Reebok 2007 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2007 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

091

ANNUAL REPORT 2007 --- adidas Group

03

T

REASUR

Y

GROUP FINANCING POLICY The major goal of our fi nancing

policy is to minimize the Group’s fi nancial expenses while

ensuring suffi cient liquidity reserves at all times to meet the

Group’s payment commitments. The operating activities of our

Group segments and the resulting cash infl ows represent the

Group’s main source of liquidity. Liquidity is planned on a

multi-year fi nancial and liquidity plan on a rolling monthly

basis. This comprises all consolidated Group companies. Our

in-house bank concept takes advantage of the surplus funds

of individual Group companies to cover the fi nancial require-

ments of others, reducing external fi nancing requirements

and optimizing our net interest expenses. By settling inter-

company transactions via inter-company fi nancial accounts,

we are able to reduce external bank account transactions and

thus bank charges. Currency management as well as ongoing

interest rate optimization are additional goals of our Group

Treasury department.

TREASURY SYSTEM AND RESPONSIBILITIES Our Group’s

Treasury Policy governs all treasury-related issues, including

banking policy and approval of bank relationships, global

fi nancing arrangements and liquidity / asset management,

currency and interest risk management as well as the man-

agement of inter-company cash fl ows. Responsibilities are

arranged in a three-tiered approach:

- The Treasury Committee consists of members of the

Executive Board and other senior executives who decide

on the Group’s Treasury Policy and provide strategic guidance

for managing treasury-related topics. The Treasury Committee

approves all major changes to our Treasury Policy.

- The Group Treasury department is responsible for specifi c

centralized treasury transactions and for global implemen-

tation of our Group’s Treasury Policy.

- On a subsidiary level, local managing directors and fi nancial

controllers are responsible for managing treasury matters in

the respective subsidiaries. Brand and regional controlling

ensures that the transactions of the individual business units

are in compliance with the Group’s Treasury Policy.

CENTRALIZED TREASURY FUNCTION In accordance with our

Group’s Treasury Policy, more than 90 % of our worldwide

credit lines are managed by the Group Treasury department.

Portions of those lines are allocated to the Group’s subsid-

iaries and backed by parental guarantees. As a result of this

centralized liquidity management, the Group is well positioned

to allocate resources effi ciently throughout the organization.

The Group’s debt is generally unsecured and includes standard

fi nancial covenants, which are reviewed on a quarterly basis.

We maintain good relations with numerous partner banks,

thereby avoiding a strong dependency on any single institution.

Banking partners of the Group and our subsidiaries are

required to have at least a BBB+ long-term investment grade

rating by Standard & Poor’s or an equivalent rating by another

leading rating agency. Only in exceptional cases are Group com-

panies and subsidiaries authorized to work with banks with a

lower rating. see Risk and Opportunity Report, p. 104 To optimize the

Group’s cash position and ensure optimal allocation of liquid

fi nancial resources, subsidiaries are required to transfer

excess cash to the Group’s headquarters.

LONG-TERM FINANCIAL FLEXIBILITY ENSURED The adidas

Group’s long-term fl exibility is ensured by unutilized fi nancial

instruments in an amount of € 4.1 billion at the end of 2007

(2006: € 4.4 billion). These instruments include a € 2.0 billion

multi-year syndicated loan (2006: € 2.0 billion) as well as bilateral

credit lines at different banks in an amount of € 2.1 billion

(2006: € 2.4 billion). The reduction of unutilized credit lines

in 2007 refl ects the decreased need for fi nancial fl exibility

as a result of the Group’s strong progress in gross borrowings

reduction in 2007. We monitor the ongoing need for available

credit lines based on the current level of debt as well as future

fi nancing requirements.

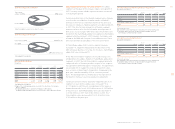

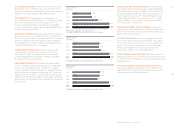

2007 2006

To

t

al

6,

2

6

2

6,935

591

2,

879

985

2,

480

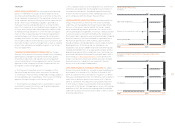

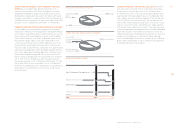

REMAINING TIME TO MATURITY OF AVAILABLE FACILITIES

€

in milli

o

n

s

3 to 5

y

ears

2

,

3

7

6

1 to 3 years 967

> 5 years 419

< 1 year

2,

500

200

7 2006

T

ota

l

6,

2

6

2

6,935

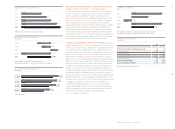

TOTAL CREDIT FACILITIES

€

in millions

P

rivate placements

1

,

564

Medium-term committed credit lines 2,000

Convertible bond 384

S

h

o

rt-t

e

rm

c

r

ed

it lin

es

2

,31

4

375

2

,77

6

2,000

1,7

84