Xcel Energy 2013 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2013 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

62

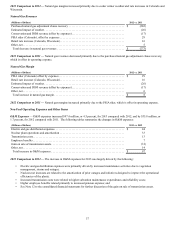

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Preparation of the consolidated financial statements and related disclosures in compliance with GAAP requires the application of

accounting rules and guidance, as well as the use of estimates. The application of these policies involves judgments regarding future

events, including the likelihood of success of particular projects, legal and regulatory challenges and anticipated recovery of costs.

These judgments could materially impact the consolidated financial statements and disclosures, based on varying assumptions. In

addition, the financial and operating environment also may have a significant effect on the operation of the business and on the results

reported even if the nature of the accounting policies applied have not changed. The following is a list of accounting policies and

estimates that are most significant to the portrayal of Xcel Energy’s financial condition and results, and that require management’s

most difficult, subjective or complex judgments. Each of these has a higher likelihood of resulting in materially different reported

amounts under different conditions or using different assumptions. Each critical accounting policy has been reviewed and discussed

with the Audit Committee of Xcel Energy Inc.’s Board of Directors on a quarterly basis.

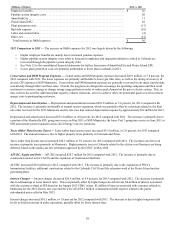

Regulatory Accounting

Xcel Energy Inc. is a holding company with rate-regulated subsidiaries that are subject to the accounting for Regulated Operations,

which provides that rate-regulated entities account for and report assets and liabilities consistent with the recovery of those incurred

costs in rates, if the rates established are designed to recover the costs of providing the regulated service and if the competitive

environment makes it probable that such rates will be charged and collected. Xcel Energy’s rates are derived through the ratemaking

process, which results in the recording of regulatory assets and liabilities based on the probability of future cash flows. Regulatory

assets generally represent incurred or accrued costs that have been deferred because they are probable of future recovery from

customers. Regulatory liabilities generally represent amounts that are expected to be refunded to customers in future rates or amounts

collected in current rates for future costs. In other businesses or industries, regulatory assets and regulatory liabilities would generally

be charged to net income or OCI.

Each reporting period Xcel Energy assesses the probability of future recoveries and obligations associated with regulatory assets and

liabilities. Factors such as the current regulatory environment, recently issued rate orders and historical precedents are considered.

Decisions made by regulatory agencies can directly impact the amount and timing of cost recovery as well as the rate of return on

invested capital and may materially impact Xcel Energy’s results of operations, financial condition, or cash flows.

As of Dec. 31, 2013 and 2012, Xcel Energy has recorded regulatory assets of $2.9 billion and $3.1 billion and regulatory liabilities of

$1.3 billion and $1.2 billion, respectively. Each subsidiary is subject to regulation that varies from jurisdiction to jurisdiction. If

future recovery of costs, in any such jurisdiction, ceases to be probable, Xcel Energy would be required to charge these assets to

current net income or OCI. There are no current or expected proposals or changes in the regulatory environment that impact the

probability of future recovery of these assets. However, if the SEC should mandate the use of IFRS and the lack of an accounting

standard for rate-regulated entities under IFRS could require us to charge certain regulatory assets and regulatory liabilities to net

income or OCI. See Note 15 to the consolidated financial statements for further discussion of regulatory assets and liabilities and

Note 12 to the consolidated financial statements for further discussion of rate matters.

Income Tax Accruals

Judgment, uncertainty, and estimates are a significant aspect of the income tax accrual process that accounts for the effects of current

and deferred income taxes. Uncertainty associated with the application of tax statutes and regulations and the outcomes of tax audits

and appeals require that judgment and estimates be made in the accrual process and in the calculation of the ETR. Changes in tax

laws and rates may affect recorded deferred tax assets and liabilities and our ETR in the future.

ETRs are also highly impacted by assumptions. ETR calculations are revised every quarter based on best available year end tax

assumptions (income levels, deductions, credits, etc.); adjusted in the following year after returns are filed, with the tax accrual

estimates being trued-up to the actual amounts claimed on the tax returns; and further adjusted after examinations by taxing authorities

have been completed.

In accordance with the interim period reporting guidance, income tax expense for the first three quarters in a year is based on the

forecasted ETR.

Accounting for income taxes also requires that only tax benefits that meet the more likely than not recognition threshold can be

recognized or continue to be recognized. The change in the unrecognized tax benefits needs to be reasonably estimated based on

evaluation of the nature of uncertainty, the nature of event that could cause the change and an estimated range of reasonably possible

changes. At any period end, and as new developments occur, management will use prudent business judgment to derecognize

appropriate amounts of tax benefits. Unrecognized tax benefits can be recognized as issues are favorably resolved and loss exposures

decline.