010 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

32

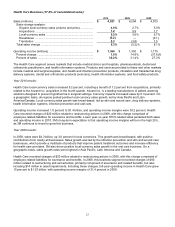

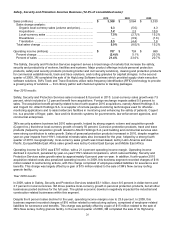

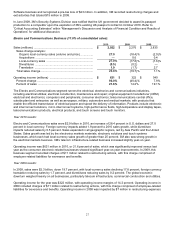

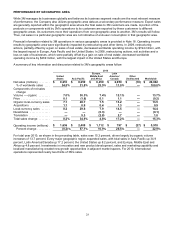

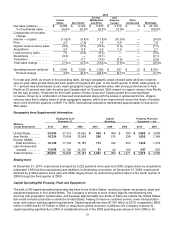

As of September 30, 2010, 3M had 38 primary reporting units, with eight reporting units accounting for approximately

71 percent of the goodwill. These eight reporting units were comprised of the following divisions: 3M Purification Inc.,

Occupational Health and Environmental Safety, Optical Systems, 3M ESPE, Communication Markets, Industrial

Adhesives and Tapes, Security Systems, and Health Information Systems.

The fair values for the majority of reporting units were in excess of carrying value by more than 30 percent. The fair

values for Optical Systems and 3M Purification Inc., based on fourth quarter 2010 testing, were in excess of carrying

value by approximately 23 percent and 26 percent, respectively, with no impairment indicated. As part of its annual

impairment testing in the fourth quarter, 3M used a weighted-average discounted cash flow analysis for Optical

Systems and 3M Purification Inc., using projected cash flows that were weighted based on different sales growth and

terminal value assumptions, among other factors. The weighting was based on management’s estimates of the

likelihood of each scenario occurring. In the fourth quarter of 2010, 3M made several larger acquisitions. These

acquisitions (with their reporting unit indicated) included Arizant Inc. (Infection Prevention), Cogent Inc. (Security

Systems) and Attenti Holdings S.A. (Track and Trace), with goodwill of approximately $512 million, $295 million and

$122 million, respectively. Due to the significance of the Cogent Inc. acquisition with respect to its reporting unit, 3M

will be monitoring the Security Systems Division in 2011 for any triggering events or other indicators of impairment.

In 2010, for those reporting units whose fair value was in excess of carrying value by more than 30 percent, 3M

primarily used an industry price-earnings ratio approach, but also used a discounted cash flows approach for certain

reporting units. Based on the fair values determined using discounted cash flows for certain reporting units and the

industry price-earnings ratio approach for the remaining reporting units, at September 30, 2010, 3M’s implied control

premium was approximately 23 percent. The control premium is defined as the sum of the individual reporting units

estimated market values compared to 3M’s total Company market value, with the sum of the individual values

typically being larger than the value for the total Company. At September 30, 2010, 3M’s market value was

approximately $62 billion, but if each reporting unit was valued individually, 3M’s market value would be

approximately $76 billion using a 23 percent control premium. 3M is an integrated materials enterprise, thus; many of

3M’s businesses could not easily be sold on a stand-alone basis. Based on its annual test in the fourth quarter of

2010, no goodwill impairment was indicated for any of the reporting units. In addition, 3M’s market value at both

September 30, 2010 and December 31, 2010 of approximately $62 billion and $61 billion, respectively, was

significantly in excess of its equity of approximately $16 billion.

Factors which could result in future impairment charges, among others, include changes in worldwide economic

conditions, changes in competitive conditions and customer preferences, and fluctuations in foreign currency

exchange rates. These risk factors are discussed in Item 1A, “Risk Factors”, of this document. As of December 31,

2010, 3M had approximately $1 billion of goodwill related to 3M Purification Inc. and $750 million related to Optical

Systems. In addition, as a result of the Cogent Inc. acquisition in the fourth quarter of 2010, Security Systems

Division goodwill increased to approximately $500 million. If future non-cash impairment charges are taken, 3M

would expect that only a portion of the long-lived assets or goodwill would be impaired. 3M will continue to monitor its

reporting units in 2011 for any triggering events or other indicators of impairment.

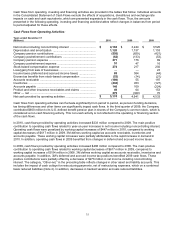

Income Taxes:

The extent of 3M’s operations involves dealing with uncertainties and judgments in the application of complex tax

regulations in a multitude of jurisdictions. The final taxes paid are dependent upon many factors, including

negotiations with taxing authorities in various jurisdictions and resolution of disputes arising from federal, state, and

international tax audits. The Company recognizes potential liabilities and records tax liabilities for anticipated tax

audit issues in the United States and other tax jurisdictions based on its estimate of whether, and the extent to which,

additional taxes will be due. The Company follows guidance provided by ASC 740, Income Taxes, regarding

uncertainty in income taxes, to record these liabilities (refer to Note 8 for additional information). The Company

adjusts these reserves in light of changing facts and circumstances; however, due to the complexity of some of these

uncertainties, the ultimate resolution may result in a payment that is materially different from the Company’s current

estimate of the tax liabilities. If the Company’s estimate of tax liabilities proves to be less than the ultimate

assessment, an additional charge to expense would result. If payment of these amounts ultimately proves to be less

than the recorded amounts, the reversal of the liabilities would result in tax benefits being recognized in the period

when the Company determines the liabilities are no longer necessary.