Berkshire Hathaway 2015 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2015 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

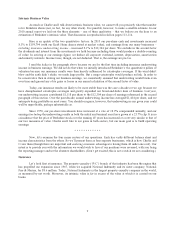

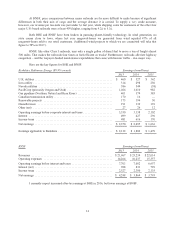

One reason we were attracted to the P/C business was its financial characteristics: P/C insurers receive

premiums upfront and pay claims later. In extreme cases, such as those arising from certain workers’ compensation

accidents, payments can stretch over many decades. This collect-now, pay-later model leaves P/C companies

holding large sums – money we call “float” – that will eventually go to others. Meanwhile, insurers get to invest this

float for their own benefit. Though individual policies and claims come and go, the amount of float an insurer holds

usually remains fairly stable in relation to premium volume. Consequently, as our business grows, so does our float.

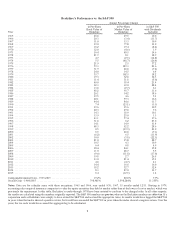

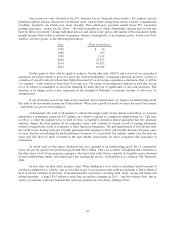

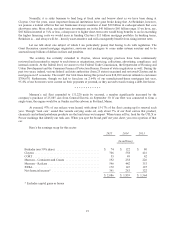

And how we have grown, as the following table shows:

Year Float (in millions)

1970 $ 39

1980 237

1990 1,632

2000 27,871

2010 65,832

2015 87,722

Further gains in float will be tough to achieve. On the plus side, GEICO and several of our specialized

operations are almost certain to grow at a good clip. National Indemnity’s reinsurance division, however, is party to

a number of run-off contracts whose float drifts downward. If we do in time experience a decline in float, it will be

very gradual – at the outside no more than 3% in any year. The nature of our insurance contracts is such that we can

never be subject to immediate or near-term demands for sums that are of significance to our cash resources. This

structure is by design and is a key component in the strength of Berkshire’s economic fortress. It will never be

compromised.

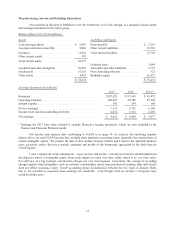

If our premiums exceed the total of our expenses and eventual losses, we register an underwriting profit

that adds to the investment income our float produces. When such a profit is earned, we enjoy the use of free money

– and, better yet, get paid for holding it.

Unfortunately, the wish of all insurers to achieve this happy result creates intense competition, so vigorous

indeed that it sometimes causes the P/C industry as a whole to operate at a significant underwriting loss. This loss,

in effect, is what the industry pays to hold its float. Competitive dynamics almost guarantee that the insurance

industry, despite the float income all its companies enjoy, will continue its dismal record of earning subnormal

returns on tangible net worth as compared to other American businesses. The prolonged period of low interest rates

the world is now dealing with also virtually guarantees that earnings on float will steadily decrease for many years

to come, thereby exacerbating the profit problems of insurers. It’s a good bet that industry results over the next ten

years will fall short of those recorded in the past decade, particularly for those companies that specialize in

reinsurance.

As noted early in this report, Berkshire has now operated at an underwriting profit for 13 consecutive

years, our pre-tax gain for the period having totaled $26.2 billion. That’s no accident: Disciplined risk evaluation is

the daily focus of all of our insurance managers, who know that while float is valuable, its benefits can be drowned

by poor underwriting results. All insurers give that message lip service. At Berkshire it is a religion, Old Testament

style.

So how does our float affect intrinsic value? When Berkshire’s book value is calculated, the full amount of

our float is deducted as a liability, just as if we had to pay it out tomorrow and could not replenish it. But to think of

float as strictly a liability is incorrect. It should instead be viewed as a revolving fund. Daily, we pay old claims and

related expenses – a huge $24.5 billion to more than six million claimants in 2015 – and that reduces float. Just as

surely, we each day write new business that will soon generate its own claims, adding to float.

10