Reebok 2007 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2007 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

106

ANNUAL REPORT 2007 --- adidas Group GROUP MANAGEMENT REPORT – OUR FINANCIAL YEAR - Risk and Opportunity Report

E

XTERNAL AND INDUSTRY RISK

S

MACROECONOMIC RISKS Growth of the sporting goods indus-

try is infl uenced by consumer confi dence and consumer

spending. Abrupt economic downturns, in particular in regions

where the Group is highly represented, therefore pose a signif-

icant short-term risk to sales development. To mitigate this

risk, the Group strives to balance sales across key global

regions and also between developed and emerging markets.

In addition, a core element of our performance positioning is

the utilization of an extensive global event and partnership

portfolio where demand is more predictable and less sensitive

to macroeconomic infl uence.

In 2008, the Group expects global and, in particular, North

American economic growth to slow. see Outlook, p. 118 Similarly,

the risk of macroeconomic shocks has increased versus 2007.

However, economic expansion in emerging markets, including

China, Russia and India, is expected to continue. These mar-

kets have overtaken North America and the European Union

as the largest contributors to Group revenue growth. Never-

theless, we now assess the likelihood that adverse macro-

economic events could impact our business as medium. The

materialization of such events could have a medium negative

fi nancial impact on our Group.

CONSUMER DEMAND RISKS Failure to anticipate and respond

to changes in consumer demand is one of the most serious

threats to our industry. Consumer demand changes can be

sudden and unexpected. Because industry product procure-

ment cycles average 12 to 18 months, the Group faces a risk of

short-term revenue loss in cases where it is unable to respond

quickly to such changes. Even more critical, however, is the

risk of continuously overlooking a new consumer trend or

failing to acknowledge its potential magnitude over a sustained

period of time.

To mitigate this risk, continually identifying and responding to

consumer demand shifts as early as possible is a key respon-

sibility of our brands. In this respect, we utilize extensive

primary and secondary research tools as outlined in our risk

and opportunity identifi cation process.

As a leader in our industry, our core brand strategies continue

to be focused on infl uencing rather than reacting to the chang-

ing consumer environment. We invest signifi cant resources

in research and development to innovate and bring fresh new

technologies and designs to market.

see Research and Development,

p. 072 In addition, we also seek to create consumer demand for

our brands and brand initiatives through extensive marketing,

product and brand communication programs. And, we con-

tinue to focus on supply chain improvements to speed up

concept-to-shelf timelines. see Global Operations, p. 062 In 2007,

we implemented new consumer segmentation strategies at

both brand adidas and Reebok and combined Group resources

for market research and competitor research. In addition, we

increased and focused our marketing working budget spend

at Reebok, in line with the future positioning of the brand. We

plan further initiatives in this respect in 2008.

Given the broad spectrum of our Group’s product offering,

retailer feedback, visibility provided through our order back-

logs and other early indicators, see Internal Group Management System,

p. 056 we view the overall risk from consumer demand shifts

as unchanged versus the prior year. Changes in consumer

demand continue to have a medium likelihood of occurrence

and could have a potential medium impact on our Group.

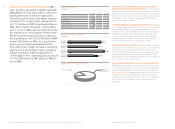

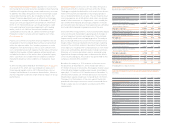

CORPORATE RISKS OVERVIEW

Probability Potential

of fi nancial

occurrence impact

External and Industry Risk

s

Macroeconomic risks medium medium

Consumer demand risks medium medium

Industry consolidation risks medium medium

Political and regulatory risks low medium

Legal risks low medium

Risks from product counterfeiting high low

Social and environmental risks low low

Natural risks low low

S

trate

g

ic and

O

perational Risks

Portfolio integration risks low high

Risks from loss of brand image medium medium

Own-retail risks medium medium

Risks from rising input costs medium medium

Supplier default risks low low

Product quality risks low low

Customer risks medium low

Risk from loss of key partnerships medium low

Product design and development risks low high

Personnel risks low medium

Risks from non-compliance low medium

IT risks low high

Fin

a

n

c

i

a

l Ri

s

k

s

Credit risks low low

Financing and liquidity risks low high

Currency risks low low

Interest rate risks low low