Xcel Energy 2013 Annual Report Download - page 162

Download and view the complete annual report

Please find page 162 of the 2013 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

144

The total obligation for decommissioning currently is expected to be funded 100 percent by the external decommissioning trust fund,

as approved by the MPUC, when decommissioning commences. The external funds are held in trust and in escrow. The portion in

escrow is subject to refund if approved by the various commissions. In November 2012, the MPUC approved NSP-Minnesota’s most

recent nuclear decommissioning study which used 2011 cost data. The MPUC approved the use of a 60-year decommissioning

scenario. This resulted in an approved annual accrual of $14.2 million for Minnesota retail customers, to be held in our external

escrow fund.

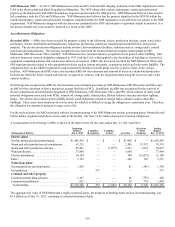

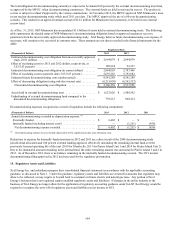

As of Dec. 31, 2013, NSP-Minnesota has accumulated $1.6 billion of assets held in external decommissioning trusts. The following

table summarizes the funded status of NSP-Minnesota’s decommissioning obligation based on approved regulatory recovery

parameters from the most recently approved decommissioning study. Xcel Energy believes future decommissioning cost expense, if

necessary, will continue to be recovered in customer rates. These amounts are not those recorded in the financial statements for the

ARO.

Regulatory Basis

(Thousands of Dollars) 2013 2012

Estimated decommissioning cost obligation from most recently approved

study (2011 dollars) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2,694,079 $ 2,694,079

Effect of escalating costs (to 2013 and 2012 dollars, respectively, at

3.63/2.63 percent) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189,924 93,327

Estimated decommissioning cost obligation (in current dollars) . . . . . . . . 2,884,003 2,787,406

Effect of escalating costs to payment date (3.63/2.63 percent). . . . . . . . . . 5,697,285 5,793,882

Estimated future decommissioning costs (undiscounted) . . . . . . . . . . . . . . 8,581,288 8,581,288

Effect of discounting obligation (using risk-free interest rate) . . . . . . . . . . (6,215,050)(6,243,332)

Discounted decommissioning cost obligation . . . . . . . . . . . . . . . . . . . . $ 2,366,238 $ 2,337,956

Assets held in external decommissioning trust . . . . . . . . . . . . . . . . . . . . . . $ 1,627,026 $ 1,489,542

Underfunding of external decommissioning fund compared to the

discounted decommissioning obligation . . . . . . . . . . . . . . . . . . . . . . . . . 739,212 848,414

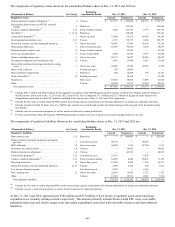

Decommissioning expenses recognized as a result of regulation include the following components:

(Thousands of Dollars) 2013 2012 2011

Annual decommissioning recorded as depreciation expense: (a)

Externally funded . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 6,402 $ — $ —

Internally funded (including interest costs) . . . . . . . . . . . . . . . . . . . . . . . — (1,251)(456)

Net decommissioning expense recorded . . . . . . . . . . . . . . . . . . . . . . . . $ 6,402 $ (1,251) $ (456)

(a) Decommissioning expense does not include depreciation of the capitalized nuclear asset retirement costs.

Reductions to expense for internally-funded portions in 2012 and 2011 are a direct result of the 2008 decommissioning study

jurisdictional allocation and 100 percent external funding approval, effectively unwinding the remaining internal fund over the

previously licensed operating life of the unit (2010 for Monticello, 2013 for Prairie Island Unit 1 and 2014 for Prairie Island Unit 2).

Due to the immaterial amount remaining in the internal fund, the entire remaining amount was unwound for Prairie Island 1 and 2 in

2012. As of December 2013, there is no balance remaining in the internally funded decommissioning account. The 2011 nuclear

decommissioning filing approved in 2012 has been used for the regulatory presentation.

15. Regulatory Assets and Liabilities

Xcel Energy Inc. and subsidiaries prepare their consolidated financial statements in accordance with the applicable accounting

guidance, as discussed in Note 1. Under this guidance, regulatory assets and liabilities are created for amounts that regulators may

allow to be collected, or may require to be paid back to customers in future electric and natural gas rates. Any portion of Xcel

Energy’s business that is not regulated cannot establish regulatory assets and liabilities. If changes in the utility industry or the

business of Xcel Energy no longer allow for the application of regulatory accounting guidance under GAAP, Xcel Energy would be

required to recognize the write-off of regulatory assets and liabilities in net income or OCI.