SunTrust 2005 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2005 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

•In Wealth and Investment Management, we introduced a

new client management operating model in Private Wealth

Management and consolidated our brokerage and investment

units under one broker/dealer, SunTrust Investment Services, to

improve efficiency and build on our demonstrated competencies.

In the same vein, we streamlined administrative, recordkeeping

and investment capabilities for institutional customers. Asset

Management Advisors, SunTrust’s family office, added a location

in Tampa and, late in the year, announced several key executive

appointments to help position SunTrust for national leadership

in this high-potential business.

•In Mortgage Banking, underscoring our national reach in this

business line, we opened 51 new mortgage offices and increased

the size of the sales force by almost 24 percent, moves that will

allow us to grow market share and purchase-loan originations

faster than our peers. We are proud that in 2005, the well-

respected J.D. Power and Associates ranked SunTrust Mortgage

“Highest in Customer Satisfaction among Mortgage Servicing

Companies” and number two in overall customer satisfaction in

the 2005 primary mortgage origination study.

We intensified our focus on talent management, a structured

process that takes traditional succession planning to a higher level

by explicitly aligning talent development with business strategies.

Specifically, the capabilities of more than 5,600 key managers across

the Company have been assessed in the context of defined leadership

competencies, future potential and performance. The result is not

only “bench strength” for top positions throughout the organization

today, but meaningful development plans for an upcoming leader-

ship generation. More broadly, our disciplined approach to talent

management is reflected in an unusually high degree of success in

hiring, retaining, and rewarding strong candidates in all areas of our

organization — including the critical and evolving risk and compliance-

related fields.

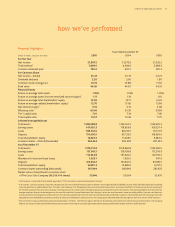

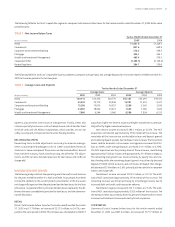

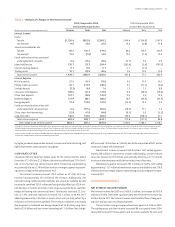

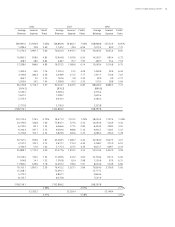

Financial Highlights

A quick look at some key components of our 2005 earnings com-

pared with prior periods suggests the business line momentum that

contributed to the strong bottom line earnings growth we reported

last year. Since 2005 financial results reflect our acquisition of the

former NCF, we have estimated historical results in examples that

follow as if NCF and SunTrust results had been combined in the ear-

lier periods as well. This permits meaningful comparisons while also

providing a more accurate picture of our underlying earnings power.

•Loans – Loan growth was robust in most segments of the

portfolio — up 13% from 2004—and particularly strong in home

equity loans and mortgages. While the mortgage industry was

challenged by a drop-off in refinancing activity as a result of

rising interest rates, SunTrust grew mortgages over the prior

year end and achieved record production volume. We believe a

significant portion of this growth was achieved by taking market

share from our competitors, reflecting investments in new business

generation capacity. We also grew commercial and construction

lending. SunTrust ranks first or second in primary banking

relationships among “middle market” companies — those with

$5 million to $250 million in revenue — in 60 percent of our

geographic markets, which provides a platform for continued

growth in this key segment. Furthermore, larger corporate lend-

ing rebounded in 2005.

•Deposits –The benefit of our emphasis on sales and retention is

perhaps most evident in deposit growth, where we place a priority

on attracting and expanding relationship-based accounts that

can lead to the sales of additional products and services. Overall

average commercial and consumer deposit growth was up a

healthy seven percent over 2004. As interest rates rose during

the year, customer preference predictably shifted to higher-

paying deposit accounts such as money market and CD

products.

We moved to capitalize on this trend by launching several high-

ly successful targeted sales campaigns throughout 2005 that

significantly boosted CD and money market accounts. We also

benefit from non-traditional deposit sources: for example, new

deposit accounts booked by our SunTrust Online call centers

were up 61 percent in 2005. Initiatives such as our in-store

relationships and our continued focus on sales and retention will

set the tone for deposit generation efforts in 2006.

SUNTRUST 2005 ANNUAL REPORT 15

13%

7%

Total Average Loan

Growth in 2005

Total Average Consumer

& Commercial Deposit

Growth in 2005

SALES FOCUS PAYS OFF

Growth in average loans and consumer and commercial deposits

reflects the positive impact of SunTrust’s focus on sales

and retention.