Rogers 2008 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2008 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

ROGERS COMMUNICATIONS INC. 2008 ANNUAL REPORT 111

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

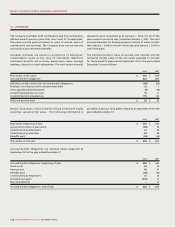

At December 31, 2008, 87.4% of the Company’s U.S. dollar-

denominated long-term debt instruments were hedged against

fluctuations in foreign exchange rates for accounting purposes.

At December 31, 2008, details of the derivative instruments net

liability are as follows:

Of the $10 million change, $7 million was recorded in the

consolidated statements of income related to Cross-Currency

Swaps not accounted for as hedges and $3 million related to Cross-

Currency Swaps accounted for as hedges was recorded in other

comprehensive income.

Estimated

Unadjusted fair value,

mark-to- being

market carrying

value amount on

on a a credit risk

U.S. $ Exchange Cdn. $ risk-free adjusted

2008 notional rate notional basis* basis*

Cross-Currency Swaps accounted for as cash flow hedges:

As assets $ 1,975 1.0252 $ 2,025 $ 492 $ 435

As liabilities 3,215 1.3337 4,288 (712) (658)

Subtotal, net mark-to-market asset (liability) 5,190 1.2163 6,313 (220) (223)

Cross-Currency Swaps not accounted for as hedges:

As assets 350 1.0258 359 79 72

As liabilities 10 1.5370 15 (3) (3)

Subtotal, net mark-to-market asset 360 1.0400 374 76 69

Total notional amounts, net mark-to-market asset (liability) $ 5,550 1.2049 $ 6,687 $ (144) $ (154)

Less current portion (45)

$ (109)

*In 2007, the estimated fair value, being carrying amount, was determined on a risk-free basis.

In 2008, $3 million (2007 - $1 million) related to hedge ineffectiveness

was recognized as a decrease in net income.

The long-term portion above is comprised of a derivative

instruments liability of $616 million and a derivative instruments

asset of $507 million.

At December 31, 2007, details of the derivative instruments liability

are as follows:

Estimated

fair value,

being

carrying

amount on

U.S. $ Exchange Cdn. $ a risk-free

2007 notional rate notional basis

Cross-Currency Swaps accounted for as cash flow hedges $ 4,190 1.3313 $ 5,578 $ 1,798

Cross-Currency Swaps not accounted for as hedges 10 1.5370 15 6

$ 4,200 $ 5,593 1,804

Less current portion 195

$ 1,609