Tesco 2011 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2011 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

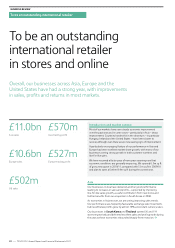

Europe

Our operations in Europe have delivered record results and strong

growth in sales, profits and margins. Recovering economies generally

helped but key to this performance was the striking improvement

in the competitiveness of our local businesses, which won market

share rapidly.

We have invested for customers through lower prices, sharper promotions

and Clubcard, funded by strong productivity and substantial early

benefits of our pan-European sourcing. The resulting strong sales

growth has driven an improvement in profitability and margins.

Sales growth varied across the region but all markets saw sharply

improved like-for-like sales growth compared with 2009/10, with a

good contribution also coming from new space.

In Ireland, like-for-like growth in the year was significantly stronger,

and although it was broadly stable during the second half, the two-year

trend has continued to improve. Despite a decline in consumer confidence

resulting from political and economic uncertainty and the continued

fall in disposable income, our business has continued its strong relative

performance with impressive market share gains.

Our business in Poland had another good year, with good growth in

sales and profits despite a period of subdued consumer sentiment

following the Smolensk tragedy.

In Hungary economic conditions and consumer confidence remain

challenging but despite this our business made solid progress.

Growth in the Czech Republic has been supported by the successful

launch of Clubcard – with over 10% of the population already enrolled.

A particularly strong performance in Slovakia with double-digit like-for-

like sales growth – has led to a further increase in our market share over

the last year, further consolidating our market leadership.

As the economy in Turkey has continued to recover, we’ve resumed

a faster rate of expansion – opening 21 new stores, including ten

hypermarkets – helping to support strong sales growth.

With the improving economic outlook we are stepping up the rate

of new store opening. Some 2.6m sq ft of new space was opened in the

year, with a programme to add a further 2.9m sq ft of new space across

the region in 2011/12.

Europe results 2010/11

£m

Actual rates

% growth

Constant rates

% growth

Europe sales 10,558 5.6 7.4

Europe revenue*9,192 5.4 7.1

Europe trading profit 527 11.2 13.7

Trading margin

(trading profit/revenue) 5.73% 30bp 42bp

United States

Customer feedback at Fresh & Easy remains excellent and strong

growth in customer numbers is driving steady sales improvement

in each store.

Although there is clearly some way to go, with these key elements

moving in the right direction, we plan to accelerate the rate of

new store openings to around 50 in the current year. With the

improvements in our distribution centre and manufacturing campus

productivity, we now expect to break-even with around 300 stores

rather than the 400 we originally anticipated.

Our losses increased in the year as a consequence of the initial costs

of integrating our two dedicated fresh food suppliers, 2 Sisters and

Wild Rocket Foods, and exchange rate movements. These businesses

have now been fully integrated with our existing kitchen operations,

with substantially improved financial performance, product quality

and service levels.

We expect losses to reduce sharply in the current year as strong growth

in like-for-like sales continues and improved store operating ratios

start to deliver shop-door profitability. We have a strong plan for the

business to break-even towards the end of the 2012/13 financial year.

US results 2010/11

£m

Actual rates

% growth

Constant rates

% growth

US sales 502 41.8 38.1

US revenue*495 41.8 38.1

US trading profit/(loss) (186) (12.7) (9.7)

EXTRAS IN EUROPE

We’ve remodelled and converted

eight Extra stores across Central

and Eastern Europe with an

average uplift of 16%. See

page 29 for more detail.

5.6%

Europe sales growth

* Revenue excludes VAT and the impact of IFRIC 13.

* Revenue excludes VAT and the impact of IFRIC 13.

TESCO PLC Annual Report and Financial Statements 2011

—

25

Overview Business review Governance Financial statements