Rogers 2006 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2006 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

|

|

101

RO GER S CO MMU NIC AT ION S IN C . 20 0 6 ANN UA L RE POR T

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

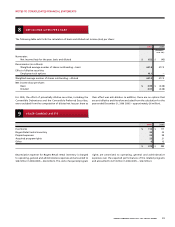

Net plan expense is outlined below:

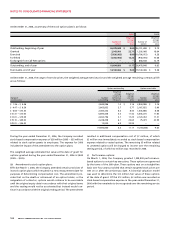

2006 2005

Plan cost:

Service cost $ 24 $ 15

Interest cost 32 30

Actual return on plan assets (40) (67)

Actuarial loss (gain) on benefit obligation (12) 82

Costs 4 60

Differences between costs arising during the year and costs recognized during the year in respect of:

Return on plan assets 7 37

Actuarial loss (gain) 22 (74)

Plan amendments/prior service cost 1 1

Transitional asset (10) (10)

Net pension expense $ 24 $ 14

December 31, 2006 (2005 – $18 million) and related expense for 2006

was $4 million (2005 – $3 million).

The Company also provides supplemental unfunded pension ben-

efits to certain executives. The accrued benefit obligation relating to

these supplemental plans amounted to approximately $19 million at

(A) ACTUARIAL ASSUMP TIONS:

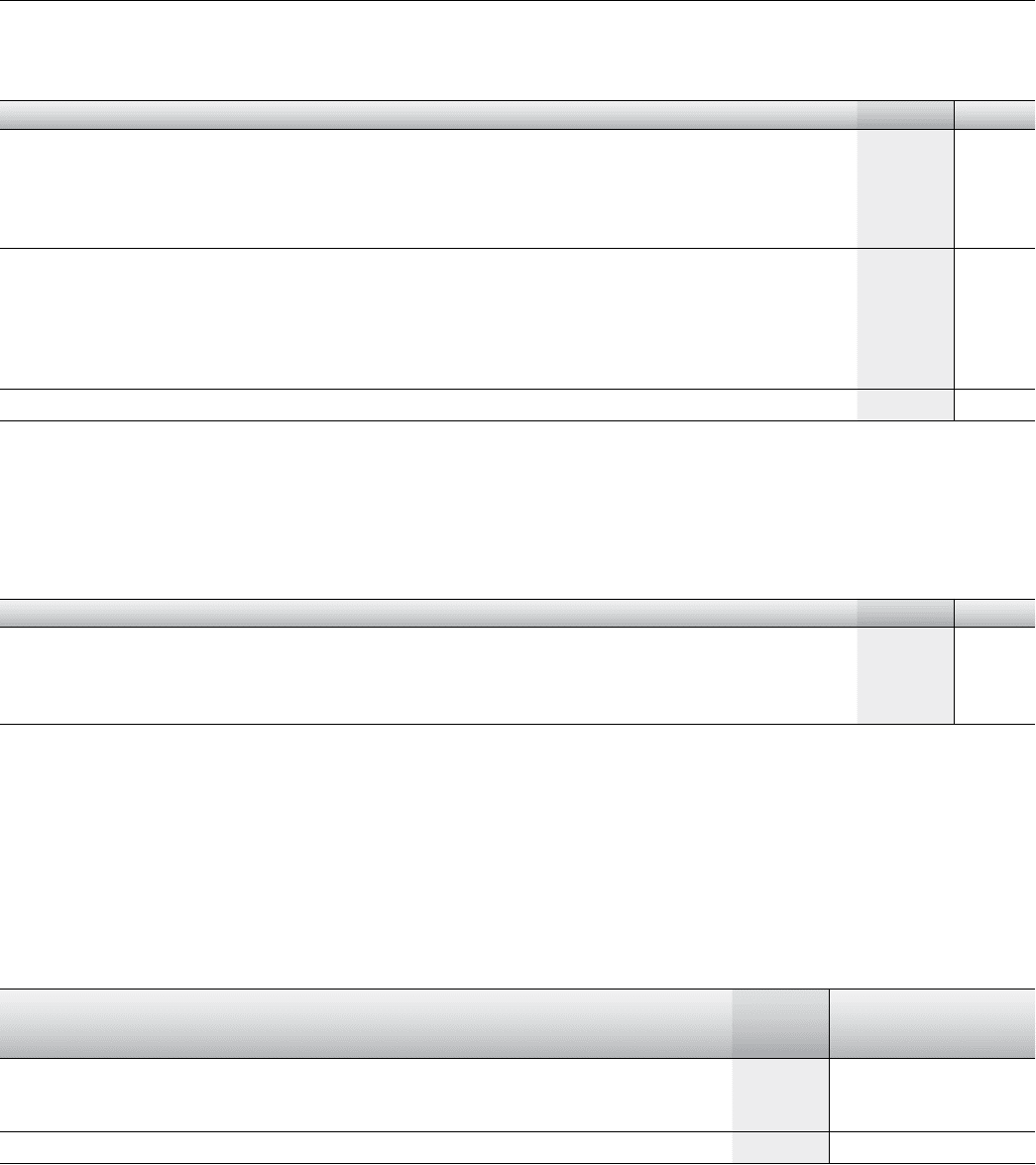

2006 2005

Weighted average discount rate for accrued benefit obligations 5.25% 5.25%

Weighted average discount rate for pension expense 5.25% 6.25%

Weighted average rate of compensation increase for pension expense and accrued benefit obligation 3.50% 4.00%

Weighted average expected long-term rate of return on plan assets 6.75% 7.25%

Expected return on assets represents management’s best estimate

of the long-term rate of return on plan assets applied to the fair

value of the plan assets. The Company establishes its estimate of the

expected rate of return on plan assets based on the fund’s target

asset allocation and estimated rate of return for each asset class.

Estimated rates of return are based on expected returns from fixed

income securities which take into account bond yields. An equity

risk premium is then applied to estimate equity returns. Differences

between expected and actual return are included in actuarial gains

and losses.

The estimated average remaining service periods for the plans range

from 9 to 13 years. The Company did not have any curtailment gains

or losses in 2006 or 2005.

Plan assets are comprised primarily of pooled funds that invest in

common stocks and bonds. The pooled Canadian equity fund has

investments in the Company’s equity securities comprising approxi-

mately 1% of the pooled fund. This results in approximately $1 million

(2005 – $1 million) of the plans’ assets being indirectly invested in the

Company’s equity securities.

The Company makes contributions to the plans to secure the benefits

of plan members and invests in permitted investments using the target

ranges established by the Pension Committee of the Company. The

Pension Committee reviews actuarial assumptions on an annual basis.

(B) ALLOCATION OF PL AN ASSETS:

Percentage of Percentage of

plan assets, plan assets, Target asset

December 31, December 31, allocation

Asset category 2006 2005 percentage

Equity securities 59.7% 59.5% 50% to 65%

Debt securities 40.0% 39.9% 35% to 50%

Other (cash) 0.3% 0.6% 0% to 1%

100.0% 100.0%