SunTrust 2005 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2005 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

SUNTRUST ANNUAL REPORT 97

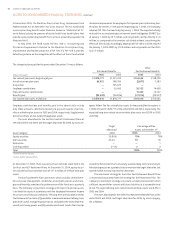

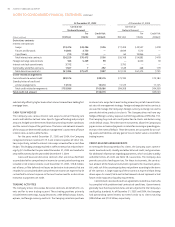

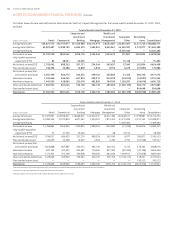

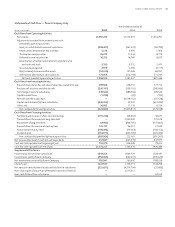

NOTE • Concentrations of Credit Risk

Credit risk represents the maximum accounting loss that would be recog-

nized at the reporting date if borrowers failed to perform as contracted and

any collateral or security proved to be of no value. Concentrations of credit

risk (whether on- or off-balance sheet) arising from financial instruments

can exist in relation to individual borrowers or groups of borrowers, certain

types of collateral, certain types of industries, certain loan products, or cer-

tain regions of the country. Credit risk associated with these concentrations

could arise when a significant amount of loans, related by similar character-

istics, are simultaneously impacted by changes in economic or other con-

ditions that cause their probability of repayment to be adversely affected.

The Company does not have a significant concentration to any individual

client except for the U.S. government and its agencies. The major concen-

trations of credit risk for the Company arise by collateral type in relation

to loans and credit commitments. The only significant concentration that

exists is in loans secured by residential real estate. At December , ,

the Company had . billion in residential real estate loans, represent-

ing .% of total loans, and an additional . billion in commitments

to extend credit on such loans. The Company originates and retains certain

residential mortgage loan products that include features such as interest

only loans, high loan to value loans and low initial interest rate loans, which

comprised approximately % of loans secured by residential real estate.

The risk in each loan type is mitigated and controlled by managing the tim-

ing of payment shock, private mortgage insurance and underwriting guide-

lines. A geographic concentration arises because the Company operates

primarily in the Southeastern and Mid-Atlantic regions of the United States.

SunTrust engages in limited international banking activities. The

Company’s total cross-border outstandings were . million as of

December , .

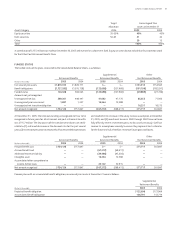

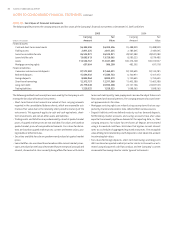

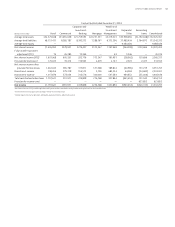

from a client’s failure to fulfill their contractual obligations. As the clear-

ing broker’s rights to charge STIS and STCM have no maximum amount,

the Company believes that the maximum potential obligation cannot be

estimated. However, to mitigate exposure, the affiliate may seek recourse

through cash or securities held in the defaulting clients’ accounts. For the

year ended December , , SunTrust experienced minimal net losses

as a result of the indemnity. The clearing agreements for STIS and STCM

expire in May .

The Company has guarantees associated with credit default swaps,

an agreement in which the buyer of protection pays a premium to the

seller of the credit default swap for protection against an event of default.

Events constituting default under such agreements that would result in the

Company making a guaranteed payment to a counterparty may include: (i)

default of the referenced asset; (ii) bankruptcy of the client; or (iii) restruc-

turing or reorganization by the client. The notional amount outstanding

as of December , and December , was . million

and . million, respectively. As of December , , the notional

amounts expire as follows: . million in , . million in ,

. million in , . million in , . million in ,

and . million in . In the event of default under the contract, the

Company would make a cash payment to the holder of credit protection

and would take delivery of the referenced asset from which the Company

may recover a portion of the credit loss. In addition, there are certain

purchased credit default swap contracts that mitigate a portion of the

Company’s exposure on written contracts. Such contracts are not included

in this disclosure since they represent benefits to, rather than obligations of,

the Company.