Reebok 2007 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2007 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

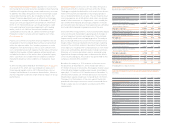

111

ANNUAL REPORT 2007 --- adidas Group

03

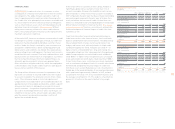

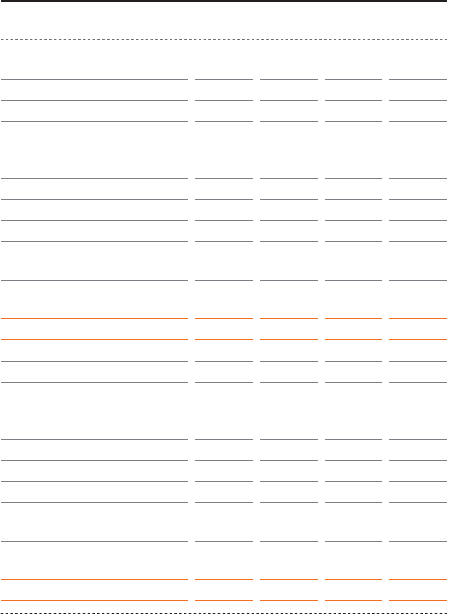

FUTURE CASH OUTFLOWS

€

in millions

Up to Between 1 Between 3 After

1 year and 3 years and 5 years 5 years

T

ota

l

As at December 31, 2007

Bank borrowings

incl. commercial

paper

Private placements

Convertible bond

Accounts payable

Other fi nancial

liabilities

Derivative fi nancial

liabilities

T

ota

l

As at December 31, 2006

Bank borrowings

incl. commercial

paper

Private placements

Convertible bond

Accounts payable

Other fi nancial

liabilities

Derivative fi nancial

liabilities

T

ota

l

0 — 198 — 1

98

8

186 583 376 419

1,564

4

— 384 — — 38

4

4

849 — — —

8

4

9

16 1 1 2

20

88 62 8 2 1

60

1,139 1,030 583 423 3,175

3

3

0

144 — 275 — 41

9

9

109 610 474 591

1

,7

84

4

— — 375 —

3

7

5

5

752 — — — 7

52

2

18 2 2 3

25

5

37 29 12 5 8

3

3

1,060 641 1,138 599 3,438

8

9

0

8

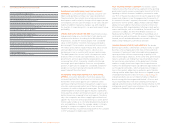

F

INANCIAL RISK

S

CREDIT RISKS A credit risk arises if a customer or other

counter party to a fi nancial instrument fails to meet its contrac-

tual obligations. The adidas Group is exposed to credit risk

from its operating activities and from certain fi nancing activi-

ties. Credit risks arise principally from accounts receivable and

to a lesser extent from other contractual fi nancial obligations

such as other fi nancial assets, short-term bank deposits and

derivative fi nancial instruments. see Note 23, p. 180 Without

taking into account any collateral or other credit enhance-

ments, the carrying amount of fi nancial assets represents the

maximum exposure to credit risk.

At the end of 2007, there was no relevant concentration of credit

risk by type of customer or geography. Instead, our credit risk

exposure is mainly infl uenced by individual customer charac-

teristics. Under the Group’s credit policy, new customers are

analyzed for creditworthiness before standard payment and

delivery terms and conditions are offered. This review utilizes

external ratings from credit agencies. Purchase limits are also

established for each customer. Then both creditworthiness and

purchase limits are monitored on an ongoing basis. Customers

that fail to meet the Group’s minimum creditworthiness are

allowed to purchase products only on a pre-payment basis.

Other activities to mitigate credit risks, which are employed on

a selective basis only, include credit insurances, bank guaran-

tees as well as retention of title clauses.

The Group utilizes allowance accounts for impairments that

represent our estimate of incurred credit losses with respect

to accounts receivable. The allowance consists of two compo-

nents: (1) an allowance based on historical experience of

unexpected losses established for all receivables based on the

ageing structure of receivables past due date, and (2) a specifi c

allowance that relates to individually assessed risk for each

specifi c customer – irrespective of ageing. Allowance accounts

are used to record impairment losses unless our Group is sat-

isfi ed that no recovery of the amount owed is possible; at that

point the amount considered irrecoverable is written off

against the receivable directly.

At the end of 2007, no customer at either adidas, Reebok or

TaylorMade-adidas Golf accounted for more than 10 % of

accounts receivable. Allowance for doubtful accounts receiv-

able remained at a similar level of total accounts receivable in

2007 compared to the prior year. Our Days of Sales Outstanding

were unchanged compared to the prior year at 58 days. As a

result, we believe that our overall credit risk level from cus-

tomers has remained nearly unchanged despite an increasingly

diffi cult retail environment in many key markets. see Economic

and Sector Development, p. 078 Therefore, we continue to estimate the

likelihood and potential fi nancial impact of credit risks from

customers as low.

Credit risks from other fi nancial contractual relationships in-

clude items such as other fi nancial assets, short-term bank

deposits and derivative fi nancial instruments. The adidas Group

Treasury department arranges currency and interest rate

hedges, and invests cash, with major banks of a high credit

standing throughout the world. All banks are rated “A–” or

higher in terms of Standard & Poor’s long-term ratings (or a

comparable rating from other rating agencies). Foreign-based

adidas Group companies are authorized to work with banks

rated “BBB +” or higher. Only in exceptional cases are subsid-

iaries authorized to work with banks rated lower than “BBB +”.

To limit risk in these cases, restrictions are clearly stipulated

such as maximum cash deposit levels. As a result, we estimate

the likelihood and potential fi nancial impact of credit risks

from these assets as low. We believe our risk concentration is

limited due to the broad distribution of our investment business

with a syndicate of approximately 30 banks. In 2007, no bank

accounted for more than 17 % of our investment business and

the average concentration is 1 %. This leads to a maximum ex-

posure of € 63 million in the event of default of any single

bank.