Rogers 2008 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2008 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

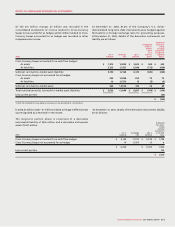

ROGERS COMMUNICATIONS INC. 2008 ANNUAL REPORT 109

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Carrying Contractual Less than 1 to 3 4 to 5 More than

amount cash flows 1 year years years 5 years

Bank advances, including outstanding cheques $ 19 $ 19 $ 19 $ – $ – $ –

Accounts payable and accrued liabilities 2,412 2,412 2,412 – – –

Bank credit facility 585 585 – – 585 –

Other long-term debt 7,910 7,910 1 1,235 1,923 4,751

Other long-term liabilities 184 184 4 81 43 56

Derivative instruments:

Cash outflow (Canadian dollar) 6,687 – 780 1,570 4,337

Cash inflow

(Canadian dollar equivalent of U.S. dollar) (6,796) – (612) (1,433)* (4,751)*

Net cash flows of derivative instruments 154 (109) – 168 137 (414)

$ 11,264 $ 11,001 $ 2,436 $ 1,484 $ 2,688 $ 4,393

*Represents Canadian dollar equivalent amount of U.S. dollar inflows matched to an equal amount of U.S. dollar maturities in “other long-term debt”.

The following are the contractual maturities, excluding interest

payments, reflecting undiscounted disbursements of the Company’s

financial liabilities at December 31, 2008:

Less than 1 to 3 4 to 5 More than

1 year years years 5 years

Interest payments $ 618 $ 1,188 $ 797 $ 1,742

In addition to the amounts noted above, at December 31, 2008,

net interest payments over the life of the long-term debt and bank

credit facility, including derivative instruments, are:

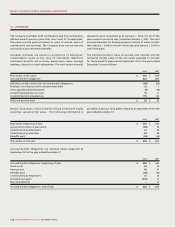

(D) MARKET RISK:

Market risk is the risk that changes in market prices, such as

fluctuations in the market prices of the Company’s publicly traded

investments, the Company’s share price, foreign exchange rates

and interest rates, will affect the Company’s income or the value of

its financial instruments.

(i) Publicly traded investments:

The Company manages its risk related to fluctuations in the

market prices of its publicly traded investments by regularly

conducting financial reviews of publicly available information

related to its publicly traded investments to ensure that

any risks are within established levels of risk tolerance. The

Company does not routinely engage in risk management

practices such as hedging, derivatives or short selling with

respect to its publicly traded investments.

At December 31, 2008, a $1 change in the market price per

share of the Company’s publicly traded investments would

have resulted in an $8 million change in the Company’s other

comprehensive income, net of income taxes of $2 million.

(ii) Company’s share price:

In addition, market risk arises from accounting for the

Company’s stock-based compensation. All of the Company’s

outstanding stock options are classified as liabilities and

are carried at their intrinsic value, as adjusted for vesting,

measured as the difference between the current share price

and the option exercise price. The intrinsic value of the

liability is marked-to-market each period, and stock-based

compensation expense is impacted by the change in the price

of the Company’s Class B Non-Voting shares during the life of

the option. At December 31, 2008, a $1 change in the market

price of the Company’s Class B Non-Voting shares would have

resulted in a change of $7 million in net income, net of income

taxes of $3 million.

(iii) Foreign exchange and interest rates:

The Company uses derivative financial instruments to manage

risks from fluctuations in exchange rates and interest rates.

These instruments include Cross-Currency Swaps, and, from

time to time, interest rate exchange agreements, foreign

exchange forward contracts and foreign exchange option

agreements. All such agreements are only used for risk

management purposes.

Effective August 6, 2008, in conjunction with the issuance of the

U.S. $1.4 billion Senior Notes due 2018, and the U.S. $350 million

Senior Notes due 2038, the Company entered into an aggregate

U.S. $1.75 billion notional principal amount of Cross-Currency Swaps.

An aggregate U.S. $1.4 billion notional principal amount of these

Cross-Currency Swaps hedge the principal and interest obligations

for the U.S. $1.4 billion Senior Notes due 2018 through to maturity

in 2018, while the remaining U.S. $350 million aggregate notional

principal amount of these Cross-Currency Swaps hedge the principal

and interest obligations on the $350 million Senior Notes due 2038

for 10 years to August 15, 2018. These Cross-Currency Swaps have

the effect of: (a) converting the U.S. $1.4 billion aggregate principal