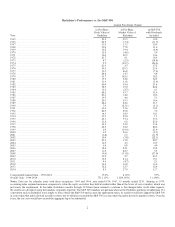

Berkshire Hathaway 2014 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2014 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

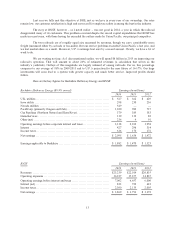

Regulated, Capital-Intensive Businesses

We have two major operations, BNSF and Berkshire Hathaway Energy (“BHE”), that share important

characteristics distinguishing them from our other businesses. Consequently, we assign them their own section in

this letter and split out their combined financial statistics in our GAAP balance sheet and income statement.

A key characteristic of both companies is their huge investment in very long-lived, regulated assets, with

these partially funded by large amounts of long-term debt that is not guaranteed by Berkshire. Our credit is in fact

not needed because each company has earning power that even under terrible economic conditions will far exceed

its interest requirements. Last year, for example, BNSF’s interest coverage was more than 8:1. (Our definition of

coverage is pre-tax earnings/interest, not EBITDA/interest, a commonly used measure we view as seriously flawed.)

At BHE, meanwhile, two factors ensure the company’s ability to service its debt under all circumstances.

The first is common to all utilities: recession-resistant earnings, which result from these companies offering an

essential service on an exclusive basis. The second is enjoyed by few other utilities: a great diversity of earnings

streams, which shield us from being seriously harmed by any single regulatory body. Recently, we have further

broadened that base through our $3 billion (Canadian) acquisition of AltaLink, an electric transmission system

serving 85% of Alberta’s population. This multitude of profit streams, supplemented by the inherent advantage of

being owned by a strong parent, has enabled BHE and its utility subsidiaries to significantly lower their cost of debt.

This economic fact benefits both us and our customers.

Every day, our two subsidiaries power the American economy in major ways:

• BNSF carries about 15% (measured by ton-miles) of all inter-city freight, whether it is transported by

truck, rail, water, air, or pipeline. Indeed, we move more ton-miles of goods than anyone else, a fact

establishing BNSF as the most important artery in our economy’s circulatory system.

BNSF, like all railroads, also moves its cargo in an extraordinarily fuel-efficient and environmentally

friendly way, carrying a ton of freight about 500 miles on a single gallon of diesel fuel. Trucks taking on

the same job guzzle about four times as much fuel.

• BHE’s utilities serve regulated retail customers in eleven states. No utility company stretches further. In

addition, we are a leader in renewables: From a standing start ten years ago, BHE now accounts for 6% of

the country’s wind generation capacity and 7% of its solar generation capacity. Beyond these businesses,

BHE owns two large pipelines that deliver 8% of our country’s natural gas consumption; the recently-

purchased electric transmission operation in Canada; and major electric businesses in the U.K. and

Philippines. And the beat goes on: We will continue to buy and build utility operations throughout the

world for decades to come.

BHE can make these investments because it retains all of its earnings. In fact, last year the company

retained more dollars of earnings – by far – than any other American electric utility. We and our

regulators see this 100% retention policy as an important advantage – one almost certain to distinguish

BHE from other utilities for many years to come.

When BHE completes certain renewables projects that are underway, the company’s renewables portfolio

will have cost $15 billion. In addition, we have conventional projects in the works that will also cost many billions.

We relish making such commitments as long as they promise reasonable returns – and, on that front, we put a large

amount of trust in future regulation.

Our confidence is justified both by our past experience and by the knowledge that society will forever

need massive investments in both transportation and energy. It is in the self-interest of governments to treat capital

providers in a manner that will ensure the continued flow of funds to essential projects. It is concomitantly in our

self-interest to conduct our operations in a way that earns the approval of our regulators and the people they

represent.

12