Rogers 2006 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2006 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

33

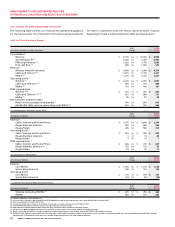

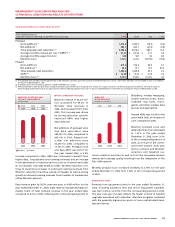

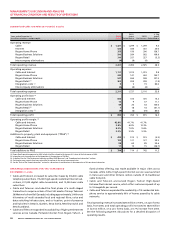

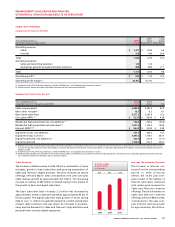

RO GER S CO MMU NIC AT ION S IN C . 20 0 6 ANN UA L RE POR T

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Cable and Telecom’s Dist ribution

In addition to the Rogers Retail stores, as described above, Cable and

Telecom markets its services through an extensive network of third

party retail locations across its network footprint. Effective January 1,

2007, Cable and Telecom acquired approximately 170 Wireless-owned

retail locations. This segment, which is now known as Rogers Retail,

will provide customers with a single direct retail channel featuring

all of the wireless and cable products and services. In addition, Cable

and Telecom markets its services and products through a variety of

channels including outbound telemarketing, field agents, direct mail,

television advertising and affinities. Cable and Telecom also offers

products and services and customer service via its e-business website,

www.rogers.com. The information contained in or connected to our

website is not a part of and not incorporated into this MD&A.

Cable and Telecom markets and sells its business products through

a variety of channels including its own direct sales force, exclusive

and non-exclusive agents as well as through business affinities and

associations.

Cable and Telecom’s Networks

Cable and Telecom’s cable networks in Ontario and New Brunswick,

with few exceptions, are interconnected to regional head-ends, where

analog and digital channel line-ups are assembled for distribution to

customers and Internet traffic is aggregated and routed to and from

customers, by inter-city fibre-optic rings. The fibre-optic interconnec-

tions allow its multiple Ontario and New Brunswick cable systems

to function as a single cable network. Cable and Telecom’s remain-

ing subscribers in Newfoundland and Labrador, and New Brunswick

are served by local head-ends. Cable and Telecom’s two regional

head-ends in Toronto, Ontario and Moncton, New Brunswick pro-

vide the source for most television signals used in the cable systems.

Cable and Telecom’s technology architecture is based on a three-

tiered structure of primary hubs, optical nodes and co-axial

distribution. The primary hubs, located in each region that it serves,

are connected by inter-city fibre-optic systems carrying television,

Internet, network control and monitoring and administrative traffic.

The fibre-optic systems are generally constructed as rings that allow

signals to flow in and out of each primary hub, or head-end, through

two paths, providing protection from a fibre cut or other disruption.

These high-capacity fibre-optic networks deliver high performance

and reliability and have capacity for future growth in the form of dark

fibre and unused optical wavelengths. Approximately 99% of the

homes passed by Cable and Telecom’s network are fed from primary

hubs, or head-ends, which each serve on average 93,000 homes. The

remaining 1% of the homes passed by the network are in smaller and

more rural systems mostly in New Brunswick and Newfoundland and

Labrador which are, on average, served by smaller primary hubs.

Optical fibre joins the primary hub to the optical nodes in the cable

distribution plant. Final distribution to subscriber homes from optical

nodes uses co-axial cable with two-way amplifiers to support on-

demand television and Internet service. Co-axial cable capacity has

been increased repeatedly by introducing more advanced amplifier

technologies. Cable and Telecom believes co-axial cable is a cost-

effective and widely deployed means of carrying two-way television

and broadband Internet services to residential subscribers.

Groups of an average of 495 homes are served from each optical

node in a cable architecture commonly referred to as fibre-to-the-

feeder (“FTTF”). The FTTF plant provides bandwidth up to 860 MHz,

which includes 37 MHz of bandwidth used for “upstream” transmis-

sion from the subscribers’ premises to the primary hub. Cable and

Telecom believes the upstream bandwidth is ample to support mul-

tiple cable modem systems, cable telephony, and data traffic from

interactive digital set-top terminals for at least the near term future.

When necessary, additional upstream capacity can be provided by

reducing the number of homes served by each optical node by what

is called node-splitting. Fibre cable has been placed to permit a

reduction of the average node size from 495 to 350 homes by install-

ing additional optical transceiver modules and optical transmitters

and return receivers in the head-ends and primary hubs.

Cable and Telecom believes that the 860 MHz FTTF architecture

provides sufficient bandwidth for foreseeable growth in television,

data, voice and other future services, extremely high picture quality,

advanced two-way capability and network reliability. This architec-

ture also allows for other emerging technologies such as switched

video and MPEG4, and offers the ability to continue to expand ser-

vice offerings on the existing infrastructure. In addition, Cable and

Telecom’s clustered network of cable systems served by regional

head-ends facilitates its ability to rapidly introduce new services

to large areas of subscribers. In new construction projects in major

urban areas, Cable and Telecom is now deploying a cable network

architecture commonly referred to as fibre-to-the-curb (“FTTC”). This

architecture provides improved reliability due to fewer active net-

work devices being deployed. FTTC also provides greater capacity for

future narrowcast services.

Cable and Telecom’s voice-over-cable telephony services are offered

over an advanced broadband IP multimedia network layer deployed

across the cable service areas. This network platform provides for

a scalable primary line quality digital voice-over-cable telephony

service utilizing Packet Cable and Data Over Cable Service Interface

Specification (“DOCSIS”) standards, including network redundancy

as well as multi-hour network and customer premises backup

powering.

To serve telephony customers on circuit-switched platforms, Cable

and Telecom co-locates its equipment in the switch centres of the

incumbent local phone companies (“ILECs”). At December 31, 2006,

Cable and Telecom was active in 175 co-locations in 60 munici-

palities in five of Canada’s most populous metropolitan areas in

and around Vancouver, Calgary, Toronto, Ottawa, and Montreal.

Many of these co-locations are connected to its local switches by metro

area fibre networks (“MANs”). Cable and Telecom also operates a

North American transcontinental fibre-optic network extending over

16,000 route kilometres (10,000 route miles) providing a significant

North American geographic footprint connecting Canada’s larg-

est markets while also reaching key U.S. markets for the exchange

of data and voice traffic. In Canada, the network extends from

Vancouver in the West to Quebec City in the East. Cable and Telecom

also acquired various CLEC assets of GT from Bell Canada in Ontario,

Quebec and Newfoundland and Labrador. The assets include local,

regional and long-haul fibre, transmission electronics and systems,

GT’s hubs, points of presence (“POPs”) and ILEC co-locations, and