Tesco 2011 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2011 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

NOTE 23 FINANCIAL RISK FACTORS CONTINUED

Insurance risk

Tesco Bank is exposed to insurance risks directly through its historic distribution arrangement with RBS Insurance and indirectly through its ownership

of 49.9% of Tesco Underwriting Limited (TU), an authorised insurance company.

Since October 2010 the majority of new business policies for Home and Motor Insurance product sold by Tesco Bank have been underwritten by

TU. Customers renewing their Tesco Motor or Home Insurance policy insurance have been underwritten by TU since November 2010. The key

insurance risks within TU relate to Underwriting Risk and specifically the potential for a major weather event to generate significant claims on Home

insurance or on Motor insurance the cost of settling bodily injury claims. Exposure to this risk is actively managed within TU with close monitoring of

performance metrics and the use of reinsurance to limit TU’s exposure above predetermined limits.

The legacy arrangement with RBS Insurance is now in run off and the primary risk that Tesco Bank remains exposed to is Reserving Risk – the risk that

reserves set by RBS Insurance will be insufficient to cover the ultimate cost of insurance claims arising from this activity. This is particularly relevant to

Motor Insurance claims where the ultimate cost of large bodily injury claims is uncertain and the time taken to settle such claims can vary significantly

depending on the severity of the injury. This risk is, in part, mitigated by the use of reinsurance to limit Tesco Bank’s exposure to the cost of individual

claims above certain predetermined limits. However, the nature of this is exposure results in the process of estimating the ultimate cost of these claims

carrying a degree of uncertainty.

Since October 2010 Pet, Travel and Breakdown insurance have all been distributed by Tesco Bank on a ‘white label’ basis. Tesco Bank does not carry

the insurance risk associated with these products.

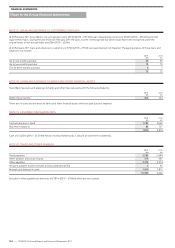

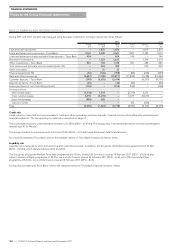

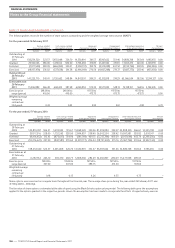

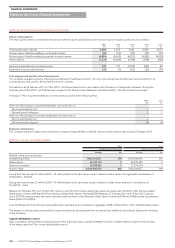

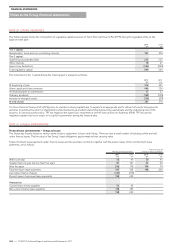

NOTE 24 CUSTOMER DEPOSITS

2011

£m

2010

£m

Customer deposits 5,074 4,357

Customer deposits are recorded at amortised cost. Included within customer deposits is £177m (2010 – £nil) that is non-current.

NOTE 25 DEPOSITS BY BANKS

The Group has deposits by banks with the following maturity:

2011

£m

2010

£m

Within three months 26 30

Three to six months 10 –

36 30

Deposits by banks are recorded at amortised cost.

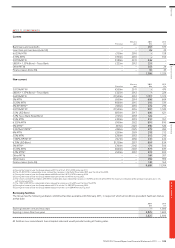

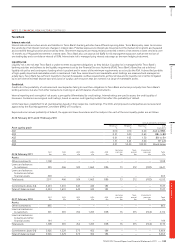

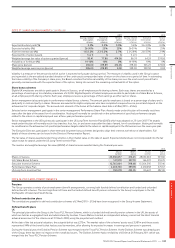

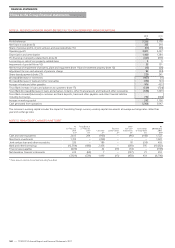

NOTE 26 PROVISIONS

Property

provisions

£m

Other

provision

£m

Total

£m

At 28 February 2009 111 99 210

Foreign currency translation 12 – 12

Amount provided in the year – 1 1

Amount utilised in the year (12) – (12)

At 27 February 2010 111 100 211

Foreign currency translation (3) – (3)

Amount released in the year (18) (50) (68)

Amount provided in the year 48 – 48

Amount utilised in the year – (11) (11)

At 26 February 2011 138 39 177

Property provisions comprise obligation for future rents payable net of rents receivable on onerous and vacant property leases, terminal dilapidations and

future rents above market value on unprofitable stores. The majority of these provisions are expected to be utilised over the period to 2020.

The other provision balance relates to a provision for customer redress in respect of potential customer complaints arising from historic sales of Personal

Protection Insurance (PPI). The provision is likely to be utilised over several years, although the timing of utilisation is uncertain.

The provision as at 27 February 2010 was established based on a forecast of the level of complaints expected to be received. The number of complaints

actually settled during the year has been lower than was expected, resulting in a reduction to the provision held at 26 February 2011 of £50m. We will

continue to handle claims and redress customers in accordance with PS 10/12 (see note 1). This will include ongoing analysis of historical claims

experience in accordance with the guidance.

The calculation of this provision involves estimating a number of variables, principally the level of customer complaints which may be received and the

level of any compensation which may be payable to customers. Uncertainty associated with these factors may result in the ultimate liability being

different from the reported provision.

On 9 October 2010, the British Bankers Association (BBA) applied to the courts for a judicial review in which they sought to overturn Policy Statement

10/12 issued by the FSA during the year in respect of PPI. On the 20 April 2011, the BBA lost their challenge on all grounds. The BBA have not yet

publicly announced whether they intend to appeal the decision. The provision at 26 February 2011 did not assume a favourable outcome for the BBA.

FINANCIAL STATEMENTS

134

—

TESCO PLC Annual Report and Financial Statements 2011

Notes to the Group financial statements