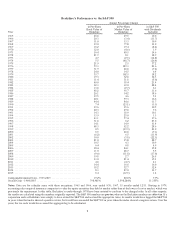

Berkshire Hathaway 2015 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2015 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

If our revolving float is both costless and long-enduring, which I believe it will be, the true value of this

liability is dramatically less than the accounting liability. Owing $1 that in effect will never leave the premises –

because new business is almost certain to deliver a substitute – is worlds different from owing $1 that will go out the

door tomorrow and not be replaced. The two types of liabilities, however, are treated as equals under GAAP.

A partial offset to this overstated liability is a $15.5 billion “goodwill” asset that we incurred in buying our

insurance companies and that increases book value. In very large part, this goodwill represents the price we paid for

the float-generating capabilities of our insurance operations. The cost of the goodwill, however, has no bearing on

its true value. For example, if an insurance company sustains large and prolonged underwriting losses, any goodwill

asset carried on the books should be deemed valueless, whatever its original cost.

Fortunately, that does not describe Berkshire. Charlie and I believe the true economic value of our

insurance goodwill – what we would happily pay for float of similar quality were we to purchase an insurance

operation possessing it – to be far in excess of its historic carrying value. Indeed, almost the entire $15.5 billion we

carry for goodwill in our insurance business was already on our books in 2000. Yet we subsequently tripled our

float. Its value today is one reason – a huge reason – why we believe Berkshire’s intrinsic business value

substantially exceeds its book value.

************

Berkshire’s attractive insurance economics exist only because we have some terrific managers running

disciplined operations that possess hard-to-replicate business models. Let me tell you about the major units.

First by float size is the Berkshire Hathaway Reinsurance Group, managed by Ajit Jain. Ajit insures risks

that no one else has the desire or the capital to take on. His operation combines capacity, speed, decisiveness and,

most important, brains in a manner unique in the insurance business. Yet he never exposes Berkshire to risks that

are inappropriate in relation to our resources.

Indeed, Berkshire is far more conservative in avoiding risk than most large insurers. For example, if the

insurance industry should experience a $250 billion loss from some mega-catastrophe – a loss about triple anything

it has ever experienced – Berkshire as a whole would likely record a significant profit for the year because of its

many streams of earnings. We would also remain awash in cash and be looking for large opportunities to write

business in an insurance market that might well be in disarray. Meanwhile, other major insurers and reinsurers

would be swimming in red ink, if not facing insolvency.

When Ajit entered Berkshire’s office on a Saturday in 1986, he did not have a day’s experience in the

insurance business. Nevertheless, Mike Goldberg, then our manager of insurance, handed him the keys to our

reinsurance business. With that move, Mike achieved sainthood: Since then, Ajit has created tens of billions of

value for Berkshire shareholders.

************

We have another reinsurance powerhouse in General Re, managed by Tad Montross.

At bottom, a sound insurance operation needs to adhere to four disciplines. It must (1) understand all

exposures that might cause a policy to incur losses; (2) conservatively assess the likelihood of any exposure actually

causing a loss and the probable cost if it does; (3) set a premium that, on average, will deliver a profit after both

prospective loss costs and operating expenses are covered; and (4) be willing to walk away if the appropriate

premium can’t be obtained.

11