SunTrust 2005 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2005 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

SUNTRUST ANNUAL REPORT70

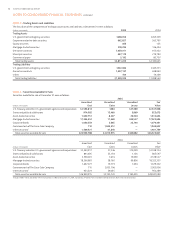

NOTE • Accounting Policies

GENERAL

SunTrust, one of the nation’s largest commercial banking organizations, is a

financial services holding company with its headquarters in Atlanta, Georgia.

SunTrust’s principal banking subsidiary, SunTrust Bank, which includes the

former National Bank of Commerce, offers a full line of financial services for

consumers and businesses through its branches located primarily in Florida,

Georgia, Maryland, North Carolina, South Carolina, Tennessee, Virginia,

West Virginia and the District of Columbia. Within its geographic footprint,

the Company operates under five business segments. These business seg-

ments are: Retail, Commercial, Corporate and Investment Banking, Wealth

and Investment Management, and Mortgage. In addition to traditional

deposit, credit and trust and investment services offered by SunTrust Bank,

other SunTrust subsidiaries provide mortgage banking, credit-related insur-

ance, asset management, securities brokerage and capital market services.

PRINCIPLES OF CONSOLIDATION AND BASIS OF PRESENTATION

The consolidated financial statements include the accounts of the

Company, its majority-owned subsidiaries, and variable interest enti-

ties (“VIEs”) where the Company is the primary beneficiary. All significant

intercompany accounts and transactions have been eliminated. Results of

operations of companies purchased are included from the date of acquisi-

tion. Assets and liabilities of purchased companies are stated at estimated

fair values at the date of acquisition. Investments in companies which are

not VIEs, or where SunTrust is not the primary beneficiary in a VIE, that the

Company owns a voting interest of % to %, and for which it may have

significant influence over operating and financing decisions, are accounted

for using the equity method of accounting. These investments are included

in other assets, and the Company’s proportionate share of income or loss

is included in other noninterest income in the Consolidated Statements of

Income.

The preparation of financial statements in conformity with account-

ing principles generally accepted in the United States (“US GAAP”) requires

management to make estimates and assumptions that affect the reported

amounts of assets and liabilities, the disclosure of contingent assets and

liabilities at the date of the financial statements and the reported amounts

of revenues and expenses during the reporting period. Actual results could

vary from these estimates. Certain reclassifications have been made to prior

year amounts to conform to the presentation.

CASH AND CASH EQUIVALENTS

Cash and cash equivalents include cash and due from banks, interest-bear-

ing bank balances, federal funds sold and securities purchased under agree-

ments to resell. Generally, cash and cash equivalents have maturities of

three months or less, and accordingly, the carrying amount of these instru-

ments is deemed to be a reasonable estimate of fair value.

SECURITIES AND TRADING ACTIVITIES

Securities are classified at trade date as trading or available for sale

securities.

Securities available for sale are used as part of the overall asset and

liability management process to optimize income and market performance

over an entire interest rate cycle. Interest income and dividends on securi-

ties are recognized in interest income on an accrual basis. Premiums and

discounts on debt securities are amortized as an adjustment to yield over

the life of the security. Securities available for sale are carried at fair value

with unrealized gains and losses, net of any tax effect, included in accumu-

lated other comprehensive income as a component of shareholders’ equity.

Realized gains and losses on securities are determined using the specific

identification method and are recognized currently in the Consolidated

Statements of Income. The Company reviews available for sale securities

for impairment on a quarterly basis. The Company determines whether a

decline in fair value below the amortized cost basis is other-than-tempo-

rary. An available for sale security that has been other-than-temporarily

impaired is written down to fair value, and the amount of the write down is

accounted for as a realized loss in the Consolidated Statements of Income.

Securities that are bought and held principally for the purpose of

resale in the near future are classified as trading instruments. Trading

account assets and liabilities are carried at market value. Realized and

unrealized gains and losses are determined using the specific identification

method and are recognized as a component of noninterest income in the

Consolidated Statements of Income.

Nonmarketable securities include venture capital equity and mezza-

nine securities that are not publicly traded as well as equity investments

acquired for various purposes. These securities are accounted for under

the cost or equity method and are included in other assets. The Company

reviews nonmarketable securities accounted for under the cost method

on a quarterly basis and reduces the asset value when declines in value are

considered to be other-than-temporary. Equity method investments are

recorded at cost adjusted to reflect the Company’s portion of income, loss

or dividends of the investee. Realized income, realized losses and estimated

losses on cost and equity method investments are recognized in noninter-

est income in the Consolidated Statements of Income.

LOANS HELD FOR SALE

Loans held for sale that are not documented as the hedged item in a fair

value hedge are carried at the lower of cost or fair value at the pool level

based on similar assets criteria. Adjustments to reflect market value and

realized gains and losses upon ultimate sale of the loans are classified as

other noninterest income in the Consolidated Statements of Income.

Loans held for sale that are documented as the hedged item in a fair

value hedge are carried at fair value. Fair value is based on an observable

current market price. Unrealized gains and losses are recorded as a compo-

nent of noninterest income in the Consolidated Statements of Income.

The Company transfers certain residential mortgage loans, commer-

cial loans, and student loans to a held for sale classification at the lower of

cost or market. At the time of transfer, any losses are recorded through the

provision for loan losses with subsequent losses recorded as a component

of noninterest expense in the Consolidated Statements of Income.

LOANS

The Company’s loan balance is comprised of loans held in portfolio, includ-

ing commercial loans, consumer loans, real estate loans and lines, factor-

ing receivables, credit card receivables, nonaccrual and restructured loans,

direct financing leases, and leveraged leases. Interest income on all types

of loans is accrued based upon the outstanding principal amounts, except

those classified as nonaccrual loans. The Company typically classifies loans

as nonaccrual when one of the following events occurs: (i) interest or princi-

pal has been in default days or more, unless the loan is well-secured and

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS