SunTrust 2005 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2005 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

SUNTRUST ANNUAL REPORT 71

in the process of collection; (ii) collection of recorded interest or principal is

not anticipated; or (iii) income for the loan is recognized on a cash basis due

to the deterioration in the financial condition of the debtor. Consumer and

residential mortgage loans are typically placed on nonaccrual when pay-

ments have been in default for and days or more, respectively.

When a loan is placed on nonaccrual, unpaid interest is reversed

against interest income. Interest income on nonaccrual loans, if recognized,

is either recorded using the cash basis method of accounting or recognized

at the end of the loan after the principal has been reduced to zero, depend-

ing on the type of loan. If and when borrowers demonstrate the ability to

repay a loan in accordance with the contractual terms of a loan classified

as nonaccrual, the loan may be returned to accrual status. If a nonaccrual

loan is returned to accruing status, the accrued interest at the date the loan

is placed on nonaccrual status, and foregone interest during the nonaccrual

period, are recorded as interest income only after all principal has been col-

lected for commercial loans. For consumer loans and residential mortgage

loans, the accrued interest at the date the loan is placed on nonaccrual

status, and forgone interest during the nonaccrual period, are recorded as

interest income as of the date the loan no longer meets the and day

past due criteria. (See Allowance for Loan and Lease Losses section of this

Note for further discussion of impaired loans.)

Fees and incremental direct costs associated with the loan origination

and pricing process, as well as premiums and discounts, are deferred and

amortized as level yield adjustments over the respective loan terms. Fees

received for providing loan commitments that result in loans are deferred

and then recognized over the term of the loan as an adjustment of the

yield.

ALLOWANCE FOR LOAN AND LEASE LOSSES

The Company’s allowance for loan and lease losses is the amount con-

sidered adequate to absorb probable losses within the portfolio based on

management’s evaluation of the size and current risk characteristics of the

loan portfolio. Such evaluation considers prior loss experience, the risk rat-

ing distribution of the portfolios, the impact of current internal and exter-

nal influences on credit loss and the levels of nonperforming loans. Specific

allowances for loan and lease losses are established for large impaired loans

on an individual basis as required per Statement of Financial Accounting

Standard (“SFAS”) No. , “Accounting by Creditors for Impairment

of a Loan—an amendment of FASB Statements No. and ,” and SFAS

No. , “Accounting by Creditors for Impairment of a Loan-Income

Recognition and Disclosures—an amendment of FASB Statement No.

,” and large impaired leases based on the criteria set forth in SFAS No.

, “Accounting for Contingencies.” The specific allowance established for

these loans and leases is based on a thorough analysis of the most probable

source of repayment, including the present value of the loan’s expected

future cash flows, the loan’s estimated market value, or the estimated fair

value of the underlying collateral. General allowances are established for

loans and leases that can be grouped into pools based on similar character-

istics as described in SFAS No. . In this process, general allowance factors

are based on an analysis of historical charge-off experience and expected

losses given default derived from the Company’s internal risk rating process.

These factors are developed and applied to the portfolio in terms of line

of business and loan type. Adjustments are also made to the allowance for

the pools after an assessment of internal and external influences on credit

quality that have not yet been reflected in the historical loss or risk rating

data. Non-pool-specific allowances relate to inherent losses that are not

otherwise evaluated in the first two elements. The qualitative factors asso-

ciated with the non-pool-specific allowances are subjective and require a

high degree of management judgement. These factors include the inherent

imprecisions in mathematical models and credit quality statistics, recent

economic uncertainty, losses incurred from recent events, and lagging or

incomplete data.

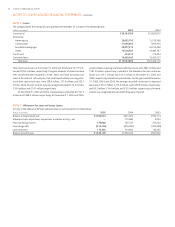

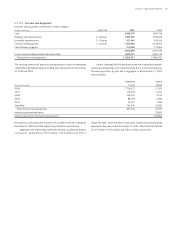

PREMISES AND EQUIPMENT

Premises and equipment are carried at cost less accumulated depreciation

and amortization. Depreciation is calculated primarily using the straight-

line method over the assets’ estimated useful lives. Certain leases are capi-

talized as assets for financial reporting purposes. Such capitalized assets

are amortized, using the straight-line method, over the terms of the leases.

Maintenance and repairs are charged to expense, and improvements are

capitalized.

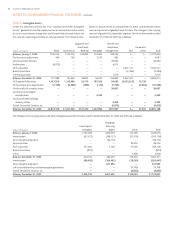

GOODWILL AND OTHER INTANGIBLE ASSETS

Goodwill represents the excess of purchase price over the fair value of iden-

tifiable net assets of acquired companies. Under the provisions of SFAS No.

, “Goodwill and Other Intangible Assets,” goodwill is not amortized and

instead is subject to impairment testing on an annual basis, or more often if

events or circumstances indicate that there may be impairment. The good-

will impairment test is performed in two phases. The first phase is used to

identify potential impairment and the second phase, if required, identifies

the amount of impairment by comparing the carrying amount of goodwill

to its implied fair value.

Identified intangible assets that have a finite life are amortized over

their useful lives and are evaluated for impairment whenever events or

changes in circumstances indicate the carrying amount of the assets may

not be recoverable.

MORTGAGE SERVICING RIGHTS “MSRs”

The Company recognizes as assets the rights to service mortgage loans for

others whether the servicing rights are acquired through purchase or loan

origination. Purchased MSRs are capitalized at cost. For loans originated

and sold where the servicing rights have been retained, the Company allo-

cates the cost of the loan and the servicing rights based on their relative

fair market values at the time of sale of the underlying mortgage loan. Fair

value is determined through a review of valuation assumptions that are

supported by market and economic data collected from various outside

sources. The carrying value of MSRs is maintained on the balance sheet in

intangible assets.

There are two components to the amortization expense that the

Company records on MSRs. First, the Company fully amortizes the remaining

balance of all MSR assets for loans paid in full in recognition of the termina-

tion of future cash flow streams. Second, amortization on the surviving MSR

assets is recorded based on the current cash flows as estimated by future

net servicing income. The current cash flows are calculated and updated

monthly by applying market-driven assumptions, such as interest rate and

prepayment speed assumptions. Impairment for MSRs is determined based

on the fair value of the rights, stratified according to interest rate and type

of related loan. Impairment, if any, is recognized through a valuation allow-

ance with a corresponding charge recorded in the Consolidated Statements

of Income.