Rogers 2003 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2003 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

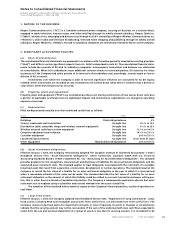

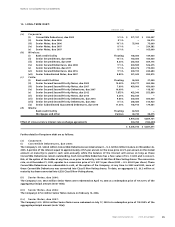

2003 Annual ReportRogers Communications Inc. 75

Notes to Consolidated Financial Statements

(Tabular amounts in thousands of dollars, except per share amounts)

Years ended December 31, 2003 and 2002

1. NATURE OF THE BUSINESS:

Rogers Communications Inc. (“RCI”) is a Canadian communications company, carrying on business on a national basis,

engaged in cable television, Internet access and video retailing through its wholly owned subsidiary, Rogers Cable Inc.

(“Cable”), wireless voice, messaging and data services through its 55.8% ownership of Rogers Wireless Communications Inc.

(“Wireless”), and in radio and television broadcasting, televised home shopping and publishing through its wholly owned

subsidiary, Rogers Media Inc. (“Media”). RCI and its subsidiary companies are collectively referred to herein as the Company.

2. SIGNIFICANT ACCOUNTING POLICIES:

(a) Basis of presentation:

The consolidated financial statements are prepared in accordance with Canadian generally accepted accounting principles

(“GAAP”) and differ in certain significant respects from U.S. GAAP as described in note 22. The consolidated financial state-

ments include the accounts of RCI and its subsidiary companies. Intercompany transactions and balances are eliminated

on consolidation. When RCI’s subsidiaries issue additional common shares to unrelated parties, RCI accounts for these

issuances as if the Company had sold a portion of its interest in that subsidiary and, accordingly, records a gain or loss on

dilution of RCI’s interest.

Investments over which the Company is able to exercise significant influence are accounted for by the equity

method. Other investments are recorded at cost. Investments are written down when there is evidence that a decline in

value that is other than temporary has occurred.

(b) Property, plant and equipment:

Property, plant and equipment (“PP&E”) are recorded at purchase cost. During construction of new assets, direct costs plus

a portion of applicable overhead costs are capitalized. Repairs and maintenance expenditures are charged to operating

expense as incurred.

(c) Depreciation:

PP&E are depreciated annually over their estimated useful lives as follows:

Asset Basis Rate

Buildings Diminishing balance 5%

Towers, head-ends and transmitters Straight line 62/3% to 10%

Distribution cable, subscriber drops and wireless network equipment Straight line 62/3% to 25%

Wireless network radio base station equipment Straight line 121/2% to 141/3%

Computer equipment and software Straight line 141/3% to 331/3%

Customer equipment Straight line 20% to 331/3%

Leasehold improvements Straight line Over term of lease

Other equipment Mainly diminishing balance 20% to 331/3%

(d) Asset retirement obligations:

Effective January 1, 2003, the Company retroactively adopted The Canadian Institute of Chartered Accountants’ (“CICA”)

Handbook Section 3110, “Asset Retirement Obligations”, which harmonizes Canadian GAAP with U.S. Financial

Accounting Standards Board’s (“FASB”) Statement No. 143, “Accounting for Asset Retirement Obligations”. The standard

provides guidance for the recognition, measurement and disclosure of liabilities for asset retirement obligations and the

associated asset retirement costs. The standard applies to legal obligations associated with the retirement of a tangible

long-lived asset that result from acquisition, construction, development or normal operations. The standard requires the

Company to record the fair value of a liability for an asset retirement obligation in the year in which it is incurred and

when a reasonable estimate of fair value can be made. The standard describes the fair value of a liability for an asset

retirement obligation as the amount at which that liability could be settled in a current transaction between willing par-

ties, that is, other than in a forced or liquidation transaction. The Company is subsequently required to allocate that asset

retirement cost to expense using a systematic and rational method over the asset’s useful life.

The adoption of this standard had no material impact on the Company’s financial position, results of operations or

cash flows.

(e) Long-lived assets:

Effective January 1, 2003, the Company adopted CICA Handbook Section 3063, “Impairment of Long-Lived Assets”. Long-

lived assets, including PP&E and intangible assets with finite useful lives, are amortized over their useful lives. The

Company reviews long-lived assets for impairment annually or more frequently if events or changes in circumstances

indicate that the carrying amount may not be recoverable. If the sum of the undiscounted future cash flows expected to

result from the use and eventual disposition of a group of assets is less than its carrying amount, it is considered to be