Rogers 2003 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2003 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

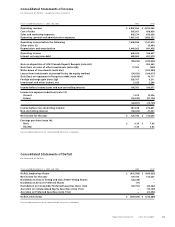

2003 Annual Report Rogers Communications Inc.

76

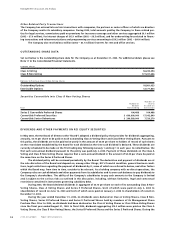

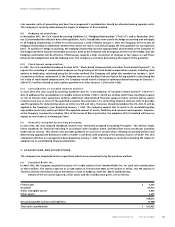

Notes to Consolidated Financial Statements

impaired. An impairment loss is measured as the amount by which the carrying amount of the group of assets exceeds its

fair value. At December 31, 2003, no such impairment had occurred.

For the year ended December 31, 2002, the Company’s policy was to review the recoverability of PP&E annually or

more frequently if events or circumstances indicated that the carrying amount may not be recoverable. Recoverability

was measured by comparing the carrying amounts of a group of assets to future undiscounted net cash flows expected to

be generated by that group of assets. As at December 31, 2002, no such impairment had occurred. Intangible assets with

definite lives were tested for impairment by comparing their book values with the undiscounted cash flows expected to

be received from their use. At December 31, 2002, no impairment had occurred.

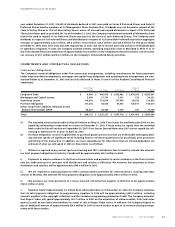

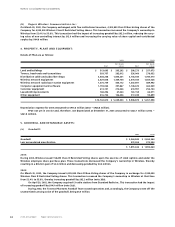

(f) Goodwill and intangible assets:

(i) Goodwill:

Goodwill is the residual amount that results when the purchase price of an acquired business exceeds the sum of the

amounts allocated to the tangible and intangible assets acquired, less liabilities assumed, based on their fair values.

When the Company enters into a business combination, the purchase method of accounting is used. Goodwill is assigned

as of the date of the business combination to reporting units that are expected to benefit from the business combination.

Goodwill is not amortized but instead is tested for impairment annually or more frequently if events or changes in

circumstances indicate that the asset might be impaired. The impairment test is carried out in two steps. In the first step,

the carrying amount of the reporting unit, including goodwill, is compared with its fair value. When the fair value of the

reporting unit exceeds its carrying amount, goodwill of the reporting unit is not considered to be impaired and the sec-

ond step of the impairment test is unnecessary. The second step is carried out when the carrying amount of a reporting

unit exceeds its fair value, in which case, the implied fair value of the reporting unit’s goodwill, determined in the same

manner as the value of goodwill is determined in a business combination, is compared with its carrying amount to mea-

sure the amount of the impairment loss, if any.

(ii) Intangible assets:

Intangible assets acquired in a business combination are recorded at their fair values and all intangible assets are tested

for impairment annually or more frequently when events or changes in circumstances indicate that their carrying

amounts may not be recoverable. Intangible assets with determinable lives are amortized over their estimated useful

lives and are tested for impairment as described in note 2(e). Intangible assets having an indefinite life, such as spectrum

licences, are not being amortized but instead are tested for impairment on an annual or more frequent basis by compar-

ing their fair values with book value. An impairment loss on indefinite life intangible assets is recognized when the

carrying amount of the asset exceeds its fair value.

The Company has tested goodwill and intangible assets with indefinite lives for impairment at December 31, 2003 and

2002 and determined no impairment in the carrying value of these assets existed.

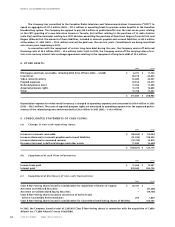

(g) Foreign currency translation:

Long-term debt denominated in U.S. dollars is translated into Canadian dollars at the period-end rate of exchange. The

effect of cross-currency interest rate exchange agreements is shown separately in note 10. Exchange gains or losses on

translating long-term debt are recognized in the consolidated statements of income. In 2003, foreign exchange gains

related to the translation of long-term debt totalled $290.7 million (2002 – $3.5 million).

(h) Deferred charges:

The costs of obtaining bank and other debt financing are deferred and amortized on a straight-line basis over the effec-

tive life of the debt to which they relate.

During the development and pre-operating phases of new products and businesses, related incremental costs are

deferred and amortized on a straight-line basis over periods of up to five years.

(i) Inventories:

Inventories are valued at the lower of cost, on a first-in, first-out basis, and net realizable value. Video rental inventory,

which includes videocassettes, DVDs and video games, is depreciated to a pre-determined residual value. The residual

value of the video rental inventory is recorded as a charge to operating expense upon the sale of the video rental inven-

tory. Depreciation of video rental inventory is charged to operating expense on a diminishing-balance basis over a

six-month period.

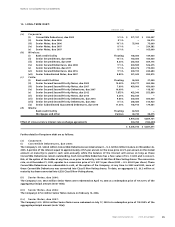

(j) Pension benefits:

The Company accrues its pension plan obligations as employees render the services necessary to earn the pension. The

Company uses the current settlement discount rate to measure the accrued pension benefit obligation and uses the corri-

dor method to amortize actuarial gains or losses (such as changes in actuarial assumptions and experience gains or losses)

over the average remaining service life of the employees. Under the corridor method, amortization is recorded only if the

accumulated net actuarial gains or losses exceed 10% of the greater of accrued pension benefit obligation and the value

of the plan assets.