Rogers 2008 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2008 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

48 ROGERS COMMUNICATIONS INC. 2008 ANNUAL REPORT

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

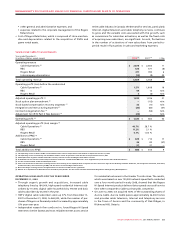

The increase in Cable Operations PP&E additions for 2008, com-

pared to 2007, is primarily attributable to a larger subscriber base,

increased demand for high-speed Internet access and the deploy-

ment of new technologies. This resulted in increased spending on

scalable infrastructure related to, amongst other things, network

capacity and investment in switched-digital technology, as well

as increased support capital. The year-over-year increase in sup-

port capital reflects higher investments in IT initiatives. Spending

on CPE decreased in 2008, compared to 2007, resulting from lower

additions of RGUs compared to 2007.

The reduction in RBS PP&E additions for 2008, compared to 2007,

reflects the refocusing of RBS’ business as discussed above.

Rogers Retail PP&E additions are attributable to improvements

made to certain retail locations.

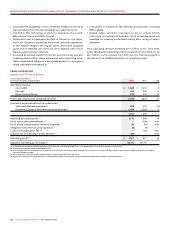

MEDIA

MEDIA’S BUSINESS

Media operates our radio and television broadcasting businesses,

our consumer and trade publishing operations, our televised home

shopping service and Rogers Sports Entertainment. In addition to

Media’s more traditional broadcast and print media platforms, it

also delivers content and conducts e-commerce over the Internet.

Media’s broadcasting group (“Broadcasting”) comprises 52 radio

stations across Canada; multicultural OMNI television stations;

the five station Citytv television network; specialty sports televi-

sion services including regional sports service Rogers Sportsnet

and Setanta Sports Canada; specialty services including OLN, The

Biography Channel Canada and G4TechTV Canada; and Canada’s

only nationally televised shopping service (“The Shopping

Channel”). Media also holds 50% ownership in Dome Productions,

a mobile production and distribution joint venture that is a leader

in HDTV production in Canada.

In addition to its organic growth, Media expanded its broadcasting

business in 2008 through the following initiatives: the acquisition

of the remaining two-thirds of the shares of OLN that it did not

already own, the acquisition of Vancouver multicultural televi-

sion station channel m, the pending purchase of CFDR-AM Halifax

(which has received CRTC approval to convert to FM) and the launch

of two OMNI stations in Alberta.

Media’s publishing group (“Publishing”) publishes more than 70

consumer magazines and trade and professional publications and

directories in Canada.

Media’s sports entertainment group (“Sports Entertainment”)

owns the Blue Jays and Rogers Centre.

MEDIA’S STRATEGY

Media seeks to maximize revenues, operating profit and return on

invested capital across each of its businesses. Media’s strategies to

achieve this objective include:

• Continuingtoleverageitsstrongmediabrandnamesandcon-

tent over its multiple media platforms and in association with

the “Rogers” brand;

• Focusing on specialized content and audience development

through its broadcast, publication and sports properties, as well

as its growing portfolio of specialty channel investments;

• Investingintechnologyandcontenttosupportaudiencemigra-

tion to the web, wireless and other mobile platforms; and

• EnhancingtheSportsEntertainmentfanexperiencebyadding

talented players to improve the Blue Jays win-loss record and by

investing in upgrades to the Rogers Centre.

RECENT MEDIA INDUSTRY TRENDS

Increased Fragmentation of Radio and TV Markets

In recent years, Canadian radio and television broadcasters have

had to operate in increasingly fragmented markets. Canadian con-

sumers have a growing number of radio and television services

available to them, providing them with an increasing number of

different programming formats. In the radio industry, since the

introduction of its Commercial Radio Policy in 1998, the CRTC has

licenced numerous new radio stations through competitive pro-

cesses in most markets across Canada. In that time, the CRTC has

also licenced a large number of additional new FM stations through

AM to FM station conversions. In 2005, the CRTC licenced two satel-

lite radio providers, both of which are affiliated with U.S. satellite

operators and both of which began offering service in Canada. In

the television industry since 2000, the CRTC has licenced a small

number of new, over-the-air stations and a significant number of

new digital television services. The new services, additional licences

and the new formats combine to fragment the market for existing

radio and television operators.

Consolidation of Industry Competitors

Ownership of Canadian radio and TV stations has consolidated

through the acquisitions by CTVglobemedia of CHUM Limited,

by Canwest Global Communications Corp. of Alliance Atlantis

Communications Inc., and by Astral Media Inc. of Standard Radio

Inc. This results in the Canadian industry being left with fewer

owners but larger competitors in the media marketplace.

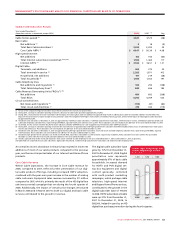

MEDIA OPERATING AND FINANCIAL RESULTS

Media’s revenues primarily consist of:

• Advertisingrevenues;

• Circulationrevenues;

• Subscriptionrevenues;

• Retailproductsales;and

• Salesoftickets,receiptsofleaguerevenuesharingandconces-

sion sales associated with Rogers Sports Entertainment.

2008 MEDIA REVENUE MIX

(%)

Radio 18%

The Shopping Channel 18%

Television 30%

Publishing 20%

Sports Entertainment 14%