PG&E 2010 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2010 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

The Utility treats the amount of its outstanding

commercial paper as a reduction to the amount available

under its revolving credit facilities so that liquidity from

the revolving credit facility is available to repay outstanding

commercial paper.

The revolving credit facilities include usual and

customary covenants for credit facilities of this type,

including covenants limiting liens to those permitted under

the senior note indenture, mergers, sales of all or

substantially all of the Utility’s assets, and other

fundamental changes. Both the $750 million and $1.9

billion revolving credit facilities require that the Utility

maintain a ratio of total consolidated debt to total

consolidated capitalization of, at most, 65% as of the end

of each fiscal quarter. At December 31, 2010, the Utility

met this ratio test.

Commercial PaperProgram

The Utility has a $1.75 billion commercial paper program,

the borrowings from which are used primarily to cover

fluctuations in cash flow requirements. Liquidity support

for these borrowings is provided by available capacity

under the Utility’s revolving credit facilities, as described

above. The commercial paper may have maturities up to

365 days and ranks equally with the Utility’s other

unsubordinated and unsecured indebtedness. Commercial

paper notes are sold at an interest rate dictated by the

market at the time of issuance. At December 31, 2010, the

average yield was 0.51%.

OtherShort-termBorrowings

On October 12, 2010, the Utility issued $250 million

principal amount of Floating Rate Senior Notes due

October 11, 2011. The interest rate for the Floating Rate

Senior Notes is equal to the three-month LIBOR plus

0.58% and will reset quarterly beginning on January 11,

2011. At December 31, 2010, the interest rate on the

Floating Rate Senior Notes was 0.87%. On January 11,

2011, the interest rate was reset to 0.88%.

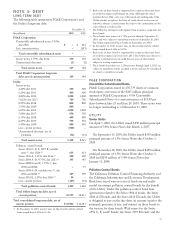

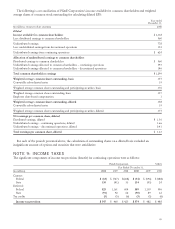

NOTE 5: ENERGY RECOVERY

BONDS

In 2005, PERF issued two separate series of ERBs in the

aggregate amount of $2.7 billion to refinance a regulatory

asset that the Utility recorded in connection with the

Chapter 11 Settlement Agreement. The proceeds of the

ERBs were used by PERF to purchase from the Utility the

right, known as “recovery property,” to be paid a specified

amount from a dedicated rate component (“DRC”) to be

collected from the Utility’s electricity customers. DRC

charges are authorized by the CPUC under state legislation

and will be paid by the Utility’s electricity customers until

the ERBs are fully retired. Under the terms of a recovery

property servicing agreement, DRC charges are collected

by the Utility and remitted to PERF for payment of

principal, interest, and miscellaneous expenses associated

with the bonds.

The first series of ERBs issued on February 10, 2005

included five classes aggregating to a $1.9 billion principal

amount, with scheduled maturities ranging from

September 25, 2006 to December 25, 2012. Interest rates

on the remaining two outstanding classes are 4.37% for the

earlier maturing class and 4.47% for the later maturing

class. The proceeds of the first series of ERBs were paid by

PERF to the Utility and were used by the Utility to

refinance the remaining unamortized after-tax balance of

the settlement regulatory asset. The second series of ERBs,

issued on November 9, 2005, included three classes

aggregating to an $844 million principal amount, with

scheduled maturities ranging from June 25, 2009 to

December 25, 2012. Interest rates on the remaining two

classes are 5.03% for the earlier maturing class and 5.12%

for the later maturing class. The proceeds of the second

series of ERBs were paid by PERF to the Utility to pre-fund

the Utility’s tax liability that will be due as the Utility

collects the DRC charges from customers.

The total amount of ERB principal outstanding was

$827 million at December 31, 2010 and $1.2 billion at

December 31, 2009. The scheduled principal repayments

for ERBs are reflected in the table below:

(in millions) 2011 2012 Total

Utility

Average fixed interest rate 4.59% 4.66% 4.63%

Energy recovery bonds $ 404 $ 423 $ 827

While PERF is a wholly owned consolidated subsidiary

of the Utility, it is legally separate from the Utility. The

assets (including the recovery property) of PERF are not

available to creditors of the Utility or PG&E Corporation,

and the recovery property is not legally an asset of the

Utility or PG&E Corporation.

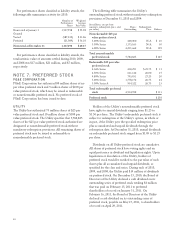

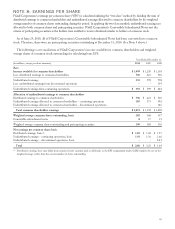

NOTE 6: COMMON STOCK AND

SHARE-BASED COMPENSATION

PG&E CORPORATION

Of the 395,227,205 shares of PG&E Corporation common

stock outstanding at December 31, 2010, 475,880 shares

were granted as restricted stock under the PG&E

Corporation Long-Term Incentive Program and the 2006

78