Berkshire Hathaway 2014 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2014 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Management’s Discussion (Continued)

Investment and Derivative Gains/Losses (Continued)

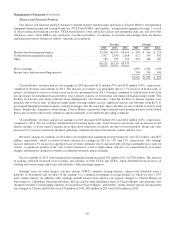

Derivative gains/losses primarily represent the changes in fair value of our credit default and equity index put option

contracts. Periodic changes in the fair values of these contracts are reflected in earnings and can be significant, reflecting the

volatility of underlying credit and equity markets.

In 2014, derivative contracts produced pre-tax gains of $506 million. The change in the fair value of our credit default

contract during 2014 produced a pre-tax gain of $397 million, and was attributable to lower credit spreads. There were no credit

loss payments in 2014. Equity index put option contracts produced pre-tax gains of $108 million in 2014. Such gains reflected

the favorable impact of foreign currency exchange rate changes and generally higher index values, partially offset by the

negative impact of lower interest rate assumptions. As of December 31, 2014, the intrinsic value of these contracts was

approximately $1.4 billion and our recorded liability at fair value was approximately $4.6 billion. Our ultimate payment

obligations, if any, under our remaining equity index put option contracts will be determined as of the contract expiration dates,

which begin in 2018, and will be based on the intrinsic value as defined under the contracts as of those dates.

In 2013, derivative contracts generated a pre-tax gain of $2.6 billion, including $2.8 billion gain from equity index put

option contracts and pre-tax losses of $213 million from credit default contracts. The gain from equity index put option

contracts was due to changes in fair values of the contracts as a result of overall higher equity index values, favorable currency

movements and modestly higher interest rate assumptions. The credit default contract loss was primarily attributable to an

increase in estimated liabilities of our remaining municipality issuer contract, reflecting wider credit spreads. There were no

credit loss payments in 2013.

In 2012, our derivative contracts produced pre-tax gains of approximately $2.0 billion, and included pre-tax gains from

equity index put option contracts of approximately $1.0 billion and gains from credit default contracts of approximately $900

million. The gains related to equity index put option contracts were due to increased index values, foreign currency exchange

rate changes and valuation adjustments on a small number of contracts where contractual settlements will be determined

differently than the standard determination of intrinsic value, partially offset by lower interest rate assumptions. The gains on

credit default contracts were attributable to narrower spreads and reduced time exposure, as well as from settlements related to

the termination of certain contracts. In 2012, credit loss payments were $68 million.

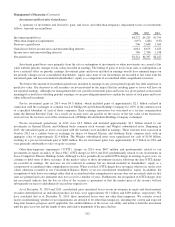

Other

Corporate income and expenses not allocated to operating businesses produced after-tax losses of $145 million in 2014,

$712 million in 2013 and $797 million in 2012. Our investments in Heinz generated after-tax earnings of $652 million in 2014

and $95 million in 2013. Also included in other earnings are amortization of fair value adjustments made in connection with

several prior business acquisitions (primarily related to the amortization of identifiable intangible assets) and corporate interest

expense. These two charges (after-tax) aggregated $682 million in 2014, $514 million in 2013 and $630 million in 2012.

Financial Condition

Our balance sheet continues to reflect significant liquidity and a strong capital base. Our consolidated shareholders’ equity

at December 31, 2014 was $240.2 billion, an increase of $18.3 billion since December 31, 2013.

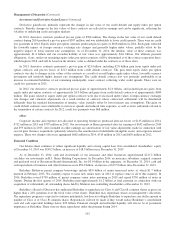

As of December 31, 2014, cash and investments of our insurance and other businesses approximated $217.2 billion

(excludes our investments in H.J. Heinz Holding Corporation). In December 2014, an insurance subsidiary acquired common

and preferred stock of Restaurant Brands International, Inc. for $3.0 billion in the aggregate. At December 31, 2014, cash and

cash equivalents of insurance and other businesses were $58.0 billion, an increase of $15.5 billion since December 31, 2013.

Berkshire Hathaway parent company borrowings include $8.0 billion of senior unsecured notes, of which $1.7 billion

matured in February 2015. We currently expect to issue new senior notes in 2015 to replace some or all of this maturity. In

2014, Berkshire issued $750 million of parent company senior notes maturing in 2019 and repaid $750 million of notes in

August. During the first quarter of 2014, Berkshire paid approximately $1.2 billion as final payment in connection with our

acquisition of substantially all outstanding shares held by Marmon non-controlling shareholders at December 31, 2013.

Berkshire’s Board of Directors has authorized Berkshire to repurchase its Class A and Class B common shares at prices no

higher than a 20% premium over the book value of the shares. Berkshire may repurchase shares at management’s discretion.

The repurchase program is expected to continue indefinitely, but does not obligate Berkshire to repurchase any dollar amount or

number of Class A or Class B common shares. Repurchases will not be made if they would reduce Berkshire’s consolidated

cash and cash equivalent holdings below $20 billion. Financial strength and redundant liquidity will always be of paramount

importance at Berkshire. There were no share repurchases under the program during 2014.

103