Rogers 2008 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2008 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

110 ROGERS COMMUNICATIONS INC. 2008 ANNUAL REPORT

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

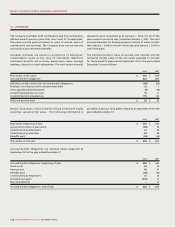

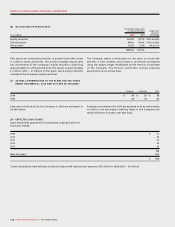

Cross- Cross-

Currency Currency

Swaps in an Swaps in a Net

asset liability liability

position position position

(A) (B) (A) + (B)

Mark-to-market value – risk-free analysis $ 572 $ (716) $ (144)

Mark-to-market value – credit-adjusted estimate (carrying value) 507 (661) (154)

Difference $ (65) $ 55 $ (10)

amount of Senior Notes due 2018 from a fixed coupon rate of 6.80%

into Cdn. $1,435 million at a weighted average fixed interest rate of

6.80%; and (b) converting the U.S. $350 million aggregate principal

amount of Senior Notes due 2038 from a fixed coupon rate of 7.50%

into Cdn. $359 million at a weighted average fixed interest rate of

7.53%. The Cross-Currency Swaps hedging the Senior Notes due 2018

have been designated as effective hedges against the designated

U.S. dollar-denominated debt for accounting purposes, while the

Cross-Currency Swaps hedging the Senior Notes due 2038 have not

been designated as hedges for accounting purposes.

Also effective on August 6, 2008, the Company re-couponed three

of its existing Cross-Currency Swaps by terminating the original

Cross-Currency Swaps aggregating U.S. $575 million notional

principal amount and simultaneously entering into three new Cross-

Currency Swaps aggregating U.S. $575 million notional principal

amount at then current market rates. In each case, only the fixed

foreign exchange rate and the Canadian dollar fixed interest rate

were changed and all other terms for the new Cross-Currency

Swaps are identical to the respective terminated Cross-Currency

Swaps they are replacing. The termination of the three original

Cross-Currency Swaps resulted in the Company paying U.S. $360

million (Cdn. $375 million) for the aggregate out-of-the-money

fair value for the terminated Cross-Currency Swaps on the date of

termination, thereby reducing by an equal amount, the fair value

of the derivative instruments liability on that date. The three new

Cross-Currency Swaps have the effect of converting U.S. $575 million

aggregate notional principal amount of U.S. dollar denominated

debt from a weighted average U.S. dollar fixed interest rate of

7.20% into notional Cdn. $589 million ($1.025 exchange rate) at a

weighted average Canadian dollar fixed interest rate of 6.88%. In

comparison, the original Cross-Currency Swaps had the effect of

converting U.S. $575 million aggregate notional principal amount

of U.S. dollar-denominated debt from a weighted average U.S.

dollar fixed interest rate of 7.20% into notional Cdn. $815 million

($1.4177 exchange rate) at a weighted average Canadian dollar

fixed interest rate of 7.89%. Each of the three new Cross-Currency

Swaps has been designated as a hedge against the designated U.S.

dollar-denominated debt for accounting purposes.

Prior to the termination of the Cross-Currency Swaps noted

above, changes in the fair value of these Cross-Currency Swaps

had been recorded in accumulated other comprehensive

income and were periodically reclassified to income to offset

foreign exchange gains or losses on related debt or to modify

interest expense to its hedged amount. The remaining balance

in accumulated other comprehensive income relating to these

terminated Cross-Currency Swaps on the termination date was

$144 million. The portion related to future periodic exchanges

of interest of $68 million, net of income taxes of $26 million, will

be recorded in income over the remaining life of the specific

debt securities to which the settled hedging items related

using the effective interest rate method. The portion of the

remaining balance that relates to the future principal exchange

of $43 million, net of income taxes of $7 million, will remain in

accumulated other comprehensive income until such time as the

related debt is settled. The total amortization of re-couponed

Cross-Currency Swaps is $3 million for 2008 and is recorded in

interest expense.

In addition, two Cross-Currency Swaps matured on December 15,

2008. These Cross-Currency Swaps hedged the foreign exchange

risk related to the U.S. $400 million 8.00% Senior Subordinated

Notes due 2012. As a result of the maturity of these Cross-Currency

Swaps, the Company’s U.S. $400 million 8.00% Senior Subordinated

Notes due 2012 are no longer hedged. Proceeds of $494 million

(U.S. $400 million) were received on the settlement of the Cross-

Currency Swaps and a payment of $475 million was made. In

addition, upon settlement of forward foreign exchange contracts on

December 15, 2008, proceeds of $476 million were received and

payments on the forward contracts of $494 million (U.S. $400 million)

were made.

The effect of estimating the credit-adjusted fair value of Cross-

Currency Swaps at December 31, 2008 is illustrated in the table

below. As at December 31, 2008, the net liability of the Company’s

swap portfolio increased by $10 million to $154 million versus the

net liability calculated using risk-free rates. The increase in the

net liability is a result of the estimated fair value of the Cross-

Currency Swaps in an asset position decreasing by $65 million

while the estimated fair value of the Cross-Currency Swaps in a

liability position decreased by $55 million. In 2007, the estimated

fair value, being carrying amount, was determined on a risk-

free basis.