SunTrust 2005 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2005 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

SUNTRUST ANNUAL REPORT40

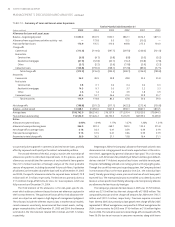

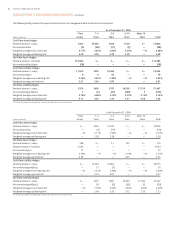

The following table presents the expected maturities of risk management derivative financial instruments:

As of December ,

Year – – – After

(Dollars in millions) or Less Years Years Years Years Total

Cash Flow Asset Hedges

Notional amount – swaps , — ,

Net unrealized loss () () () () — ()

Weighted average receive fixed rate .% .% .% .% —% .%

Weighted average pay floating rate . . . . — .

Fair Value Asset Hedges

Notional amount – forwards , — — — — ,

Net unrealized (loss)/gain () — — — — ()

Cash Flow Liability Hedges

Notional amount – swaps , , — — ,

Net unrealized gain — —

Weighted average receive floating rate .% .% .% —% —% .%

Weighted average pay fixed rate . . . — — .

Fair Value Liability Hedges

Notional amount – swaps , , ,

Net unrealized gain/(loss) () () () ()

Weighted average receive fixed rate .% .% .% .% .% .%

Weighted average pay floating rate . . . . . .

All interest rate swaps have variable pay or receive rates with resets of six months or less.

As of December ,

Year – – – After

(Dollars in millions) or Less Years Years Years Years Total

Cash Flow Asset Hedges

Notional amount – swaps — , — — ,

Net unrealized loss — () () — — ()

Weighted average receive fixed rate —% .% .% —% —% .%

Weighted average pay floating rate — . . — — .

Fair Value Asset Hedges

Notional amount – swaps — — —

Notional amount – forwards , — — — — ,

Net unrealized gain — — —

Weighted average receive floating rate .% —% —% .% —% .%

Weighted average pay fixed rate . — — . — .

Cash Flow Liability Hedges

Notional amount – swaps — , , — — ,

Net unrealized gain/(loss) — () — —

Weighted average receive floating rate —% .% .% —% —% .%

Weighted average pay fixed rate — . . — — .

Fair Value Liability Hedges

Notional amount – swaps — , , ,

Net unrealized gain/(loss) — () () ()

Weighted average receive fixed rate —% .% .% .% .% .%

Weighted average pay floating rate — . . . . .

All interest rate swaps have variable pay or receive rates with resets of six months or less.

MANAGEMENT’S DISCUSSION AND ANALYSIS continued