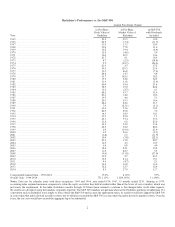

Berkshire Hathaway 2014 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2014 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

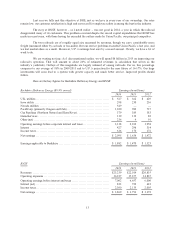

‹Our subsidiaries spent a record $15 billion on plant and equipment during 2014, well over twice their

depreciation charges. About 90% of that money was spent in the United States. Though we will always

invest abroad as well, the mother lode of opportunities runs through America. The treasures that have been

uncovered up to now are dwarfed by those still untapped. Through dumb luck, Charlie and I were born in

the United States, and we are forever grateful for the staggering advantages this accident of birth has given

us.

‹Berkshire’s yearend employees – including those at Heinz – totaled a record 340,499, up 9,754 from last

year. The increase, I am proud to say, included no gain at headquarters (where 25 people work). No sense

going crazy.

‹Berkshire increased its ownership interest last year in each of its “Big Four” investments – American

Express, Coca-Cola, IBM and Wells Fargo. We purchased additional shares of IBM (increasing our

ownership to 7.8% versus 6.3% at yearend 2013). Meanwhile, stock repurchases at Coca-Cola, American

Express and Wells Fargo raised our percentage ownership of each. Our equity in Coca-Cola grew from

9.1% to 9.2%, our interest in American Express increased from 14.2% to 14.8% and our ownership of

Wells Fargo grew from 9.2% to 9.4%. And, if you think tenths of a percent aren’t important, ponder this

math: For the four companies in aggregate, each increase of one-tenth of a percent in our ownership raises

Berkshire’s portion of their annual earnings by $50 million.

These four investees possess excellent businesses and are run by managers who are both talented and

shareholder-oriented. At Berkshire, we much prefer owning a non-controlling but substantial portion of a

wonderful company to owning 100% of a so-so business. It’s better to have a partial interest in the Hope

Diamond than to own all of a rhinestone.

If Berkshire’s yearend holdings are used as the marker, our portion of the “Big Four’s” 2014 earnings

before discontinued operations amounted to $4.7 billion (compared to $3.3 billion only three years ago). In

the earnings we report to you, however, we include only the dividends we receive – about $1.6 billion last

year. (Again, three years ago the dividends were $862 million.) But make no mistake: The $3.1 billion of

these companies’ earnings we don’t report are every bit as valuable to us as the portion Berkshire records.

The earnings these investees retain are often used for repurchases of their own stock – a move that

enhances Berkshire’s share of future earnings without requiring us to lay out a dime. Their retained

earnings also fund business opportunities that usually turn out to be advantageous. All that leads us to

expect that the per-share earnings of these four investees, in aggregate, will grow substantially over time

(though 2015 will be a tough year for the group, in part because of the strong dollar). If the expected gains

materialize, dividends to Berkshire will increase and, even more important, so will our unrealized capital

gains. (For the package of four, our unrealized gains already totaled $42 billion at yearend.)

Our flexibility in capital allocation – our willingness to invest large sums passively in non-controlled

businesses – gives us a significant advantage over companies that limit themselves to acquisitions they can

operate. Our appetite for either operating businesses or passive investments doubles our chances of finding

sensible uses for Berkshire’s endless gusher of cash.

‹I’ve mentioned in the past that my experience in business helps me as an investor and that my investment

experience has made me a better businessman. Each pursuit teaches lessons that are applicable to the other.

And some truths can only be fully learned through experience. (In Fred Schwed’s wonderful book, Where

Are the Customers’ Yachts?, a Peter Arno cartoon depicts a puzzled Adam looking at an eager Eve, while a

caption says, “There are certain things that cannot be adequately explained to a virgin either by words or

pictures.” If you haven’t read Schwed’s book, buy a copy at our annual meeting. Its wisdom and humor are

truly priceless.)

6