PG&E 2010 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2010 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

NOTE 13: RESOLUTION OF

REMAINING CHAPTER 11

DISPUTED CLAIMS

Various electricity suppliers filed claims in the Utility’s

proceeding under Chapter 11 seeking payment for energy

supplied to the Utility’s customers through the wholesale

electricity markets operated by the CAISO and the

California Power Exchange (“PX”) between May 2000 and

June 2001. These claims, which the Utility disputes, are

being addressed in various FERC and judicial proceedings

in which the State of California, the Utility, and other

electricity purchasers are seeking refunds from electricity

suppliers, including municipal and governmental entities,

for overcharges incurred in the CAISO and the PX

wholesale electricity markets between May 2000 and June

2001. At December 31, 2010 and December 31, 2009, the

Utility held $512 million and $515 million in escrow,

respectively, including interest earned, for payment of the

remaining net disputed claims. These amounts are included

within restricted cash on the Consolidated Balance Sheets.

While the FERC and judicial proceedings have been

pending, the Utility entered into a number of settlements

with various electricity suppliers to resolve some of these

disputed claims and to resolve the Utility’s refund claims

against these electricity suppliers. These settlement

agreements provide that the amounts payable by the parties

are, in some instances, subject to adjustment based on the

outcome of the various refund offset and interest issues

being considered by the FERC. The proceeds from these

settlements, after deductions for contingencies based on

the outcome of the various refund offset and interest issues

being considered by the FERC, will continue to be

refunded to customers in rates. Additional settlement

discussions with other electricity suppliers are ongoing.

Any net refunds, claim offsets, or other credits that the

Utility receives from energy suppliers through resolution of

the remaining disputed claims, either through settlement or

the conclusion of the various FERC and judicial

proceedings, will also be refunded to customers.

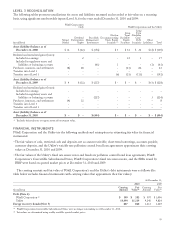

The following table presents the changes in the

remaining net disputed claims liability and interest accrued

from December 31, 2009 to December 31, 2010:

(in millions)

Balance at December 31, 2009 $ 946

Interest accrued 30

Less: supplier settlements (42)

Balance at December 31, 2010 $ 934

At December 31, 2010, the Utility’s net disputed claims

liability was $934 million, consisting of $745 million of

remaining disputed claims (classified on the Consolidated

Balance Sheets within accounts payable – disputed claims

and customer refunds) and interest accrued at the FERC-

ordered rate of $683 million (classified on the

Consolidated Balance Sheets within interest payable),

partially offset by accounts receivable from the CAISO and

the PX of $494 million (classified on the Consolidated

Balance Sheets within accounts receivable – other).

Interest accrues on the net liability for disputed claims at

the FERC-ordered rate, which is higher than the rate

earned by the Utility on the escrow balance. Although the

Utility has been collecting the difference between the

accrued interest and the earned interest from customers,

this amount is not held in escrow. If the amount of interest

accrued at the FERC-ordered rate is greater than the

amount of interest ultimately determined to be owed with

respect to disputed claims, the Utility would refund to

customers any excess net interest collected from customers.

The amount of any interest that the Utility may be

required to pay will depend on the final amounts to be

paid by the Utility with respect to the disputed claims and

when such interest is paid.

PG&E Corporation and the Utility are unable to predict

when the FERC or judicial proceedings that are still pending

will be resolved, and the amount of any potential refunds that

the Utility may receive or the amount of disputed claims,

including interest that the Utility will be required to pay.

NOTE 14: RELATED PARTY

AGREEMENTS AND

TRANSACTIONS

The Utility and other subsidiaries provide and receive

various services to and from their parent, PG&E

Corporation, and among themselves. The Utility and PG&E

Corporation exchange administrative and professional

services in support of operations. Services provided directly

to PG&E Corporation by the Utility are priced at the higher

of fully loaded cost (i.e., direct cost of good or service and

allocation of overhead costs) or fair market value, depending

on the nature of the services. Services provided directly to

the Utility by PG&E Corporation are generally priced at the

lower of fully loaded cost or fair market value, depending on

the nature and value of the services. PG&E Corporation also

allocates various corporate administrative and general costs

to the Utility and other subsidiaries using agreed-upon

allocation factors, including the number of employees,

operating and maintenance expenses, total assets, and other

cost allocation methodologies. Management believes that

the methods used to allocate expenses are reasonable and

meet the reporting and accounting requirements of its

regulatory agencies.

105