Rogers 2003 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2003 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112

|

|

2003 Annual Report Rogers Communications Inc.

104

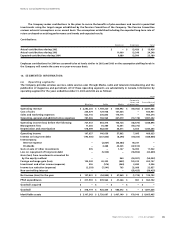

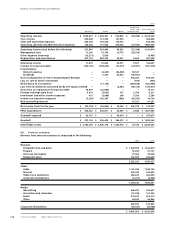

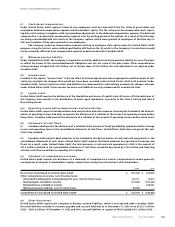

Notes to Consolidated Financial Statements

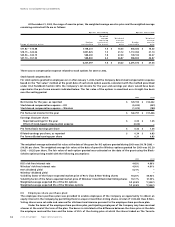

(b) Gain on sale of cable systems:

Under Canadian GAAP, the cash proceeds on the non-monetary exchange of the cable assets in 2000 were recorded as a

reduction in the carrying value of PP&E. Under United States GAAP, a portion of the cash proceeds received must be rec-

ognized as a gain in the consolidated statements of income on an after-tax basis. The gain amounted to $40.3 million

before income taxes.

Under Canadian GAAP, the after-tax gain arising on the sale of certain of the Company’s cable television systems

in prior years was recorded as a reduction of the carrying value of goodwill acquired in a contemporaneous acquisition of

certain cable television systems. Under United States GAAP, the Company included the gain on sale of the cable television

systems in income, net of related future income taxes.

As a result of these transactions, amortization expense under United States GAAP was increased in subsequent years.

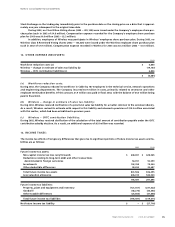

(c) Pre-operating costs:

Under Canadian GAAP, the Company defers the incremental costs relating to the development and pre-operating phases

of new businesses and amortizes these costs on a straight-line basis over periods up to five years. Under United States

GAAP, these costs are expensed as incurred.

(d) Equity instruments:

Under Canadian GAAP, the Convertible Preferred Securities are classified as shareholders’ equity and the related interest

expense is recorded as a distribution from retained earnings. Under United States GAAP, these securities are classified as

long-term debt and the related interest expense is recorded in the consolidated statements of income.

Under Canadian GAAP, the Preferred Securities were classified as shareholders’ equity and until September 2002, the

related interest expense was recorded as a distribution from retained earnings. Under U.S. GAAP, the Preferred Securities

were classified as long-term debt and the related interest expense was recorded in the consolidated statements of income.

Under Canadian GAAP, the proceeds from the Collateralized Equity Securities were classified as shareholders’ equity.

Under United States GAAP, these securities were recorded as long-term debt and recorded at their fair value at December 31,

2001. Adjustments to the fair value at each reporting date are recorded in the consolidated statements of income.

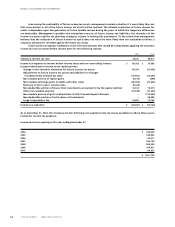

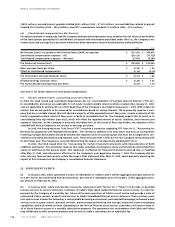

(e) Interest capitalization:

United States GAAP requires capitalization of interest costs as part of the historical cost of acquiring certain qualifying

assets that require a period of time to prepare for their intended use. This is not required under Canadian GAAP.

(f) Unrealized holding gains and losses on investments:

United States GAAP requires that certain investments in equity securities that have readily determinable fair values be

stated in the consolidated balance sheets at their fair values. The unrealized holding gains and losses from these invest-

ments, which are considered to be “available-for-sale securities” under United States GAAP, are included as a separate

component of shareholders’ equity and comprehensive income, net of related future income taxes.

As at December 31, 2003 and 2002, this amount represents the Company’s accumulated other comprehensive income.

(g) Acquisition of Cable Atlantic:

United States GAAP requires that shares issued in connection with a purchase business combination be valued based on

the market price at the announcement date of the acquisition, whereas Canadian GAAP had required such shares be val-

ued based on the market price at the consummation date of the acquisition. Accordingly, the Class B Non-Voting shares

issued in respect of the acquisition of Cable Atlantic in 2001 were recorded at $35.4 million more under United States

GAAP than under Canadian GAAP. This resulted in an increase to goodwill in this amount, with a corresponding increase

to contributed surplus in the amount of $35.4 million.

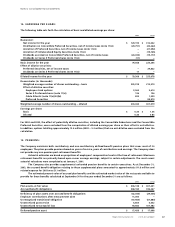

(h) Financial instruments:

Under Canadian GAAP, the Company accounts for its cross-currency interest rate exchange agreements and interest

exchange agreements as hedges of specific debt instruments. Under United States GAAP, these instruments are not

accounted for as hedges as a result of adopting the new pronouncement entitled “Accounting for Derivative Instruments

and Hedging Activities (“SFAS 133”), effective January 1, 2001. As a result, the Company has recorded the net excess of the

fair values of the cross-currency interest rate exchange agreements and interest rate exchange agreements over the car-

rying values of these instruments as at December 31, 2000, being $18.4 million, as a cumulative transition adjustment to

net income under United States GAAP. The Company has also recorded a cumulative transition adjustment to write off

the net balance of the deferred foreign exchange as at December 31, 2000, being $20.7 million, that arose upon redesig-

nation of certain of the Company’s cross-currency interest rate exchange agreements. Further, the Company has recorded

$29.7 million as a cumulative transition adjustment to net income, which represents the excess of the fair value of the

long-term debt to which the derivative instruments relate (the “hedged debt”) over its carrying value. Therefore, the net

cumulative transition adjustment under SFAS 133 to the loss for the year ended December 31, 2001 under United States

GAAP was a charge to the net loss of $32.1 million. The adjustment to long-term debt is being amortized to net income

under United States GAAP over the remaining effective life of the related long-term debt.

Therefore, for the years ended December 31, 2003 and 2002, under United States GAAP, the Company has recorded

the change in the fair values of the cross-currency interest rate exchange agreements since January 1, 2001 and the amor-

tization of the adjustment to its long-term debt, as discussed above.